The transition from understanding cryptocurrency concepts to actively participating in the digital economy marks a significant step for any investor. While holding digital assets has historically been the primary strategy for many, the maturation of blockchain technology now offers direct avenues to utilize capital. The integration of staking and decentralized finance protocols directly into self-custodial wallets has bridged the gap between theoretical knowledge and practical application. Users no longer need to rely on centralized intermediaries to access sophisticated financial tools.

Instead of leaving assets idle, individuals can now engage with networks that require capital to function. This participation powers the infrastructure of the blockchain itself or provides necessary liquidity for financial markets. The result is a shift from passive accumulation to active network involvement. This evolution places the responsibility and the rewards directly in the hands of the asset owner. It transforms the wallet from a simple storage device into a command center for digital finance.

The Architecture of Decentralized Finance

Decentralized Finance, commonly referred to as DeFi, represents a collection of financial products that operate on permissionless networks. Unlike traditional finance, which relies on banks and brokerages to act as gatekeepers, DeFi utilizes software to automate these functions. The core objective is to recreate and improve upon legacy financial services like borrowing, lending, and trading without the need for a central authority.

Smart Contract Automation

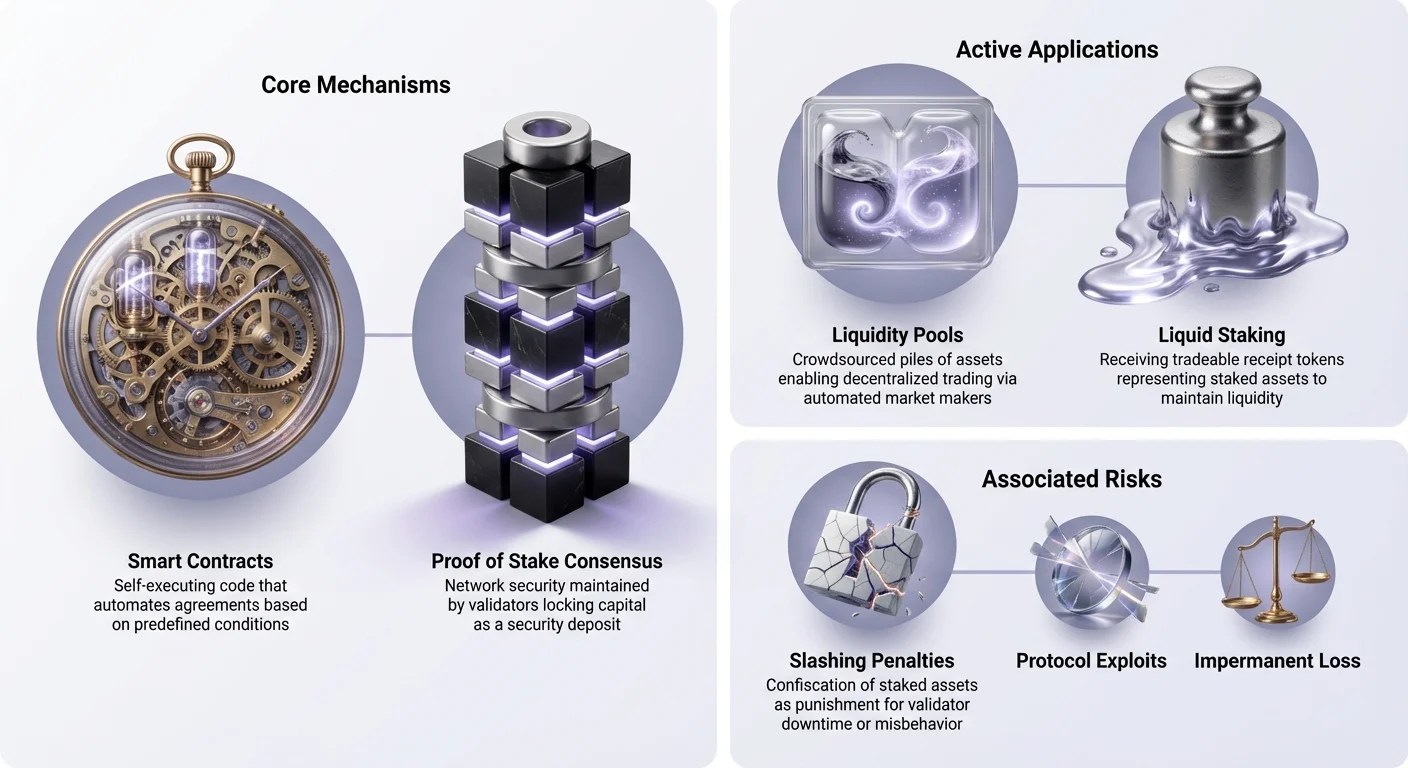

The engine driving these financial applications is the smart contract. These are self-executing contracts where the terms of the agreement are directly written into lines of code. When a user interacts with a DeFi protocol, they are not trusting a bank manager or a corporate policy. They are interacting with a deterministic program that executes exactly as it was designed.

