Navigating the cryptocurrency market requires more than just identifying profitable trades or selecting assets with high growth potential. As the industry matures, regulatory bodies worldwide have tightened their oversight, making tax compliance and reporting standards critical factors for investors. Choosing the right platform is no longer solely about low fees or high liquidity. It is equally about finding exchanges that align with legal frameworks and simplify the burden of financial reporting.

For investors in the United States and other strictly regulated jurisdictions, the consequences of using non-compliant platforms can be severe. These range from frozen assets to complex tax audits. Therefore, understanding the operational mechanics of compliant exchanges is the first step toward a sustainable investment strategy. This involves evaluating how platforms handle identity verification, transaction tracking, and data security.

The shift toward regulation has encouraged the growth of centralized entities that mirror traditional financial institutions. These platforms offer robust security measures, insurance policies, and detailed transaction histories that are essential for tax season. However, the crypto ecosystem remains diverse. It includes decentralized platforms and peer-to-peer networks that offer different benefits but pose unique challenges regarding compliance and reporting.

The Importance of Regulatory Oversight

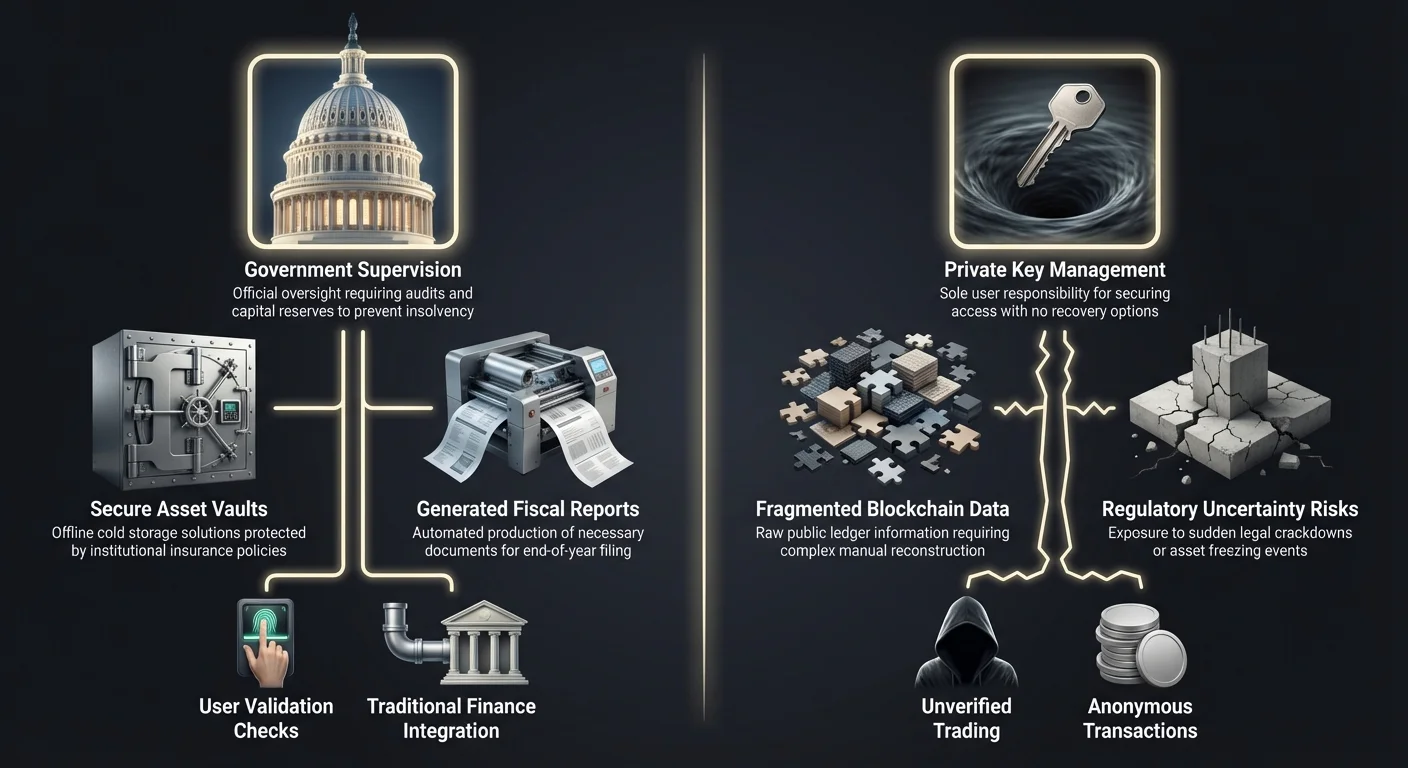

Regulatory compliance provides a safety net for users. Exchanges that adhere to strict guidelines are often required to maintain specific capital reserves and undergo regular audits. This transparency reduces the risk of insolvency and fraud. For the user, this means that funds are generally safer and that the platform is less likely to be shut down by government authorities.

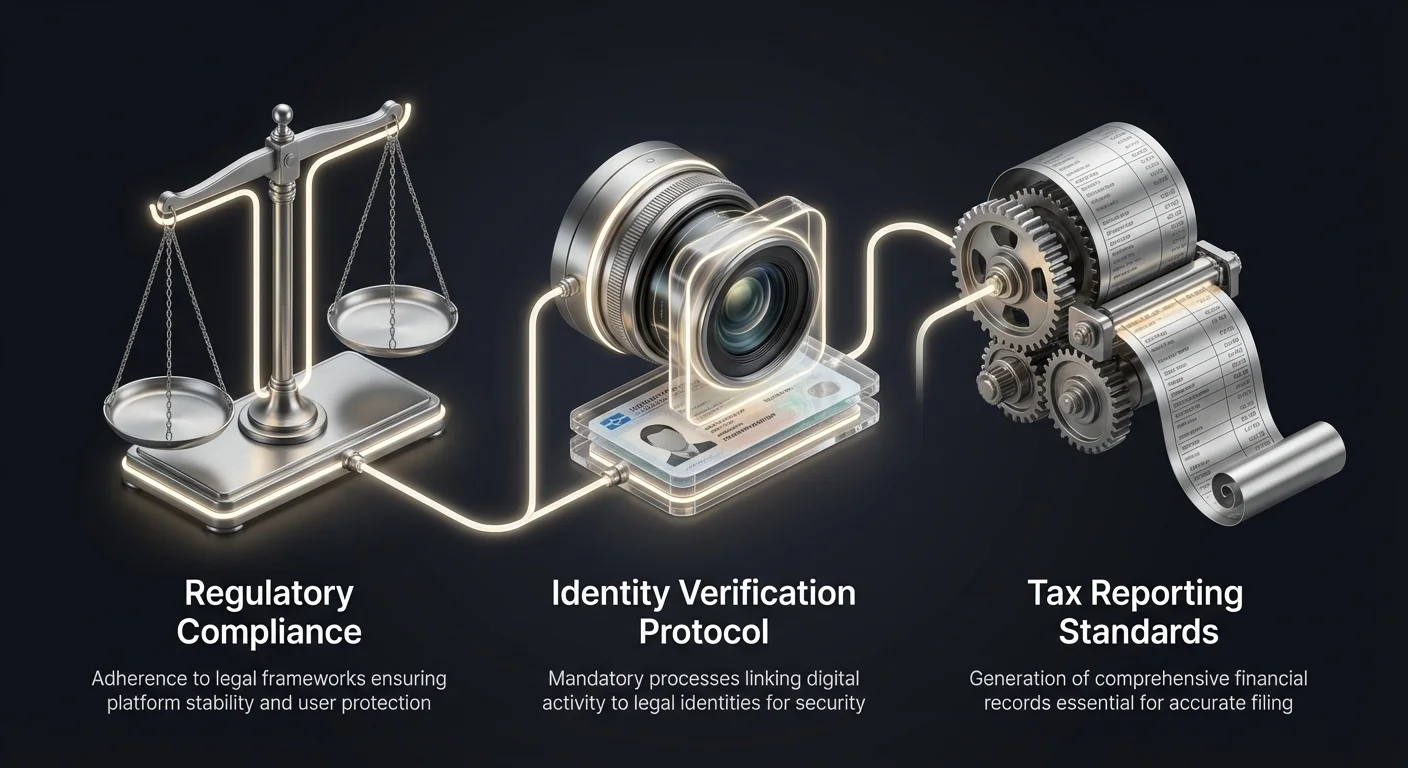

In the United States, compliance often involves adhering to standards set by the Financial Crimes Enforcement Network (FinCEN) and state-level bodies like the New York Department of Financial Services (NYDFS). Platforms operating under these licenses must implement rigorous anti-money laundering (AML) protocols. They must also verify the identity of every user through Know Your Customer (KYC) procedures.

