The digital asset landscape has evolved significantly from its early days of speculative frenzy into a mature ecosystem offering sophisticated tools for wealth accumulation. For investors looking to build value over the long term, the focus often shifts from day-to-day price action to strategic portfolio growth and efficiency. By utilizing methods that prioritize steady accumulation and passive yield generation, investors can navigate the inherent volatility of the market while positioning themselves for future appreciation.

Developing a comprehensive strategy requires understanding the mechanisms that drive market movements and the tools available to mitigate risk. Long-term success is rarely the result of a single lucky trade. Instead, it stems from disciplined habits, a deep understanding of asset utility, and the ability to leverage financial products that preserve capital. Whether through automated buying schedules or lending protocols, the goal remains consistent: maximizing asset growth while minimizing unnecessary exposure to market timing risks.

The Fundamentals of Dollar-Cost Averaging

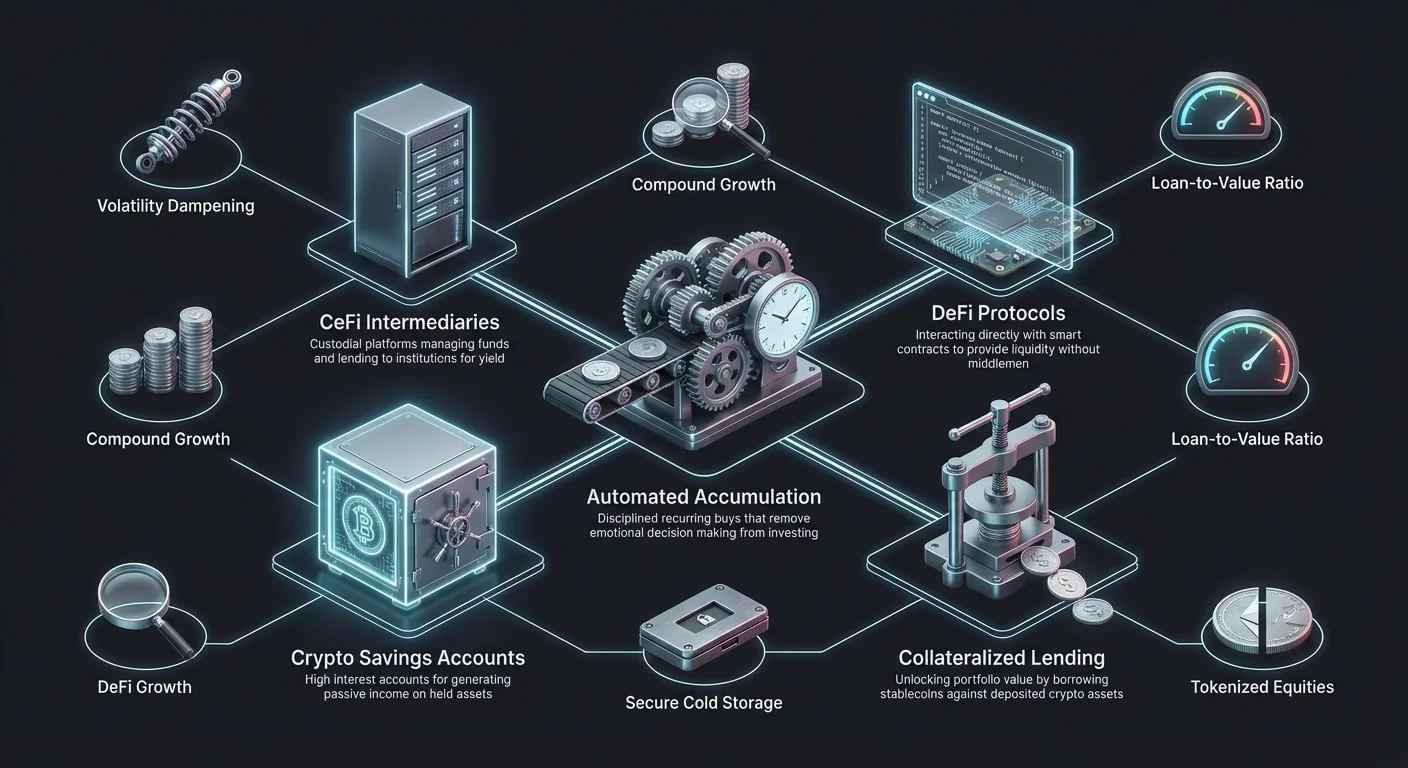

Dollar-cost averaging (DCA) stands as a foundational strategy for investors seeking to build a position in cryptocurrencies without succumbing to the stress of market timing. This approach involves investing a fixed amount of money at regular intervals, regardless of the asset's current price. By spreading purchases over time, investors naturally buy more units when prices are low and fewer units when prices are high.

