High-frequency trading and scalping in the cryptocurrency market represent the pinnacle of technical execution and strategic precision. These trading styles rely on capitalizing on minute price movements over short timeframes, often executing hundreds or thousands of trades within a single day. Success in this arena is not merely a matter of predicting market direction. It depends heavily on the underlying infrastructure used to execute orders. The connection between a trader's algorithm and the exchange's matching engine is the critical lifeline for algorithmic execution.

For traders operating at this velocity, the standard web interface or mobile application is insufficient. These tools are designed for human reaction times and casual investment. Scalping requires the use of Application Programming Interfaces, or APIs. An API allows automated software to interact directly with an exchange. This direct link facilitates the rapid retrieval of market data and the immediate placement of orders. It removes the friction of manual entry and allows for strategies that react to market changes in milliseconds.

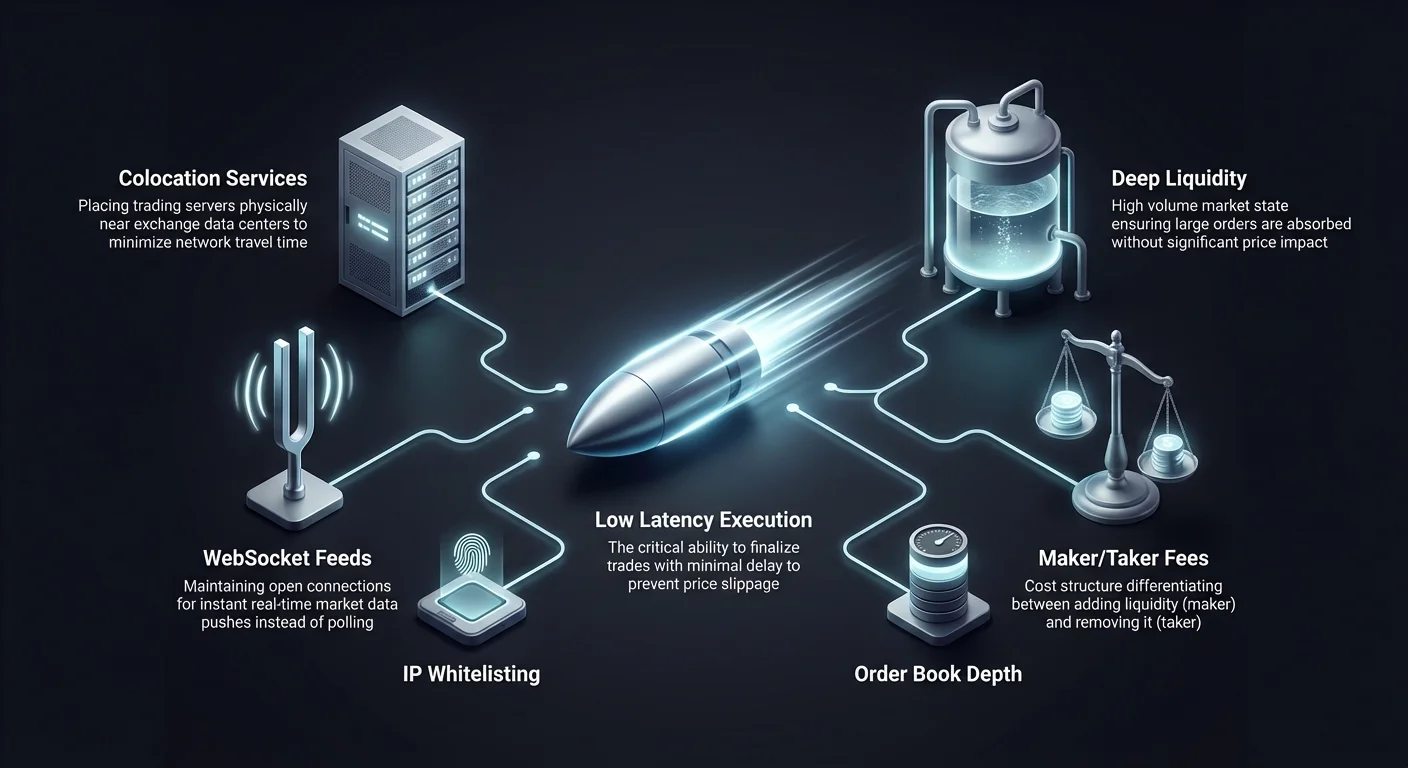

Optimizing this execution channel involves understanding the nuances of exchange architecture. Traders must evaluate platforms based on specific technical criteria rather than marketing promises. Factors such as API rate limits, latency, liquidity depth, and fee structures become the primary determinants of profitability. A platform that works well for a long-term holder may be disastrous for a high-frequency trader due to lag or excessive costs. We must prioritize exchange latency and uptime.

The Mechanics of Algorithmic Execution

Algorithmic trading automates the process of buying and selling assets based on predefined criteria. In the context of high-frequency trading, these algorithms are designed to detect micro-patterns in market behavior. They might look for imbalances in the order book or fleeting arbitrage opportunities between pairs. Once a signal is identified, the system must act instantly. The efficiency of this action is determined by the quality of the exchange's API documentation and stability.

The technical sophistication of the exchange's matching engine plays a vital role here. A matching engine is the software core of an exchange that pairs buy and sell orders. For high-frequency strategies, this engine must be capable of processing thousands of orders per second without buckling under load. If the engine lags during periods of high volatility, the algorithm's edge is lost. Traders often look for platforms that boast high-performance matching engines capable of executing trades in microseconds.

Latency and Connection Stability

Latency refers to the time delay between a request being sent and the action being executed. In scalping, latency is the enemy. A delay of even a few hundred milliseconds can result in price slippage, where the executed price is worse than the expected price. This erosion of value can turn a profitable trade into a loss.

