When you first enter the world of cryptocurrency, one of the first decisions you must make is where to store your digital assets. Unlike traditional money, which is held by banks, cryptocurrencies require the owner to manage their own access credentials—known as private keys.

This distinction introduces the concept of custody.

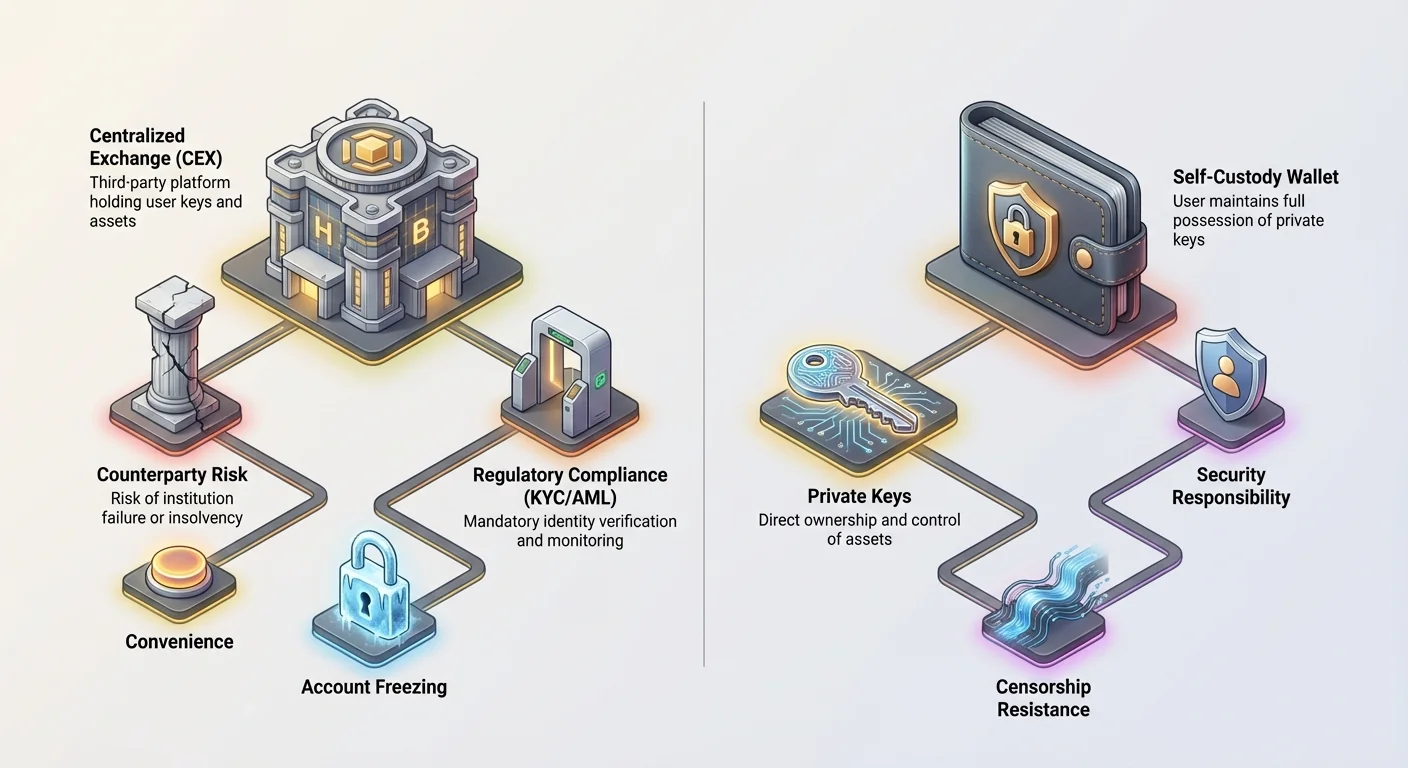

A custodial wallet is the simplest and most common entry point for beginners. It operates on the principle of delegated trust: you entrust a third party—typically a centralized cryptocurrency exchange (CEX) like Coinbase or Kraken—to hold your private keys for you. In exchange for this convenience, you trade away some control and introduce a new set of risks, particularly those related to the institution’s solvency, security posture, and legal obligations under global financial regulations.