While some traders view these requirements as intrusive, they are fundamental to the legitimacy of the market. They ensure that the exchange can operate within the banking system. This facilitates smooth deposits and withdrawals of fiat currency. Furthermore, compliant exchanges are more likely to provide necessary tax documents, such as Form 1099 in the US, which significantly simplifies the filing process for investors.

Security as a Compliance Pillar

Security and compliance are deeply interconnected. A platform that fails to secure user funds is often in violation of regulatory standards regarding consumer protection. The safest exchanges utilize cold storage solutions. This means the majority of digital assets are held offline, away from potential hackers.

Insurance is another critical component. Top-tier platforms often carry insurance policies that cover digital assets held in hot wallets (online storage) against theft or cybersecurity breaches. This level of protection is standard in traditional finance but is a distinguishing feature in the crypto world. It signals that an exchange is mature and reliable.

Regular audits reinforce this security. Independent third parties review the exchange's holdings to verify that user funds are fully backed. This practice, often referred to as Proof of Reserves, has become a benchmark for trust. It assures users that the numbers they see on their screen correspond to actual assets held in the exchange's custody.

Centralized Exchanges and Tax Reporting

Centralized exchanges (CEX) are the most common entry point for new investors. They function similarly to traditional stock brokerages. A central authority manages the order book, holds user funds, and facilitates trades. Because they act as intermediaries, these platforms are best positioned to assist with tax reporting.

These exchanges track every transaction made on their platform. This includes the date, time, price, and volume of every trade. This data is crucial for calculating capital gains and losses. At the end of the tax year, users can typically download a comprehensive transaction history. Some platforms even integrate directly with tax software to automate the calculation process.

For US users, the ability of an exchange to issue tax forms is a major advantage. It eliminates the need to manually reconstruct trading history from disparate records. However, users must remember that exchanges can only report on activity that occurs within their system. Transfers to external wallets or other exchanges must be tracked separately by the investor.

Coinbase: A Benchmark for US Compliance

Coinbase is widely recognized for setting the standard for regulatory compliance in the United States. Founded in 2012, it has grown into a publicly traded company. This status subjects it to the rigorous oversight of the Securities and Exchange Commission (SEC). For traders, this offers a high degree of transparency regarding the company's financial health and operational practices.

The platform is designed with the user's tax obligations in mind. It provides specific tools for tax reporting and offers educational resources to help users understand the tax implications of their trades. Coinbase employs strict KYC measures, ensuring that all users are verified. This minimizes the risk of illicit activity on the platform.

Security on Coinbase is robust. It utilizes vast cold storage networks to secure customer funds. The platform also carries insurance for assets held in online hot wallets. While its fee structure can be higher than some competitors, the premium pays for a regulated, secure environment that simplifies the legal aspects of crypto ownership.

Gemini: New York Regulatory Standards

Gemini is another top-tier option for traders prioritizing compliance. It is one of the few exchanges available in all 50 US states. This includes New York, which has some of the strictest crypto regulations in the country. Gemini is regulated as a trust company by the NYDFS. This designation imposes higher capital reserve requirements and compliance standards than standard money transmitter licenses.

The platform places a heavy emphasis on security certifications. It has achieved SOC 1 Type 2 and SOC 2 Type 2 compliance. These are auditing standards that verify the effectiveness of a service organization's controls over data and security. For institutional and high-net-worth individuals, these certifications provide assurance that the platform meets enterprise-grade security benchmarks.

Gemini also focuses on transparency. It operates as a full-reserve exchange. This means users' funds are backed 1:1 and are not lent out or used for the exchange's own investments. This approach aligns with the conservative risk management strategies favored by regulators and risk-averse investors.