API stability is equally important. High-frequency strategies rely on a continuous stream of data. If the API connection drops or times out, the trading bot is effectively blind. Reliability metrics and historical uptime data are crucial when selecting a venue for algorithmic trading.

Analyzing Liquidity and Order Book Depth

Liquidity is a measure of how easily an asset can be bought or sold without affecting its price. For scalpers and high-frequency traders, deep liquidity is non-negotiable. It ensures that large orders can be absorbed by the market without causing significant price shifts. A thin order book leads to slippage, which directly eats into the razor-thin margins that scalpers target.

The Impact of Volume on Execution

High trading volume is often a proxy for liquidity. Exchanges with substantial daily volume typically attract more market makers and institutional participants. This activity creates a dense order book with tight spreads between the highest bid and the lowest ask. A tight spread is essential for scalping strategies that aim to capture small price increments. If the spread is too wide, the price must move significantly just for the trade to break even.

Slippage Mitigation Strategies

To mitigate the risk of slippage, traders analyze the depth of the order book. This involves looking at the volume of pending buy and sell orders at various price levels. A deep order book acts as a buffer against volatility. It allows high-frequency algorithms to enter and exit positions rapidly with minimal price impact. Platforms known for high liquidity are often preferred for this reason.

| Liquidity Feature | Benefit to Scalper | Risk of Deficiency |

|---|---|---|

| Tight Spreads | Reduces breakeven cost | Higher transaction costs |

| High Volume | Faster order filling | Slow execution times |

| Deep Order Book | Minimizes price slippage | Significant price impact |

Understanding Fee Structures

Transaction fees are the primary cost of doing business for high-frequency traders. Since scalpers execute a vast number of trades to accumulate small profits, fees can quickly outpace gains. Understanding the distinction between maker fees and taker fees is fundamental to strategy optimization.

Exchanges typically differentiate between liquidity makers and liquidity takers. A "maker" places an order that does not fill immediately, such as a limit order below the current price. This adds liquidity to the order book. A "taker" places an order that fills immediately, usually a market order, removing liquidity. Exchanges often incentivize makers with lower fees to encourage a healthy order book. Scalpers who use limit orders can significantly reduce their overhead by targeting maker fee tiers.