This automation removes human error and bias from the equation. For example, in a lending protocol, the interest rates are often determined algorithmically based on supply and demand. If many users supply an asset but few borrow it, the interest rate drops to encourage borrowing. Conversely, if demand is high, rates rise to attract more lenders. This dynamic adjustment happens instantly and transparently on the blockchain.

Permissionless Lending Systems

One of the most prominent use cases within this architecture is decentralized lending. In this system, users deposit cryptocurrencies into a smart contract pool. These assets become available for other users to borrow. The distinct advantage here is the elimination of credit checks and geographic barriers. Anyone with an internet connection and a wallet can participate as either a lender or a borrower.

To manage risk without human oversight, these loans are typically over-collateralized. This means a borrower must deposit more value than they intend to withdraw. If the value of the collateral drops below a specific threshold, the smart contract automatically liquidates the asset to repay the loan. This ensures the safety of the lender's capital without the need for debt collectors or legal intervention.

The Mechanics of Consensus and Staking

While DeFi replicates financial services, staking is fundamental to the operation of the blockchain itself. It is the process by which Proof of Stake networks maintain security and agreement. Staking is often compared to a high-yield savings account, but the underlying mechanics are vastly different. It involves active participation in the network's consensus protocol rather than simply lending money to a bank.

Proof of Stake Fundamentals

Proof of Stake (PoS) emerged as an alternative to the energy-intensive Proof of Work mechanism used by Bitcoin. In a PoS system, network validators are selected to create new blocks and confirm transactions based on the amount of cryptocurrency they have locked up, or "staked," in the network. This staked capital acts as a security deposit. It ensures that validators have a financial interest in following the rules.

If a validator attempts to validate fraudulent transactions or attacks the network, their staked assets can be penalized. This creates a strong economic incentive for honest behavior. The more assets that are staked on a network, the more expensive and difficult it becomes for any single actor to compromise the system. This relationship between economic value and network security is the cornerstone of modern blockchain design.

Validator Incentives and Delegation

For their service to the network, validators receive rewards. These rewards typically come from two sources: new issuance of coins (inflation) and transaction fees paid by users. This establishes a circular economy where the network pays those who secure it. However, running a validator node often requires technical expertise and significant hardware.

To make staking accessible to everyone, most PoS networks allow for delegation. This process enables everyday users to contribute their tokens to a validator of their choice without giving up custody of their assets. The validator performs the technical work, and the rewards are shared with the delegators. This system democratizes access to network rewards, allowing anyone with a compatible wallet to earn yield while contributing to blockchain security.

Evolution of Yield: Liquid Staking and Restaking

A significant limitation of traditional staking is illiquidity. When assets are staked, they are locked within the protocol, often for days or weeks. During this time, the user cannot trade, sell, or use that capital for other opportunities. This opportunity cost led to the development of liquid staking, a solution that unlocks the value of staked assets.

Solving Liquidity Constraints

Liquid staking protocols accept a user's deposit and stake it on their behalf. In return, the protocol issues a "receipt token" or Liquid Staking Token (LST) that represents the underlying deposit and the accumulating rewards. For instance, if a user deposits Ether into a liquid staking provider, they receive a token that holds equivalent value.

The critical innovation is that this new token is fully transferable and tradeable. Users can hold the LST to accrue staking rewards, or they can use it within the broader DeFi ecosystem. It can be used as collateral for a loan or traded on an exchange. This allows participants to earn staking yields without sacrificing the ability to move into or out of positions as market conditions change.

The Rise of Restaking

Building upon the foundation of liquid staking, a newer concept known as restaking has emerged. Restaking allows validators to utilize their staked capital to secure multiple protocols simultaneously. Traditionally, stake is committed to a single network. Restaking protocols enable that same capital to provide security for additional services, such as data availability layers, oracle networks, or bridges.

This mechanism improves capital efficiency significantly. Validators can earn rewards from the main blockchain and additional rewards from the secondary services they secure. It creates a marketplace for decentralized trust, where new applications can "rent" security from an established validator set rather than bootstrapping their own from scratch. However, this increased utility comes with increased responsibility, as validators must adhere to the rules of all connected protocols.

Decentralized Exchanges and Market Structure

The ability to trade assets without an intermediary is another pillar of the on-chain economy. Decentralized exchanges (DEXs) fundamentally change how markets are structured. In traditional markets, centralized entities control the order book and custody the assets. DEXs replace this with automated market makers and liquidity pools.

Automated Liquidity Provision

A liquidity pool is essentially a pile of funds locked in a smart contract. Users, known as liquidity providers (LPs), deposit pairs of assets into these pools. For example, an LP might deposit an equal value of a stablecoin and a volatile crypto asset. When a trader wants to swap one token for the other, they trade against the pool rather than a specific counterparty.

The smart contract automatically adjusts the price based on the ratio of assets in the pool. In exchange for providing the capital that makes trading possible, liquidity providers earn a portion of the trading fees. This model effectively crowdsources the role of the market maker. It allows anyone to earn fees on their idle assets, provided they are willing to accept the specific risks associated with automated market making.