Kraken: Security and Audit Trails

Kraken is a veteran in the industry, operating since 2011. It has built a reputation for resilience and security. It has never suffered a major hack, a significant achievement in the crypto space. Kraken emphasizes comprehensive security protocols, including 2FA and encryption.

From a compliance perspective, Kraken supports a wide range of fiat currencies and adheres to regulations in multiple global jurisdictions. It offers robust reporting tools that allow users to export detailed trade history. This is vital for accurate tax filing, especially for active traders with high transaction volumes.

Kraken also pioneered the use of independent audits to verify asset reserves. By allowing users to cryptographically verify that their funds are held by the exchange, Kraken promotes a level of transparency that regulators encourage. This "Proof of Reserves" mechanism helps build trust and ensures the platform remains solvent and accountable.

Identity Verification and KYC Protocols

Know Your Customer (KYC) protocols are the gateway to compliant crypto trading. These procedures are mandatory for any exchange that interacts with the traditional banking system. The process involves collecting personal data to verify the identity of the user. This typically includes a government-issued ID, a selfie, and proof of address.

While this eliminates anonymity, it protects the user and the platform. It prevents identity theft and ensures that the exchange is not used for money laundering. For tax purposes, KYC is essential. It links the trading account to a specific legal entity or individual. This connection allows tax authorities to verify that income and capital gains are being reported correctly.

Traders should be wary of platforms that allow significant trading volume without KYC. These platforms often operate in legal gray areas. They may face sudden regulatory crackdowns, leading to frozen assets. Furthermore, using non-compliant platforms can trigger audits if tax authorities suspect a trader is attempting to hide assets.

The Verification Process

The verification process on compliant exchanges is usually streamlined. Users upload photos of their documents through a secure portal. Automated systems and manual reviews verify the authenticity of the documents. This process can take anywhere from a few minutes to a few days, depending on the platform and the volume of applications.

Once verified, users gain access to higher withdrawal limits and a broader range of features. This often includes the ability to deposit fiat currency via bank transfer. Unverified accounts are typically restricted to crypto-to-crypto trading with low withdrawal caps. In some jurisdictions, unverified trading is prohibited entirely.

Maintaining updated verification information is also part of compliance. Exchanges may periodically request users to re-verify their identity or provide additional information if their trading patterns change. This ongoing monitoring ensures continued adherence to AML regulations.

Privacy vs. Compliance

There is often a tension between the crypto ethos of privacy and the requirements of regulation. Early crypto adopters valued anonymity. However, mass adoption has required a compromise. To integrate with the global financial system, crypto must play by the same rules as banks and stockbrokers.

Anonymous exchanges still exist. They typically do not require ID verification and may prioritize privacy coins. However, these platforms often lack fiat on-ramps. This means users cannot directly deposit dollars or euros. They must acquire crypto elsewhere and transfer it in.

From a tax perspective, anonymous exchanges complicate matters. They rarely provide tax forms. The user bears the full burden of tracking cost basis and fair market value for every trade across different platforms. Additionally, transferring funds to an opaque exchange can raise red flags with compliance teams at regulated exchanges, potentially leading to account closures.

Decentralized Exchanges (DEX) and Reporting

Decentralized exchanges (DEX) operate on a different model than their centralized counterparts. They do not rely on a central authority to hold funds or execute trades. Instead, they use smart contracts—self-executing code on a blockchain—to facilitate peer-to-peer trading. Users trade directly from their personal wallets.

This model offers advantages in terms of security and control. The exchange never takes custody of the user's assets, reducing the risk of exchange-level hacks. However, this decentralization creates significant challenges for tax reporting. DEXs generally do not collect user data. They do not perform KYC checks, and they do not issue tax forms.