Mitigating Market Volatility

Volatility refers to the frequency and magnitude of price fluctuations in a market. In the cryptocurrency space, volatility is often higher than in traditional financial markets due to the industry's relative youth and smaller liquidity pools. Rapid price changes can be driven by news cycles, economic events, or shifts in market sentiment. For a lump-sum investor, this volatility poses a significant risk. If a large capital deployment occurs immediately before a market downturn, the portfolio's value drops instantly.

DCA specifically targets this risk by smoothing out the entry price. Since the investment is broken into smaller chunks over weeks, months, or years, the impact of any single price drop is diluted. The average cost per coin potentially ends up lower than the asset's average market price over the same period, as the fixed fiat amount acquires more digital assets during bearish trends. This approach transforms volatility from a threat into an opportunity for accumulation.

The Psychology of Discipline

One of the most challenging aspects of investing is managing emotional responses to market movements. The fear of missing out (FOMO) often drives investors to buy at peaks, while panic leads to selling at bottoms. DCA removes the emotional component from the decision-making process. By committing to a schedule, the investor essentially automates their behavior, ensuring that they remain active participants in the market regardless of the prevailing sentiment.

This discipline is crucial for long-term wealth accumulation. It prevents the paralysis that often strikes when prices are falling. Instead of trying to predict the absolute bottom—a feat difficult even for professional traders—the DCA investor continues to accumulate. Over time, this consistency harnesses the power of compounding, allowing the portfolio to grow exponentially as assets are held and potentially reinvested.

Preserving Optionality

Investing a large lump sum commits all available capital to a single moment in time. This removes flexibility. If the market structure changes or new opportunities arise shortly after the purchase, the investor has no "dry powder" left to react. DCA preserves optionality by keeping a portion of capital in cash reserves, deployed slowly over time.

This flexibility prevents the investor from being overly committed to a single course of action. It allows for adaptation. If the market fundamentals shift drastically, the investor can pause or adjust their strategy without having risked their entire principal in one go. Maintaining options is a key component of risk management, ensuring that the investor is never backed into a corner by an ill-timed decision.

Analyzing DCA Performance Scenarios

To understand the mathematical advantage of dollar-cost averaging, it is helpful to look at historical examples of market extremes. Predicting peaks and troughs is notoriously difficult, and "buying the top" is a common fear. However, historical data suggests that a disciplined DCA strategy can mitigate the damage of entering the market at an unfavorable time.

Consider a scenario where an investor buys at a market peak. If a lump-sum purchase is made at the absolute height of a cycle, and the market subsequently corrects, the portfolio may remain underwater for an extended period. The investor faces a significant unrealized loss. However, if that same investor had split their capital into weekly purchases starting at the peak, they would have continued buying as the price fell.

In this DCA scenario, the average entry price decreases significantly as the market corrects. Even if the asset price has not returned to the previous all-time high after a few years, the DCA investor might still be in profit because they accumulated the majority of their holdings at much lower prices during the bear market. The lump-sum investor, by contrast, requires the price to fully recover just to break even.

The strategy also performs well during "catching the bottom" attempts. While a perfectly timed lump sum at the absolute bottom yields the highest theoretical return, identifying that bottom in real-time is speculative gambling. A DCA strategy started near the bottom captures much of the upside while protecting against the possibility that the price could drop further. It provides a balanced approach that sacrifices the theoretical maximum of perfect timing for the practical safety of average pricing.

| Scenario | Lump Sum Outcome | DCA Outcome |

|---|---|---|

| Buying the Peak | High risk of long-term loss | Lowers average cost, faster recovery |

| Market Downturn | Significant unrealized losses | Accumulates more assets at discount |

| Market Recovery | Requires full price rebound | Profitable before reaching previous highs |

Automated Investing and recurring Buys

The evolution of crypto exchanges has made implementing DCA strategies easier through automation. Auto DCA, or recurring buy features, allow users to set parameters once and let the platform execute trades. This "set it and forget it" model ensures that the schedule is adhered to without requiring manual intervention or constant monitoring of price charts.

