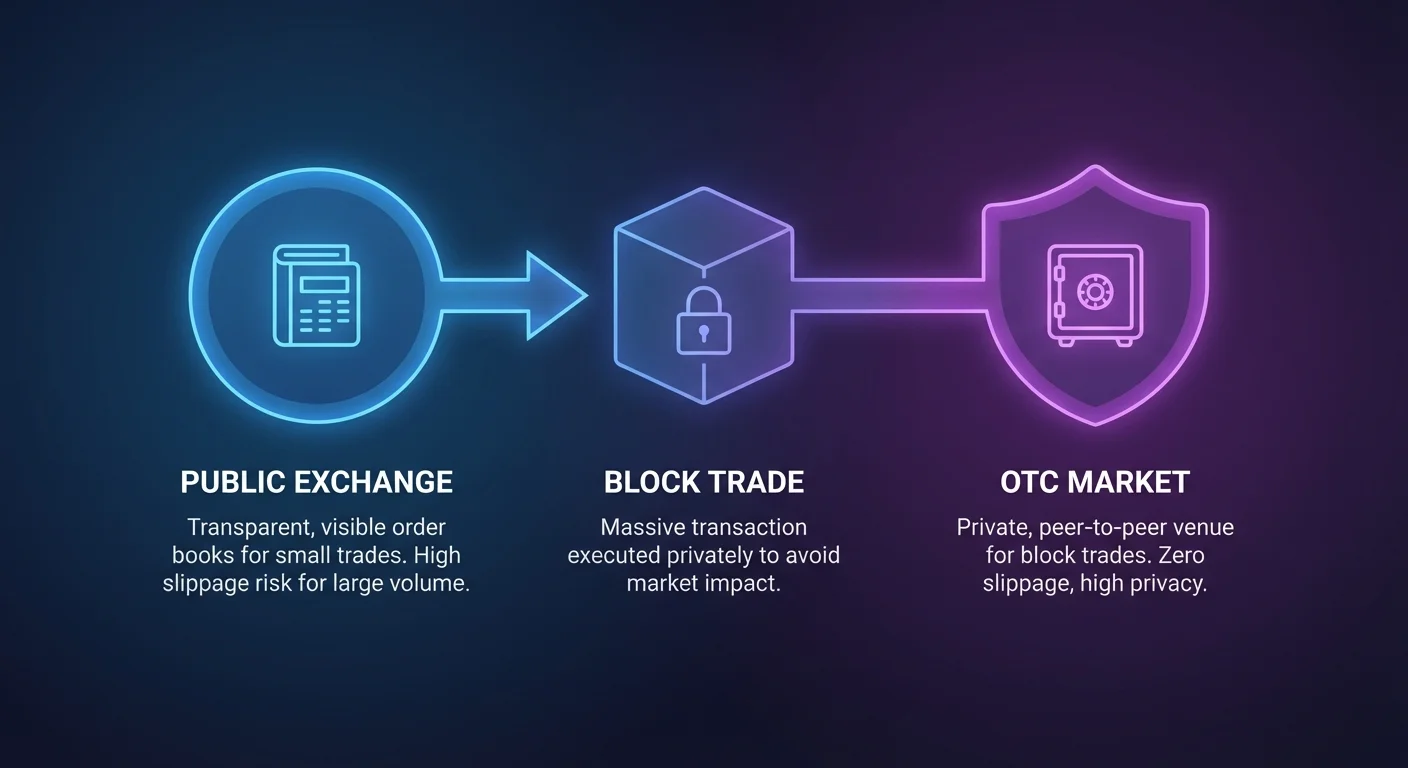

In the ecosystem of digital asset markets, the method of execution is often as critical as the asset itself. For retail traders moving small amounts of capital, public order books on centralized exchanges provide sufficient liquidity and transparency. However, for high-net-worth individuals, institutions, and mining operations, these public venues present significant challenges. The sheer size of their intended transactions, known as block trades, can destabilize market prices before an order is fully filled.

This necessity for alternative execution methods gave rise to the Over-the-Counter (OTC) trading market. This sector operates differently from the visible "spot" markets found on popular apps. It is a private, peer-to-peer environment where buyers and sellers transact directly. The primary objective here is to move substantial volume without alerting the broader market or suffering from predatory pricing mechanisms.