Because the exchange does not track the user's identity, it cannot provide a consolidated report of gains and losses. The user must rely on blockchain data. Every transaction is recorded on the public ledger, but interpreting this raw data for tax purposes can be difficult. Users often need specialized software to scan their wallet addresses and reconstruct their trading history.

| Feature | Centralized Exchange (CEX) | Decentralized Exchange (DEX) |

|---|---|---|

| Custody | Exchange holds funds | User holds funds (Self-custody) |

| Identity | KYC required | No KYC (Anonymous) |

| Reporting | Detailed history & tax forms | Raw blockchain data only |

The Self-Custody Dilemma

Self-custody gives users complete control over their private keys. This means no third party can freeze their funds. However, with great power comes great responsibility. If a user loses their private keys, the funds are irretrievable. There is no customer support to reset a password.

From a tax perspective, self-custody requires diligent record-keeping. Moving funds from a centralized exchange to a personal wallet is generally not a taxable event (it is a transfer). However, using those funds to interact with a DEX is a taxable event.

Regulators are increasingly scrutinizing the DeFi (Decentralized Finance) space. While the software itself may be decentralized, the governance tokens and development teams behind them may fall under regulatory scope. Users should be aware that the "wild west" nature of DeFi is changing, and future regulations may impose reporting requirements on these protocols.

Smart Contracts and Complexity

Trading on a DEX involves interacting with smart contracts. These transactions can be complex. A single trade might involve multiple steps, such as approving a token for spending and then executing the swap. Each of these steps requires a network fee (gas fee).

These network fees are deductible expenses in many tax jurisdictions, as they are part of the cost of acquiring or disposing of an asset. However, tracking these fees across hundreds of transactions requires automated tools. Manual calculation is prone to error.

Furthermore, DEXs often enable access to a vast array of tokens that are not listed on centralized exchanges. Determining the fair market value of a low-liquidity token at the exact time of the trade can be challenging. This valuation is necessary to calculate the capital gain or loss accurately.

Peer-to-Peer (P2P) Platforms

Peer-to-peer (P2P) exchanges connect buyers and sellers directly. Unlike a DEX, which uses an automated liquidity pool, a P2P platform functions more like a classifieds listing. Users post offers to buy or sell crypto at a specific price and using a specific payment method. The platform usually provides an escrow service to secure the transaction.

P2P platforms are popular in regions with limited banking infrastructure or where banking restrictions prevent direct transfers to crypto exchanges. They offer a wide variety of payment methods, including cash, gift cards, and local bank transfers. This flexibility is their primary advantage.

However, compliance on P2P platforms varies. Some enforce strict KYC measures similar to centralized exchanges. Others allow for more anonymity, particularly for small amounts. For tax reporting, P2P trades present the same challenges as DEXs. The user is responsible for tracking the cost basis and the sale price in their local currency.

Risks in P2P Trading

The primary risk in P2P trading is counterparty risk. While escrow services mitigate fraud, scams are still possible. A seller might refuse to release the crypto, or a buyer might reverse a payment after receiving the assets. Users must rely on reputation systems and dispute resolution mechanisms provided by the platform.

Price variability is another factor. Prices on P2P markets are determined by individual sellers. This can lead to a wide spread of prices for the same asset. Users must be savvy to ensure they are getting a fair market rate.

From a compliance standpoint, using cash or unconventional payment methods creates a disconnect in the audit trail. If a trader is audited, proving the source of funds for a cash transaction can be difficult. Maintaining detailed records of communication and trade receipts is essential for P2P users.

Global vs. US-Specific Platforms

The regulatory landscape for cryptocurrency is fragmented. Rules vary significantly between the United States, Europe, and Asia. This has led to a divergence in the platforms available to traders in different regions. Some global giants have created specific subsidiaries to operate legally in the US.

US-based traders are generally restricted to platforms that comply with federal and state regulations. This limits their access to certain features, such as high-leverage trading or certain types of derivatives, which are heavily regulated in the US. Global traders often have access to a wider range of products.

Choosing a platform that is licensed in your specific jurisdiction is the safest bet for compliance. It ensures that the exchange is following local laws regarding consumer protection and data privacy. It also increases the likelihood that the exchange can provide relevant tax documents for that jurisdiction.

Uphold: Global Reach and Transparency

Uphold is a platform that bridges the gap between crypto and traditional finance across many jurisdictions. It serves users in over 150 countries. A key feature of Uphold is its ability to facilitate trading between diverse asset classes. Users can trade anything from crypto to fiat currencies to precious metals within a single interface.