Eliminating Execution Risk

Manual investing introduces execution risk. An investor might intend to buy every Friday, but they might forget, be busy, or hesitate because they think the price might drop further in an hour. Automation removes these variables. The system executes the buy order at the pre-determined interval—daily, weekly, or monthly—regardless of external factors. This consistency is vital for the strategy's success.

Automated tools also allow for precise budget management. Investors can align their crypto purchases with their income cycles, such as scheduling buys to occur immediately after a paycheck is deposited. This treats investment as a mandatory expense similar to rent or utilities, prioritizing wealth building before discretionary spending can deplete available funds.

Customization and Flexibility

Modern platforms offer significant flexibility in how these automated strategies are structured. Investors are not locked into rigid contracts. They can usually pause, adjust, or cancel the recurring buys at any time. If financial circumstances change, the investment amount can be lowered. If a bonus is received, the amount can be temporarily increased.

Furthermore, Auto DCA is not limited to a single asset. Investors can often set up automated purchases for a basket of cryptocurrencies, ensuring portfolio diversification. By splitting the recurring investment across Bitcoin, Ethereum, and other assets, the investor mitigates the risk associated with any single project failing while maintaining exposure to the broader market growth.

Generating Yield Through Savings Accounts

Holding cryptocurrency for the long term does not mean the assets must sit idle. Crypto savings accounts have emerged as a primary method for generating passive income on held assets. These accounts function similarly to traditional bank savings accounts but often offer significantly higher interest rates, reflecting the different risk profiles and economic mechanics of the crypto industry.

CeFi vs. DeFi Yield Options

Yield generation generally falls into two categories: Centralized Finance (CeFi) and Decentralized Finance (DeFi). CeFi platforms are custodial entities that manage the funds on behalf of the user. They act as intermediaries, lending out user deposits to institutions or other borrowers and passing a portion of the interest back to the depositor. This offers a user experience similar to traditional banking, often with customer support and easier interface navigation.

DeFi protocols, conversely, operate through smart contracts on a blockchain. Users interact directly with the code, providing liquidity to pools or lending markets without a central company managing the transaction. DeFi can offer higher transparency and potentially higher yields since there is no middleman taking a cut. However, it requires a higher level of technical proficiency and places the responsibility of security entirely on the user.

Fixed vs. Flexible Terms

When depositing assets into a savings account, investors often face a choice between flexible and fixed terms. Flexible accounts allow users to withdraw their funds at any time. This liquidity is valuable for investors who may need to access their capital on short notice or who wish to sell if the market heats up. The trade-off is typically a lower annual percentage yield (APY).

Fixed-term accounts require the user to lock their assets for a specific duration, such as 30, 60, or 90 days. In exchange for this commitment, the platform offers a higher interest rate. This option is best suited for long-term holders who have no intention of selling in the near future and want to maximize their passive returns. It enforces a "forced HODL" strategy, which can prevent impulsive selling during minor market dips.

Crypto Lending and Borrowing Strategies

Beyond simple savings accounts, the crypto lending market provides sophisticated tools for capital efficiency. Crypto loans allow investors to borrow fiat currency or stablecoins using their crypto holdings as collateral. This mechanism unlocks the value of the portfolio without requiring the sale of the underlying assets.

Tax Efficiency of Borrowing

One of the most significant advantages of crypto-backed loans is the potential for tax efficiency. In many jurisdictions, selling cryptocurrency is a taxable event that triggers capital gains tax. If an investor has held an asset for years and it has appreciated significantly, selling it to access cash results in a tax liability that reduces the net gain.

Borrowing against the asset, however, is generally not considered a sale. The investor retains ownership of the cryptocurrency while receiving liquidity in the form of a loan. Since no sale occurred, no capital gains tax is typically triggered at the time of the loan. This allows long-term investors to access liquidity for lifestyle expenses or other investment opportunities while deferring the tax obligations associated with selling.

Understanding Loan-to-Value (LTV)

The Loan-to-Value (LTV) ratio is a critical concept in crypto lending. It represents the percentage of the collateral's value that is being borrowed. For example, if an investor deposits $10,000 worth of Bitcoin and takes out a $5,000 loan, the LTV is 50%. Platforms set maximum LTV limits to protect themselves from market volatility.

Lower LTV ratios generally secure better interest rates and lower the risk of liquidation. If the value of the collateral drops, the LTV increases. If it hits a critical threshold, the platform may issue a margin call, requiring the borrower to add more collateral or repay part of the loan. If the borrower fails to do so, the platform will liquidate (sell) the collateral to cover the debt.