The paradox of OTC trading lies in the balance between opacity and efficiency. While the public market relies on transparency to discover prices, the OTC market relies on discretion to preserve value. Understanding this mechanism requires analyzing how liquidity is sourced, how risks are managed during execution, and why privacy becomes a financial necessity rather than just a preference.

The Mechanics of Off-Chain Transactions

OTC trading does not occur on a public ledger or a visible order book where buy and sell walls are displayed to the world. Instead, it functions through a network of dealers, brokers, and automated desks. When a participant wants to sell a large quantity of Bitcoin or Ethereum, they do not simply click "sell" on an exchange interface. Doing so would strip the order book of available bids, driving the price down immediately.

Direct Negotiation Protocols

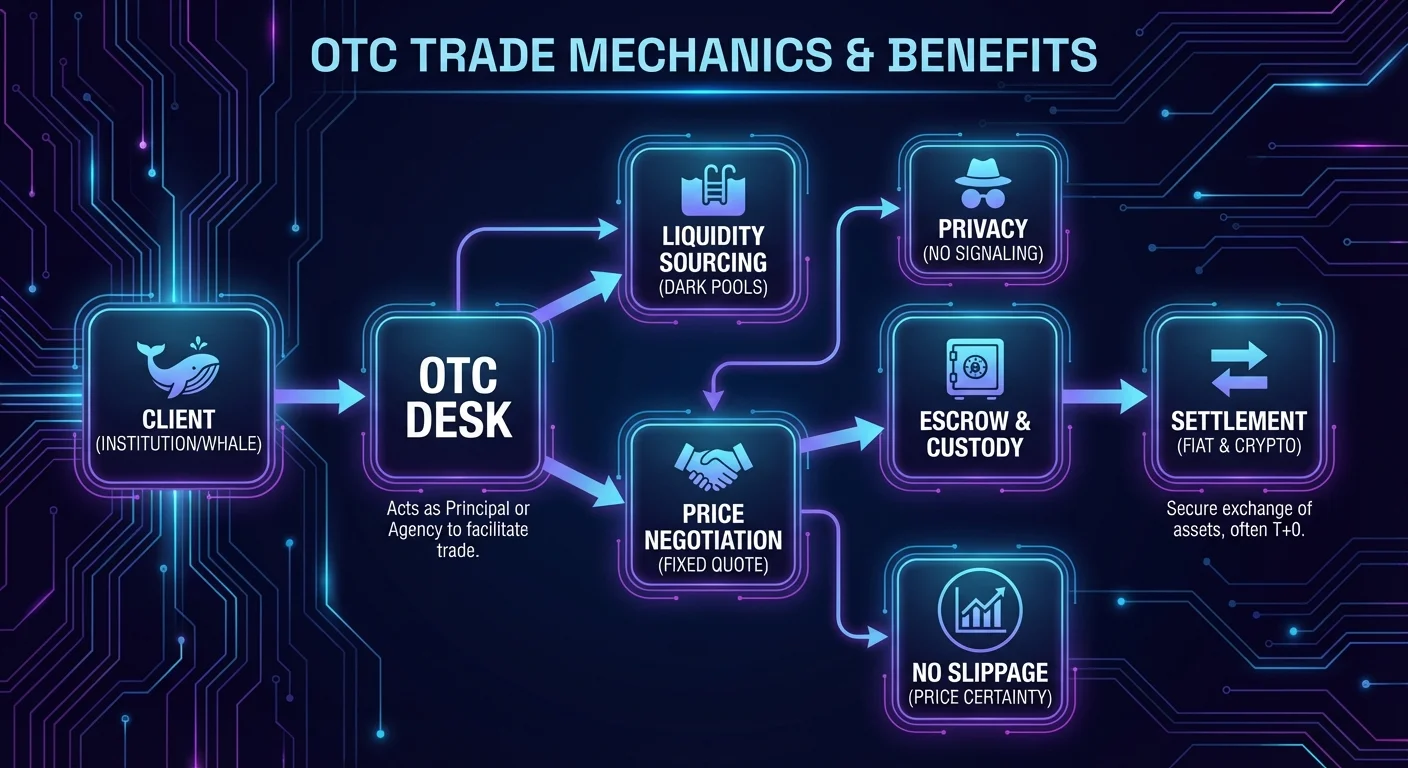

In a traditional OTC arrangement, the trade is a negotiated contract. A client contacts a desk—often via private chat channels or proprietary voice trading systems—and requests a quote for a specific volume. The dealer provides a fixed price or a pricing formula based on current market rates. This process is distinct from placing a limit order.