Uphold emphasizes transparency through a "real-time reserve" model. It publishes its assets and liabilities in real-time on its website. This allows anyone to verify that the platform is fully reserved. This level of openness is rare and caters to users concerned about solvency risks.

The platform supports a vast array of assets, providing deep liquidity by connecting to multiple exchanges. For tax purposes, this consolidation of diverse assets into one platform simplifies reporting. Instead of gathering records from a precious metals broker, a forex broker, and a crypto exchange, the user has a single source of truth.

Binance: Navigating Global Rules

Binance is one of the largest exchanges in the world by trading volume. It offers an immense selection of cryptocurrencies and advanced trading features. However, its approach to compliance has had to evolve rapidly. To serve US customers, it launched Binance.US, a separate entity that adheres to US regulations.

The global Binance platform offers features like high leverage, futures, and options that are restricted on the US version. This distinction is critical. US users attempting to access the global site via VPNs risk having their accounts frozen for violating terms of service and regulatory controls.

For global users, Binance provides a comprehensive ecosystem. This includes earning products, staking, and a launchpad for new tokens. The platform has ramped up its compliance efforts globally, implementing mandatory KYC for all users. This move signals its transition from an unregulated startup to a mature financial institution.

Fee Structures and Tax Implications

Fees are an unavoidable part of crypto trading. However, they also play a role in tax calculations. Trading fees are generally considered part of the cost basis of the asset. When you buy Bitcoin, the fee you pay is added to your cost. When you sell, the fee is subtracted from the proceeds.

This effectively reduces your taxable capital gain (or increases your capital loss). Therefore, high fees act as a drag on investment performance but offer a small tax deduction. Conversely, low-fee exchanges maximize immediate profit. Understanding the fee structure of an exchange is vital for accurate accounting.

Exchanges use different models. The most common is the maker-taker model. Makers (who provide liquidity by placing limit orders) usually pay lower fees than takers (who remove liquidity by placing market orders). Some platforms also charge for deposits and withdrawals.

Minimizing Costs

To optimize returns, traders should look for exchanges with competitive fee schedules. Many platforms offer tiered fees, where costs decrease as trading volume increases. Using the exchange's native token to pay for fees can also result in significant discounts.

Network fees (gas fees) are separate from exchange fees. These are paid to the miners or validators who secure the blockchain. On a centralized exchange, these are often bundled into the withdrawal fee. On a DEX, the user pays them directly. During times of network congestion, these fees can be substantial.

Accurately tracking these fees is essential. If a user fails to include fees in their cost basis, they will overpay on their capital gains tax. Good record-keeping software automates this, pulling fee data directly from the exchange's API.

Table: Fee Types and Tax Impact

| Fee Type | Description | Tax Treatment |

|---|---|---|

| Trading Fee | Charged per trade (Maker/Taker) | Adds to Cost Basis / Reduces Proceeds |

| Withdrawal Fee | Charged to move funds off exchange | Generally not deductible (transfer cost) |

| Network (Gas) Fee | Blockchain transaction cost | Adds to Cost Basis if part of acquisition |

Brokerage Platforms and Simplified Access

Cryptocurrency brokers function differently than traditional exchanges. Instead of matching buy and sell orders between users, the broker acts as the counterparty. They sell the crypto to the user directly, often sourcing it from liquidity pools or other exchanges.

This model is often more user-friendly. It simplifies the interface and the purchasing process. Brokers like Robinhood or eToro (though distinct in their specific crypto offerings) fall into this category. They are designed for investors who want exposure to price movements without dealing with the complexities of wallets and blockchains.

From a compliance standpoint, brokers are usually highly regulated. They are often registered financial institutions that also handle stocks or forex. This means their reporting standards are robust. Users can expect clear, consolidated tax statements that often combine their crypto activity with their traditional investment activity.

The Trade-Offs of Brokers

The convenience of brokers often comes at a cost. Spreads—the difference between the buy and sell price—can be wider than on exchanges. This effectively acts as a hidden fee. Additionally, some brokers do not allow users to withdraw their crypto to a personal wallet. The user owns the value of the asset, but not the private keys.