This article moves beyond a simple definition of custodial wallets. We will analyze the core trade-offs between convenience and control, delve into the regulatory requirements like Know Your Customer (KYC) and Anti-Money Laundering (AML) that govern these platforms, and explore the legal and financial risks associated with relying on a third party to safeguard your digital wealth.

Understanding the Custody Continuum

To fully grasp what a custodial wallet entails, it is essential to understand the difference between self-custody and third-party custody.

Defining Private Keys and Ownership

In cryptocurrency, ownership is proven by possessing the private key. This key is a secret, sophisticated string of characters that grants the holder the ability to authorize transactions and move funds.

- Self-Custody (Non-Custodial): You, and only you, hold the private key. You have full control, but you also bear the full responsibility for security and recovery. If you lose the key, your funds are lost forever.

- Third-Party Custody (Custodial): The institution (the exchange or custodian) holds the private key on your behalf. When you want to move funds, you log into the platform, and the institution authorizes the transaction using the private keys they control. You own the assets, but they control the access.

A useful analogy is comparing crypto custody to owning gold. Self-custody is storing the gold bars in your own safe at home (full control, full risk). Custodial custody is storing the gold in a bank vault (convenient, but the bank controls the vault door).

Centralized Exchanges as Custodians

For most beginners, the custodial wallet is synonymous with the account they open on a major centralized exchange (CEX). These platforms combine several functions: a marketplace for trading, a user interface for accessing your funds, and, crucially, a custodian service for storing the vast majority of user assets.

When you deposit Bitcoin into your exchange account, that Bitcoin is usually moved into the exchange's large, centralized "hot" and "cold" wallets, mixed with the assets of all other users. Your balance on the screen is essentially an IOU—a record on the exchange's internal ledger stating how much crypto you are entitled to withdraw.

The Primary Appeal: Convenience and Accessibility

The enduring popularity of custodial wallets stems from the immense convenience and lower barrier to entry they provide, making them the default choice for millions of new users.

Eliminating Key Management Stress

The single biggest benefit of the custodial model is the removal of responsibility for managing complex private keys and seed phrases. For a beginner, the thought of securing a 12- or 24-word seed phrase against loss, theft, or fire is daunting.

Custodial wallets handle all the technical security measures for you. If you forget your password, the exchange offers standard recovery mechanisms, such as email resets, two-factor authentication (2FA), and identity verification. This vastly lowers the stakes for simple user errors.

Seamless Trading and Integrated Services

Centralized exchanges offer a unified platform where storage is immediately integrated with liquidity, trading, and auxiliary services. This integration is crucial for users who actively trade or plan to use their crypto for immediate financial activity.

For example, if you want to swap Ethereum for Bitcoin, a custodial wallet allows you to execute that trade in seconds directly within the platform. If you were using a self-custodial wallet, you would have to transfer the funds to an exchange first, wait for network confirmations, conduct the trade, and then potentially withdraw the funds back to your wallet—a time-consuming and expensive process involving multiple steps and network fees.

Regulatory Footing for Institutional Users

While not a direct benefit for retail users, the fact that major exchanges are regulated financial entities (or attempt to operate within regulatory frameworks) makes them necessary partners for institutions, corporations, and licensed investment funds. These entities often cannot use pure self-custody due to strict internal compliance, auditing, and insurance requirements, making regulated custodial services mandatory for participating in the crypto market.

The Fundamental Risks of Centralized Custody

The trade-off for convenience is the introduction of systemic and counterparty risks. When you delegate custody, you become dependent on the third party's operational integrity.

Counterparty Risk: Insolvency and Bankruptcy

The most significant danger of custodial wallets is the risk of the institution failing—often called "counterparty risk." Since the exchange controls the private keys to the pooled funds, if the exchange goes bankrupt or becomes insolvent (meaning their debts outweigh their assets), users may lose access to their funds.

This risk was starkly demonstrated by major exchange failures. When these firms collapse, user funds are typically treated as assets of the bankrupt company, forcing users to become unsecured creditors in long, complex legal proceedings. The phrase "Not your keys, not your coin" serves as the primary warning against this risk. Your balance on the screen might show $10,000, but if the exchange is insolvent, your ability to withdraw that $10,000 may be permanently compromised.