Volume-Based Discounts

Many platforms offer tiered fee structures based on 30-day trading volume. As a trader's volume increases, their fee percentage decreases. For high-frequency traders, reaching these upper tiers is essential for long-term viability. Some platforms even offer rebates to high-volume makers, effectively paying the trader to provide liquidity.

Zero-Fee Trading Environments

The emergence of zero-fee trading options has altered the landscape for some scalping strategies. These platforms eliminate commission costs on specific trading pairs, such as Bitcoin or stablecoin pairs. This allows traders to execute frequent transactions without the burden of per-trade fees.

Strategic Implications of No Fees

In a zero-fee environment, the break-even point for a trade is lower. A trader only needs the price to move enough to cover the spread. This opens up opportunities for strategies that target extremely small price movements which would be unprofitable on a fee-charging exchange. However, traders must remain vigilant about other potential costs, such as wider spreads or withdrawal fees, which might offset the benefit of zero commissions.

Asset Selection in Zero-Fee Zones

Zero-fee promotions often apply to specific high-volume pairs. Traders must ensure that the assets they intend to scalp are eligible for these benefits. Strategies often focus on major pairs like BTC/USDT or ETH/USDT where liquidity is highest and fees are waived. This concentration of activity can create highly competitive but potentially lucrative environments for algorithmic execution.

Grid Trading as an HFT Strategy

Grid trading is a specific type of automated strategy that fits well within the high-frequency domain. It involves placing a series of buy and sell orders at predefined price intervals within a specific range. As the price fluctuates, the system automatically executes these orders, profiting from the volatility.

Automating Volatility Capture

Grid trading bots are particularly effective in sideways or ranging markets where prices oscillate without a strong trend. The bot buys when the price dips to a grid line and sells when it rises to the next level. This systematic approach removes emotional decision-making and ensures that the strategy capitalizes on every minor market movement. The frequency of trades depends on the density of the grid lines; tighter intervals result in more frequent execution.

Configuring Grid Parameters

Successful grid trading requires precise configuration. Traders must determine the upper and lower limits of the grid and the number of grid lines. A dense grid with many lines will execute more trades, requiring a platform with low fees and high stability. If the exchange's API is slow, the bot may miss rapid price swings, failing to execute the grid orders effectively.

Leveraging Derivatives for Scalping

Derivatives markets, particularly futures and perpetual swaps, are heavily utilized by high-frequency traders. These instruments allow for the use of leverage, which amplifies the potential returns from small price movements. In scalping, where the target profit per trade is often less than 1%, leverage can make these small gains meaningful.

Perpetual Swaps and Funding Rates

Perpetual swaps are contracts that mimic the spot price but do not have an expiration date. They use a mechanism called the funding rate to keep the contract price anchored to the spot price. High-frequency algorithms often incorporate funding rate arbitrage into their strategies. They may also use the deep liquidity found in derivatives markets to execute larger positions than would be possible in the spot market.

Risk Management with Leverage

While leverage increases profit potential, it also magnifies risk. Automated systems must have robust risk management logic to prevent liquidation. This includes setting strict stop-loss orders and managing margin requirements dynamically. Exchanges that offer flexible margin modes and real-time risk data via API are essential for safely navigating leveraged scalping.

Centralized Exchange Architecture

Centralized exchanges (CEXs) remain the primary venue for high-frequency trading due to their superior speed and liquidity. In a CEX model, the exchange hosts the order book and matches trades on its own servers. This centralization allows for execution speeds that decentralized blockchains currently cannot match.

Matching Engine Performance

The performance of a CEX is defined by its matching engine. Top-tier exchanges invest heavily in infrastructure to ensure their engines can handle surges in activity. For an API trader, the metric to watch is "orders per second" (OPS). A high OPS capacity suggests the platform can maintain low latency even during market crashes or pumps.

Institutional-Grade Tools

Many centralized platforms cater specifically to algorithmic traders by offering institutional-grade features. These may include colocation services, where the trader's server is physically located near the exchange's server to minimize network travel time. Additionally, CEXs often provide more comprehensive historical data via API, allowing traders to backtest their algorithms against accurate past market behavior.