Once the price is agreed upon, the trade is considered "locked." The desk then takes on the responsibility of sourcing the assets or the liquidity. This might involve utilizing their own reserves, tapping into a network of other liquidity providers, or algorithmically breaking the order into smaller pieces to execute across multiple venues over time.

The Role of Principal vs. Agency Desks

Understanding the counterparty is vital in these transactions. OTC desks generally operate under two models: principal or agency. In a principal model, the desk acts as the direct counterparty. They use their own funds to buy the asset from the client or sell from their own inventory. This offers speed and immediate certainty regarding the price.

Conversely, an agency desk acts as a middleman. They do not take the other side of the trade with their own capital. Instead, they act on behalf of the client to find a buyer or seller in the market. They charge a fee for this service. While this can sometimes yield better prices if the market is favorable, it introduces execution risk if a counterparty cannot be found quickly.

Liquidity Dynamics in Block Trades

Liquidity in the context of block trades is fundamentally different from retail liquidity. On a standard exchange, liquidity is visual. You can see the depth of the order book. However, this visible liquidity is often "thin" compared to the needs of institutional capital. A sell order of 500 Bitcoin might consume the entire buy side of a standard order book, crashing the price by several percentage points.

Accessing Dark Liquidity Pools

OTC desks access what is known as "deep" or "dark" liquidity. These are pools of capital that are not displayed publicly. They consist of other institutional players, cold storage reserves held by the desk, or aggregated liquidity from fragmented sources. By matching a large buyer directly with a large seller, the desk bypasses the public order book entirely.

This prevents the "slippage" that occurs on public exchanges. Slippage is the difference between the expected price of a trade and the price at which the trade is actually executed. In high-volume transactions, even a fractional percentage of slippage can translate to losses amounting to tens or hundreds of thousands of dollars. Deep liquidity pools ensure that the price remains stable throughout the entire transaction.

The Impact of Market Fragmentation

The crypto market is highly fragmented, with liquidity split across hundreds of exchanges and blockchains. OTC desks serve as aggregators. They often maintain accounts and connections across this fragmented landscape. When a block trade is requested, they can source liquidity from Asia, North America, and Europe simultaneously.

This global reach is essential for assets beyond Bitcoin and Ethereum. For altcoins with lower trading volumes, the risk of slippage is exponentially higher. A dedicated OTC desk can coordinate a transaction that would be impossible to execute on a single public exchange without destroying the asset's market structure.

Execution Risk and Price Stability

Execution risk refers to the danger that a trade will fail to complete or will complete at a significantly unfavorable price due to market movements during the process. In the volatile cryptocurrency sector, prices can fluctuate wildly in the span of minutes. For a block trade, the time it takes to execute is a period of high exposure.

Managing Volatility During Settlement

One of the primary advantages of OTC trading is the ability to lock in a price. When a dealer provides a quote, it is usually valid for a short window (often seconds or minutes). Once accepted, that price is binding regardless of what happens in the public market immediately after. This transfers the volatility risk from the client to the desk.

If the market crashes two minutes after a client sells a block of Bitcoin at a fixed rate, the client is protected. The desk absorbs that variance. To manage this, desks often employ sophisticated hedging strategies. They might use derivatives, futures contracts, or offsetting trades on other platforms to neutralize their exposure to the asset's price movements.

Slippage Mitigation Strategies

For trades that are not executed as a single block but are instead "worked" by an agency desk, minimizing slippage requires algorithmic precision. Desks use Smart Order Routers (SORs) to slice a massive order into thousands of micro-orders. These micro-orders are dispersed across various exchanges over a set period.

The goal is to mimic organic market activity. If the algorithms are successful, the market absorbs the selling pressure without triggering panic or algorithmic trading bots that hunt for large orders. This "stealth" execution is the only way to exit large positions without cannibalizing the value of the remaining assets in the portfolio.