Eliminating Counterparty Risk

The primary advantage of this model is the elimination of custodial risk. When trading on a centralized exchange, users must deposit funds into a wallet controlled by the company. If that company fails or is hacked, user funds are often lost. On a DEX, the trade happens directly between the user's wallet and the smart contract.

At no point does a third party take control of the assets. This "non-custodial" approach aligns with the broader ethos of cryptocurrency. It ensures that market access remains open and permissionless. There are no account freezes, withdrawal limits, or identity verification hurdles to trade. The code governs the interaction, ensuring transparency and equal access for all participants regardless of their location or status.

Navigating Risks in On-Chain Finance

While the opportunities for earning and participation are extensive, they are accompanied by distinct risks. The absence of intermediaries means there is no customer support to reverse a transaction or insurance fund to cover operational errors. Understanding these risks is a prerequisite for safe participation in staking and DeFi.

Technical and Contract Vulnerabilities

The most prevalent risk in DeFi is smart contract failure. While code is objective, it is written by humans and can contain bugs. Hackers often analyze open-source contracts to find loopholes that allow them to drain funds. Even audited projects—those reviewed by security firms—can suffer from exploits. A "rug pull" is another malicious scenario where developers intentionally leave backdoors in the code to steal user funds.

Users must also be wary of "phishing" DApps. These are fraudulent websites designed to look exactly like legitimate financial protocols. If a user connects their wallet to a phishing site, they may inadvertently sign a transaction that gives the attacker permission to drain their assets. verifying URLs and using trusted bookmarks are essential security habits for anyone navigating this space.

Operational Hazards in Staking

Staking carries its own set of risks, primarily centered around "slashing." Slashing is the penalty mechanism used by PoS networks to punish bad behavior. If a validator goes offline for too long or validates incorrect transactions, the network may confiscate a portion of the staked tokens. This penalty affects both the validator and the users who delegated to them.

Furthermore, liquidity is a major consideration. Standard staking often imposes a strict unbonding period. During this time, which can last weeks, assets cannot be withdrawn or sold. If the market crashes during an unbonding period, the user is forced to hold the asset until the unlock is complete. Liquid staking mitigates this but introduces smart contract risk associated with the liquid staking provider.

| Risk Category | Staking | DeFi / Yield Farming |

|---|---|---|

| Principal Loss | Slashing events (Validator error) | Smart contract bugs or exploits |

| Liquidity | Locked during unbonding period | Generally liquid (unless specified) |

| Complexity | Low (Native) to Medium (Liquid) | High (Impermanent loss, strategies) |

The Wallet as a Control Center

The self-custodial wallet has evolved from a passive vault into the primary interface for the Web3 economy. It serves as the bridge between the user and the various blockchain protocols. By controlling their own private keys, users retain absolute authority over their assets. This control is the foundation upon which all decentralized interaction is built.

The Importance of Self-Custody

"Not your keys, not your coins" remains a defining mantra of the industry. When assets are left on a centralized exchange, the user is essentially holding an IOU. The exchange decides when withdrawals are processed and which assets are supported. A self-custodial wallet removes this dependency. It empowers the user to interact directly with the blockchain.

This autonomy is critical for accessing DeFi and staking. Most decentralized applications generally do not allow connections from centralized exchange accounts. To use a DEX, stake in a protocol, or vote in a DAO, one must connect via a personal wallet. This puts the full spectrum of financial utility directly in the hands of the individual, removing the friction of intermediary approval.

Connecting to Protocols

Modern wallets have integrated browsers or connection protocols like WalletConnect to streamline interactions. When a user visits a DeFi application, the wallet acts as a digital identity and signing device. The application requests permission to view balances or initiate transactions, and the wallet requires the user to approve each action.

This handshake ensures that the user remains in control of every transfer. The integration has become seamless enough that staking often requires just a few taps within the wallet interface itself. Many wallets now offer native staking features, where the complex backend interactions with smart contracts are abstracted away into a simple "Stake" button. This lowers the barrier to entry, allowing non-technical users to participate in complex earning strategies.

Conclusion

The integration of staking and decentralized finance into consumer wallets represents a maturation of the cryptocurrency ecosystem. It moves the industry beyond speculation and into the realm of functional utility. By leveraging smart contracts, users can now access financial services that are transparent, automated, and permissionless. Whether through securing a network via staking or providing liquidity on a decentralized exchange, the opportunities to put capital to work are vast and accessible.

However, this increased power necessitates a heightened level of responsibility. The risks of smart contract bugs, slashing penalties, and operational errors are real and must be managed through education and vigilance. The shift to self-custody removes the safety net of traditional finance, placing the onus of security squarely on the individual. As the technology continues to evolve, the line between a simple wallet and a comprehensive financial institution will continue to blur.

Self-custody wallets turn passive holders into active participants by directly connecting assets to yield-bearing protocols.