Security Vulnerabilities and Centralized Attack Vectors

While major exchanges invest heavily in cybersecurity, centralizing billions of dollars worth of assets makes them massive targets. Historically, large-scale exchange hacks have resulted in the irreversible loss of user funds.

While decentralized protocols can also be hacked, a successful attack on a custodial exchange affects millions of users simultaneously. Even if the platform itself is not breached, the user accounts are often targets for phishing and social engineering attacks, meaning that a compromised user password on a custodial platform can lead to the immediate theft of funds, whereas self-custody typically requires a direct theft of the key itself.

Regulatory Seizure and Account Freezing

Since custodial wallets operate within defined legal jurisdictions, they are required to comply with local and international laws, court orders, and government directives. This means that a court order, a law enforcement request, or an international sanctions mandate can compel the custodian to freeze a specific user’s account, preventing them from withdrawing or transacting with their funds, even if the user is ultimately found innocent of any wrongdoing.

This control over access, based on external legal pressures, fundamentally undermines the core promise of censorship-resistance that defines non-custodial digital assets.

The Regulatory Environment and Its Impact

The rise of custodial exchanges has forced governments worldwide to apply traditional financial regulatory tools, primarily aimed at preventing illicit financial activity. For users, this means sacrificing anonymity and submitting to identity verification protocols.

KYC and AML: The Cost of Compliance

Know Your Customer (KYC) and Anti-Money Laundering (AML) are the cornerstones of regulatory compliance for custodial institutions.

- KYC: Requires exchanges to verify the identity of every user (name, address, date of birth) using government-issued documents. This links your digital asset activity directly to your real-world identity.

- AML: Requires exchanges to monitor transactions for suspicious activity, file detailed reports on large transactions, and screen all users against global watchlists and sanctions lists.

For the user, KYC/AML means that crypto is no longer an anonymous asset class when held on a custodial platform. While this compliance promotes mainstream acceptance and discourages criminal usage, it introduces privacy risks and guarantees that the government can trace the movement of funds into and out of the regulated environment.

Compliance with Global Sanctions

Regulated custodians must operate within the framework of global sanctions. For example, if the U.S. Office of Foreign Assets Control (OFAC) imposes sanctions on a specific entity, person, or geographical area, any compliant, centralized exchange must immediately screen its entire user base and transaction history to ensure it is not doing business with the sanctioned parties.

This regulatory obligation creates immediate friction for users caught in sanctioned regions or those whose funds interact with blacklisted addresses. The exchange is legally required to freeze the assets, regardless of the user's specific circumstances, thereby reinforcing the centralized control over access.

The Role of Regulated Crypto Custodians

It is important to differentiate between a centralized exchange (like Binance or Coinbase) and a professional, regulated custodian (often a specialized trust company or financial service provider).

While both hold private keys, professional custodians often operate under stricter financial licenses and have a fiduciary duty to their clients, meaning they legally must act in the clients’ best financial interest. They typically use superior security measures, such as offline cold storage in high-security vaults, and hold minimal operational risk because they only store assets and do not offer speculative trading or lending services. These services are usually designed for institutions rather than retail investors, offering a higher degree of regulated safety than standard CEX wallets.

Mitigating Trust: Transparency and Liability

In the wake of major custodial failures, the crypto industry has sought ways to provide users with assurances that the funds they see on their screens are genuinely backed 1:1 by real assets held by the custodian.

Proof of Reserves (PoR) Models

Proof of Reserves (PoR) is a cryptographic auditing technique intended to verify that a custodian holds the assets they claim to hold on behalf of their users. PoR is similar to a crypto platform security audit but focuses solely on asset verification. While PoR confirms solvency at a single moment in time (do they hold enough Bitcoin today?), it does not confirm segregation of client assets. It doesn't guarantee that the custodian hasn't secretly borrowed or lent out the funds, nor does it guarantee operational integrity. Furthermore, PoR rarely addresses fiat currency holdings or off-chain liabilities, offering only a partial picture of the custodian's financial health. For beginners, PoR should be seen as a necessary but insufficient step toward establishing trust. Wait, I must only insert one link. Let me find a better insertion point for P30.