The Privacy Dilemma in Institutional Finance

Privacy in crypto block trades is not necessarily about ideological anonymity; it is a strategic financial requirement. Public blockchains are transparent ledgers. If a known wallet address associated with a major fund or early adopter moves 10,000 BTC to an exchange, it signals intent.

Signaling Risk and Front-Running

"Signaling risk" occurs when the market detects a large player is about to make a move. If traders see a massive inflow of Bitcoin to a public exchange, they anticipate a sell-off. High-frequency traders and algorithmic bots will immediately "front-run" the trade. They sell their positions before the whale can, driving the price down.

By the time the whale actually executes their trade, the price has already dropped. This is a predatory environment for large capital. OTC trades mitigate this by settling off the public order books. While the final transaction eventually settles on the blockchain (unless it is an internal book transfer), the intent to trade is never broadcasted beforehand.

Strategic Anonymity

Strategic anonymity preserves the trader's alpha. If the market knows a large institution is accumulating a specific altcoin, the price will skyrocket due to copy-trading behaviors. By accumulating slowly via OTC desks, an institution can build a substantial position at a consistent average price.

This discretion extends to the platform level. Many OTC services and specialized swap platforms operate with varying degrees of data retention. While compliant desks require KYC (Know Your Customer) documentation, the trade data itself is kept confidential between the two parties, unlike the public ticker tape of a centralized exchange.

Counterparty Risk and Settlement Assurance

While OTC trading solves liquidity and privacy issues, it introduces counterparty risk. In a public exchange, the exchange itself acts as the central clearinghouse. If you buy, the exchange guarantees the crypto is delivered. In a direct peer-to-peer OTC trade, trust is paramount.

The Necessity of Escrow and Custody

To mitigate the risk of one party defaulting, reputable OTC desks utilize rigorous settlement procedures. This often involves escrow services. The seller deposits the crypto into a secure, multi-signature wallet controlled by the desk or a third-party custodian. The buyer wires the fiat currency.

Only when both assets are verified in the desk’s possession are the funds released to the respective parties. This eliminates the "who goes first" standoff. Institutional-grade custody solutions, often backed by cold storage and insurance policies, are standard requirements for desks handling volumes in the millions of dollars.

Settlement Timelines and Efficiency

Speed of settlement varies significantly. In the traditional banking world, wire transfers can take days (T+2 or T+3 settlement). Crypto, by nature, allows for near-instant settlement. However, the friction often lies in the fiat leg of the transaction.

Top-tier OTC desks often maintain pre-funded accounts or credit lines with banking partners to facilitate "T+0" or same-day settlement. This ensures that liquidity is not locked up in banking limbo. For crypto-to-crypto swaps, settlement can be nearly instantaneous, leveraging the speed of the underlying blockchains.

Comparing OTC Venues and Public Exchanges

Choosing between an OTC desk and a public exchange depends entirely on the trader's goals and volume. The following table outlines the structural differences that influence this decision.

| Feature | Public Exchange | OTC Desk |

|---|---|---|

| Primary User | Retail & Small Traders | Institutions & Whales |

| Price Mechanism | Market Order Book | Negotiated/Fixed Quote |

| Slippage Risk | High for large volume | Minimal/None |

| Privacy | Low (Public Book) | High (Private Chat) |

| Settlement | Instant (on platform) | Delayed (Bank Wires) |

| Fee Structure | Maker/Taker Fees | Spread (Net Price) |

The Trade-Off Analysis

The primary trade-off is cost versus certainty. Public exchanges often appear cheaper on paper because of low maker/taker fees. However, for large trades, the hidden cost of slippage often exceeds the fees charged by OTC desks.

OTC desks usually charge a "spread"—the difference between the buy and sell price—rather than a transparent commission line item. While this spread might seem higher than a 0.1% exchange fee, the guarantee of a fixed price on a million-dollar trade is often worth the premium to avoid a 2% or 3% slippage loss.

The Rise of Automated Swap Platforms

A hybrid model has emerged that bridges the gap between traditional OTC desks and retail exchanges: the automated swap platform. These platforms allow for direct crypto-to-crypto exchange without the need for an account on a centralized order-book exchange.