Collateralized vs. Uncollateralized Loans

The majority of crypto loans are collateralized. This security allows lenders to offer loans without credit checks, as the risk is covered by the assets held in escrow. The transaction is trustless in nature; the lender does not need to know the borrower's financial history, only that the collateral is sufficient.

Unsecured or uncollateralized loans are rarer and typically resemble traditional finance products. They require thorough credit assessments and identity verification. Because there is no asset backing the loan, interest rates are usually higher to compensate for the increased risk to the lender. For most crypto-native investors, collateralized loans remain the primary tool for liquidity access.

| Feature | Collateralized Loans | Unsecured Loans |

|---|---|---|

| Security Required | Yes (Crypto assets) | No (Creditworthiness) |

| Interest Rates | Typically Lower | Typically Higher |

| Approval Process | Fast / Instant | Slower / Credit Check |

Navigating Risks in Yield Strategies

While generating yield and borrowing against assets offer clear benefits, they introduce specific risks that differ from simple cold storage holding. Understanding these dangers is essential for preserving the principal investment.

Platform and Counterparty Risk

When using CeFi platforms for savings or lending, the investor is exposed to counterparty risk. This is the risk that the platform itself becomes insolvent, is managed poorly, or acts maliciously. If a centralized lender fails, user deposits may be frozen or lost. Unlike traditional bank accounts, these deposits are often not insured by government programs.

DeFi protocols carry smart contract risk. While there is no central company to fail, bugs or vulnerabilities in the code can be exploited by hackers. If a smart contract is drained, there is rarely a recourse for recovering funds. Investors must conduct due diligence, checking for audits and the protocol's track record before depositing significant capital.

Liquidation Cascades

For borrowers, the primary risk is liquidation driven by market volatility. A sudden flash crash can drop the value of collateral significantly in minutes. If the LTV spikes above the liquidation threshold, the protocol or platform will automatically sell the assets. This often happens at the bottom of the market, meaning the investor loses their holdings at the worst possible price.

To mitigate this, prudent borrowers maintain a healthy buffer in their LTV ratio. Rather than borrowing the maximum amount allowed, they might borrow only 20% or 30% of the collateral's value. This provides a safety margin that allows the asset price to fluctuate significantly without triggering a forced sale.

Diversification with Tokenized Stocks

Tokenized stocks represent a convergence of traditional finance and blockchain technology. These are digital tokens that track the price performance of publicly traded equity shares. For crypto investors, they offer a method to diversify a portfolio beyond cryptocurrencies without leaving the blockchain ecosystem.

24/7 Market Access

Traditional stock markets operate within rigid hours, typically closing in the evenings and on weekends. Tokenized stocks, residing on blockchains, can often be traded 24/7. This continuous liquidity allows investors to react to news or economic events immediately, rather than waiting for the market bell to ring on Monday morning.

This feature is particularly valuable for global investors who may be in different time zones than the stock exchange where the underlying company is listed. It democratizes access, allowing a user in Asia to trade US tech stocks during their own daylight hours with the same ease as trading Bitcoin.

Fractional Ownership

High share prices of major technology or holding companies can be a barrier to entry for smaller investors. Tokenized stocks often support fractional ownership. An investor does not need to buy a whole share; they can purchase a fraction of a token representing $10 or $50 worth of the company.

This granularity enables precise portfolio construction. An investor can allocate exact dollar amounts to specific equities, creating a balanced portfolio regardless of the individual share prices. It mirrors the accessibility of crypto assets, where one can buy a fraction of a Bitcoin, applying that same logic to the stock market.

Selecting the Right Exchange Infrastructure

The choice of platform is a critical decision that underpins all other strategies. The exchange serves as the gateway for DCA, the custodian for savings, and the interface for lending. Factors such as security, fees, and liquidity directly impact the efficiency of long-term investing.

Evaluating Security Protocols

Security is the paramount concern. Top-tier exchanges employ robust measures such as cold storage, where the majority of user funds are kept offline, disconnected from the internet. This makes them inaccessible to remote hackers. Two-factor authentication (2FA) is a standard requirement, adding a layer of protection to user accounts.

Proof of Reserves has become an increasingly important metric. Transparent exchanges publish data verifying that they hold the assets they claim to hold on behalf of their users. This transparency reassures investors that the exchange is solvent and not misusing customer funds for speculative activities.