How PoR Works:

- Proof of Liability: The custodian cryptographically proves the sum total of all user liabilities (the amount owed to users). This is often done using a Merkle Tree, which summarizes millions of individual account balances into a single, verifiable root hash, without revealing individual balances.

- Proof of Assets: The custodian cryptographically proves ownership and control over the on-chain addresses that hold the equivalent total assets. This is typically done by signing a specific transaction or message using the addresses' private keys.

Limitations of PoR:

While PoR confirms solvency at a single moment in time (do they hold enough Bitcoin today?), it does not confirm segregation of client assets. It doesn't guarantee that the custodian hasn't secretly borrowed or lent out the funds, nor does it guarantee operational integrity. Furthermore, PoR rarely addresses fiat currency holdings or off-chain liabilities, offering only a partial picture of the custodian's financial health. For beginners, PoR should be seen as a necessary but insufficient step toward establishing trust.

Insurance and Client Liability

A common beginner assumption is that centralized crypto exchanges offer insurance similar to the Federal Deposit Insurance Corporation (FDIC) found in traditional banks. This is generally false.

- FDIC/SIPC Analogies: FDIC protection (up to $250,000 in the US) covers losses resulting from bank failure. SIPC coverage protects securities investors from broker failure. Neither of these models typically apply directly to cryptocurrency holdings on an unregulated CEX.

- Custodial Insurance: Some large, regulated exchanges carry proprietary commercial insurance policies, but these policies are almost always limited in scope. They typically only cover assets held in "cold storage" (offline) against specific risks, such as theft by a malicious insider, not against market losses or against the exchange’s business mismanagement (insolvency).

- Fiat vs. Crypto: Importantly, any fiat money you hold on a centralized exchange might be insured through traditional banking partners. However, the crypto assets themselves often remain uninsured against the primary risk: institutional failure. Users must carefully read the platform's terms of service to understand exactly what, if anything, is insured, and under what circumstances.

Choosing the Right Approach: A Beginner’s Guide

For new users, the choice between custodial and self-custodial wallets should be based on risk tolerance, technical comfort, and primary use case.

| Factor | Custodial Wallet (CEX) | Self-Custodial Wallet (e.g., Ledger, MetaMask) |

|---|---|---|

| Key Control | Third-party holds keys | User holds keys |

| Primary Risk | Counterparty risk (insolvency, seizure) | User error (losing seed phrase) |

| Security | Centralized, professional security team | Depends entirely on the user’s diligence |

| Regulatory Burden | High (KYC/AML required) | Low/None |

| Best For | Active traders, small balances, beginners, quick onboarding | Long-term investors, large balances, high security needs |

Actionable Tips for Using Custodial Wallets

If you choose to use a custodial wallet for its convenience, follow these best practices to minimize risk:

- Keep Balances Low: Treat your custodial wallet as a checking account—a place for assets you plan to trade or spend soon. Do not use it as a long-term savings or investment vehicle. Assets intended for long-term holding should be moved to a self-custody solution.

- Enable Maximum Security: Always enable two-factor authentication (2FA) using an authenticator app (like Google Authenticator) rather than SMS (which is more susceptible to phishing). Use strong, unique passwords.

- Research Regulation: Only use exchanges that are registered and licensed within reputable financial jurisdictions. These platforms typically offer a higher standard of security and transparency, and a clearer legal recourse path should an issue arise.

- Stay Informed on Insolvency: Pay attention to news about the custodian’s financial health and market behavior. If an exchange restricts withdrawals or fails to provide regular, verifiable PoR statements, it may be time to move your funds immediately.

Conclusion

Custodial wallets offer a necessary bridge between the complexities of decentralized technology and the convenience expected by modern consumers. They provide an easy entry point, handle technical security, and integrate seamlessly with trading environments.

However, users must enter this arrangement with clear eyes, understanding the inherent trade-offs: when a third party holds your private keys, you sacrifice sovereignty and introduce legal and financial risks far beyond those found in the self-custody model. The convenience of a centralized account comes with the permanent risk of insolvency, regulatory seizure, and relying on the financial integrity of a single corporation.

For the security-conscious crypto user, the custodial wallet is a tool for daily transactions and trading, but never a permanent home for significant digital wealth.