This restriction eliminates the ability to use the crypto for payments or to interact with DeFi protocols. It is a purely speculative investment vehicle. For users solely interested in price appreciation, this is acceptable. For those wanting to participate in the crypto economy, it is a limitation.

However, the security on these platforms is typically institutional-grade. Because they do not facilitate external transfers (in some cases), the risk of a user sending funds to a scam address is eliminated. This "walled garden" approach offers safety for beginners but restricts freedom.

Tax on Derivatives

Some brokers offer crypto derivatives, such as Contracts for Difference (CFDs). When trading a CFD, the user does not own the underlying cryptocurrency. They are betting on the price movement. The tax treatment of CFDs can differ from buying actual crypto.

In some jurisdictions, CFD trading is treated as income rather than capital gains. It allows for leverage, meaning users can trade with more money than they have. This amplifies both gains and losses. It also complicates tax reporting, as leverage introduces overnight financing fees and potential liquidation events.

Traders must understand the specific tax laws regarding derivatives in their country. US citizens, for example, are generally restricted from trading CFDs. Using a broker ensures that the products offered are legal for the user's location, preventing accidental regulatory violations.

Handling Fiat On-Ramps and Off-Ramps

The bridge between the traditional banking system and the crypto world is known as the "ramp." On-ramps allow users to deposit fiat currency (USD, EUR, etc.) to buy crypto. Off-ramps allow them to sell crypto and withdraw fiat to their bank.

These points are the most heavily scrutinized by regulators. This is where money laundering is most likely to be detected. Therefore, any exchange offering fiat ramps must implement strict KYC procedures. The ease and speed of these transfers are major factors in choosing an exchange.

Payment methods vary. Bank transfers (ACH, SEPA, Wire) are common and usually have the lowest fees. Credit and debit cards offer instant buys but come with high processing fees. Some platforms also integrate with third-party processors or digital wallets like PayPal.

PayPal Integration

PayPal has become a significant player in the crypto on-ramp space. Its integration with exchanges makes funding an account accessible to millions of users who are already comfortable with the PayPal ecosystem. Transactions are typically instant, allowing traders to capitalize on market movements quickly.

However, privacy is a consideration. PayPal transactions create a clear digital trail linking the user's real-world identity to their crypto purchases. Both PayPal and the exchange will have records of the transaction. For tax compliance, this is actually a benefit. It creates undeniable proof of the purchase date and cost.

Fees for PayPal deposits can be higher than bank transfers. Users must weigh the convenience against the cost. Additionally, withdrawal limits may apply. Not all exchanges support withdrawals to PayPal, sometimes requiring users to withdraw to a bank account instead.

The "Paper Trail" Importance

Maintaining a clear paper trail is the best defense in a tax audit. Fiat on-ramps provide the starting point of this trail. They establish the initial investment amount. Without proof of the initial fiat deposit, a tax authority might assume that the entire value of the crypto portfolio is taxable income (zero cost basis).

Using regulated exchanges for fiat transfers ensures that these records are preserved. Even if a user moves funds to a DEX later, the initial acquisition is documented. This documentation is crucial for calculating the holding period, which determines whether gains are taxed at short-term or long-term rates.

Consistent use of the same banking channels also simplifies accounting. Mixing personal and business accounts, or using multiple third-party payment processors, can create a chaotic financial picture that is difficult to reconcile at tax time.

Conclusion

The landscape of cryptocurrency trading has shifted decisively toward compliance and regulation. For the modern investor, particularly in the US and other regulated markets, the choice of platform is a strategic decision that impacts asset security and tax liability. Centralized exchanges like Coinbase, Gemini, and Kraken offer the most robust tools for staying compliant, providing necessary documentation and adhering to strict security standards.

While decentralized and peer-to-peer platforms offer freedom and control, they shift the burden of reporting and security entirely onto the user. Navigating these options requires a clear understanding of the trade-offs between privacy, convenience, and legal obligation. Ultimately, utilizing platforms that prioritize regulatory adherence not only secures assets against insolvency and theft but also simplifies the complex reality of financial reporting.

Compliance is not just a legal requirement; it is a foundational element of protecting and preserving your digital wealth.