Fee Structures and Liquidity

Fees erode long-term returns. Investors must analyze the fee schedule of their chosen platform, looking at both trading fees (maker/taker) and withdrawal fees. Some platforms offer lower trading fees but charge high amounts to move crypto off the exchange. For a DCA strategy involving frequent small purchases, high transaction fees can significantly drag down performance.

Liquidity ensures that trades execute quickly and at the expected price. High liquidity means there are many buyers and sellers active on the platform. This prevents "slippage," where a large order moves the price disadvantageously before it is fully filled. For investors dealing with larger sums or less common assets, deep liquidity is essential for entering and exiting positions efficiently.

The Role of Custody in Long-Term Holding

For long-term investors, the question of where to store assets is vital. While exchanges offer convenience and yield opportunities, they introduce third-party risk. Self-custody involves holding assets in a private wallet where the user controls the private keys.

Hardware Wallets vs. Exchange Wallets

Hardware wallets are physical devices that store private keys offline. They provide the highest level of security against online threats. For the portion of a portfolio that is not actively generating yield or being used as collateral, cold storage via a hardware wallet is often recommended. It eliminates the risk of an exchange collapse affecting those specific assets.

Exchange wallets (custodial wallets) are necessary for participating in savings programs or setting up Auto DCA. The trade-off is between security and utility. A balanced approach often involves keeping a "working stack" on exchanges for yield and liquidity, while moving the "vault stack" of long-term holdings to self-custody.

Assisted Self-Custody

Some modern platforms offer hybrid models or "vault" services. These solutions aim to combine the security of self-custody with the recovery options of a managed service. They may use multi-signature technology, where multiple keys are required to move funds. The user holds one key, the institution holds another, and a third allows for recovery. This prevents a single point of failure while ensuring that the user maintains a degree of sovereignty over their assets.

Optimizing Cost Efficiency

Tax efficiency is not just about government levies; it is about minimizing all costs that reduce net value. "Cash drag" is a phenomenon where capital sits uninvested, earning zero returns while inflation erodes its purchasing power. In a DCA strategy, holding cash between intervals can create drag.

Minimizing Transaction Costs

Frequent trading or transferring creates a trail of fees. Using an exchange that offers low-fee recurring buys helps. Additionally, understanding network fees is crucial. Transferring Ethereum or Bitcoin during times of high network congestion can be expensive. Long-term investors should time their withdrawals to self-custody during periods of low network activity to save on gas fees.

Using native exchange tokens can sometimes reduce trading fees. Many platforms incentivize the use of their proprietary token by offering discounts on maker/taker fees. For a high-frequency DCA strategy, these small savings compound over years, preserving a noticeable amount of capital.

Managing Spread Costs

"Spread" is the difference between the buying price and the selling price. Some brokerage-style platforms charge zero explicit fees but hide their profit in a wide spread. This means the investor buys at a price slightly higher than the market rate. Over time, paying a 1% spread on every DCA purchase is more expensive than paying a 0.5% transparent trading fee. Investors should verify the actual execution price against the spot market price to ensure they are not overpaying for the convenience of a "fee-free" interface.

Conclusion

Building wealth in the cryptocurrency market is a marathon that rewards patience, discipline, and strategic planning. By adopting Dollar-Cost Averaging, investors neutralize the chaos of short-term volatility and remove the emotional burden of market timing. This mechanical approach ensures consistent accumulation, turning market downturns into opportunities rather than setbacks. When combined with automation, DCA becomes a powerful tool for effortless portfolio growth.

Yield generation strategies, such as crypto savings accounts and lending protocols, further enhance capital efficiency. They allow idle assets to work for the investor, compounding returns over time. Furthermore, the strategic use of crypto-backed loans provides a mechanism to access liquidity without triggering taxable sales events, preserving the long-term upside of the portfolio. However, these tools must be used with a clear understanding of the associated risks, including platform solvency and liquidation thresholds.

Ultimately, the most effective strategy is one that balances growth with security. Diversifying through tokenized stocks, selecting reputable exchange infrastructure, and managing custody risks are all essential components of a robust investment plan. By minimizing fees, optimizing tax implications through strategic borrowing, and maintaining a long-term horizon, investors can navigate the complexities of the digital asset space with confidence.

Consistent automated accumulation combined with strategic yield generation creates the most reliable path to long-term crypto wealth.