Non-Custodial Execution

Automated swap platforms often operate on a non-custodial basis. This means the user remains in control of their private keys throughout the process. The user sends crypto to a specific address, and the platform's algorithm calculates the exchange rate and returns the desired asset to the user's receiving wallet.

This model appeals to privacy-conscious users who may not be moving institutional volumes but still wish to avoid the intrusive data collection or potential hacks associated with holding funds on centralized exchanges. It essentially democratizes the "direct swap" mechanic of OTC trading for mid-sized traders.

Algorithm-Driven Liquidity

Unlike traditional OTC desks run by human brokers, swap platforms use algorithms to aggregate liquidity from various exchanges and liquidity providers. They scan the market for the best rates in real-time.

This automation reduces the overhead costs associated with human dealers. Consequently, these platforms can offer competitive rates for "medium" sized trades—too big for a standard retail app but perhaps too small to interest a major institutional OTC desk.

Cost Structures and Hidden Fees

In the world of block trades and swaps, "zero fee" is a marketing term that requires scrutiny. When a platform claims zero fees, the revenue is almost always generated through the spread. The spread is the margin added to the market price.

Deconstructing the Spread

If the market price of Bitcoin is $50,000, an OTC desk might offer to buy it from you at $49,800 or sell it to you at $50,200. That $200 difference is the spread. It covers the desk's risk, operational costs, and profit margin.

Traders must calculate the "all-in" price per coin to understand the true cost of the trade. A platform with a 0.5% trading fee but a very tight spread might actually be cheaper than a "zero fee" platform that marks up the asset price by 1.5%. Transparency regarding how the rate is derived is a key indicator of a reputable desk.

Network Fees vs. Service Fees

It is also crucial to distinguish between service fees and network fees. Network fees (gas) are paid to the blockchain miners or validators to process the transaction. These are unavoidable and fluctuate based on network congestion.

Neither the OTC desk nor the swap platform controls these costs. However, efficient platforms optimize their smart contracts or transaction batching to minimize the gas burden on the user. In high-congestion networks like Ethereum, these efficiencies can result in significant savings.

Regulatory and Tax Implications

Operating in the OTC space does not exempt traders from regulatory oversight. In fact, because OTC desks handle large sums of fiat currency, they are often subject to stricter banking compliance standards than crypto-only exchanges.

Compliance and KYC

Reputable OTC desks mandate comprehensive KYC (Know Your Customer) and AML (Anti-Money Laundering) procedures. They must verify the source of funds to ensure they are not facilitating money laundering. This creates a friction point for privacy absolutists but provides a layer of legitimacy and legal protection for institutional clients.

Trading or swapping crypto is widely considered a taxable event in most jurisdictions. Whether the trade happens on a public exchange or a private OTC desk, the disposal of an asset triggers capital gains or losses.

Record Keeping for High-Volume Trading

The opacity of OTC trading can make tax reporting complex. Unlike centralized exchanges that might provide a neat end-of-year tax document, OTC trades are often bespoke contracts. Traders must maintain meticulous records of trade confirmations, settlement times, and fiat values at the moment of the transaction.

Failure to accurately track the cost basis of assets acquired through block trades can lead to severe complications during tax season. The "fixed rate" nature of OTC trades actually simplifies this somewhat, as there is a single clear price for the entire volume, rather than a list of 50 partial fills at different prices.

Conclusion

The paradox of the OTC market is that it operates in the shadows to stabilize the light. By removing massive buy and sell pressure from public order books, block trading venues allow the broader crypto ecosystem to function without constant catastrophic volatility. For the high-volume trader, the shift to OTC is rarely about convenience; it is a mathematical necessity to preserve portfolio value against slippage and front-running.

While the privacy and fixed pricing of OTC desks offer significant advantages, they come with higher barriers to entry and require a greater degree of trust in the counterparty. The evolution of automated swap platforms is slowly bridging this divide, offering OTC-like benefits to a wider audience. Ultimately, the choice of venue dictates the efficiency of the exit, proving that in crypto, how you trade is just as important as what you trade.

Large volume trading requires sacrificing transparency to gain price stability and execution certainty.