Decentralized Execution and AMMs

Decentralized exchanges (DEXs) operate on different principles. Instead of a central matching engine, they often use Automated Market Makers (AMMs). While generally slower than CEXs due to block times, they offer unique opportunities for specific types of algorithmic trading, such as arbitrage between pools.

On-Chain Latency Factors

Trading on a DEX involves interacting directly with a blockchain. Execution speed is limited by the network's block time and congestion levels. For true high-frequency scalping, this latency is often prohibitive. However, the transparency of on-chain data allows for strategies that analyze pending transactions in the mempool, a technique known as MEV (Maximum Extractable Value).

Gas Fees and Efficiency

On a DEX, every trade incurs a network gas fee. This introduces a variable cost that can destroy the profitability of high-frequency strategies. Automated traders on DEXs must incorporate gas price optimization into their algorithms. They often focus on networks with low transaction costs and high throughput to make frequent trading viable.

Security Protocols for API Keys

Using an API requires generating unique keys that grant access to an account. These keys are sensitive credentials. If they fall into the wrong hands, a malicious actor could execute unauthorized trades. Security hygiene is paramount for anyone engaging in automated trading.

Traders should configure API keys with the principle of least privilege. Most exchanges allow users to set specific permissions for each key. For a trading bot, the key should have permission to "read" data and "trade" but should never have permission to "withdraw" funds. This ensures that even if the key is compromised, the funds cannot be stolen directly.

IP whitelisting is another critical security layer. This feature restricts API access to specific IP addresses. By linking the API key to the static IP address of the trading server, the trader ensures that requests from any other location are automatically rejected. This blocks external attackers from using stolen keys.

Market Making and Rebate Strategies

Market making is a strategy where a trader provides liquidity to the market by placing both buy and sell orders simultaneously. The trader profits from the spread—the difference between the buy and sell price. This is a core component of high-frequency trading ecosystems.

Capturing the Spread

Market makers rely on the continuous flow of orders to earn the spread repeatedly throughout the day. This strategy requires an extremely stable API connection. The market maker must constantly update their orders to reflect changing market prices. If the connection lags, the maker's orders might be executed at an unfavorable price, leading to losses known as "toxic flow."

Exchange Rebates

To attract market makers, exchanges often offer rebates on maker fees. Instead of paying a fee, the trader receives a small percentage of the trade value. For high-frequency market makers, these rebates can form a significant portion of total profitability. Selecting an exchange with a favorable rebate program is a strategic decision for liquidity providers.

Evaluating Exchange Reliability

Uptime is a non-negotiable metric for automated trading. A platform that goes offline during periods of high volatility prevents traders from exiting positions, potentially leading to catastrophic losses. Reliability extends beyond just the website being accessible; the API endpoints must remain responsive.

Traders should investigate an exchange's historical status pages and community reports regarding downtime. Frequent "maintenance" windows during critical market hours are a red flag. The best platforms for high-frequency trading are those that have redundant systems and a proven track record of stability under stress.

The Impact of Latency on Profitability

In the realm of high-frequency trading, physical distance matters. Data travels at the speed of light, but it still takes time to move between a trader's server and the exchange's data center. This travel time contributes to network latency.

Server Location Strategies

Serious algorithmic traders often rent servers located in the same geographic region or data center as the exchange. This proximity minimizes the physical distance data must travel. Some exchanges disclose their server locations to assist traders in optimizing their setups. Reducing latency by even a few milliseconds can provide a competitive advantage in filling orders before other market participants.

WebSocket vs. REST APIs

The method of data retrieval also affects speed. REST APIs require the trader to send a request for data and wait for a response. WebSocket APIs, in contrast, maintain an open connection and push data to the trader instantly as it happens. For high-frequency trading, WebSockets are superior because they provide real-time updates with lower overhead.

Choosing Platforms for Algo Trading

Selecting the right exchange is a multifaceted decision. Beyond technical specs, the quality of the developer experience matters. Good documentation is essential for building robust algorithms. It should be clear, comprehensive, and provide examples for various endpoints.

Support and Community

Technical issues are inevitable. When an API endpoint returns an error or a connection fails, responsive support is vital. Exchanges that cater to algorithmic traders often have dedicated support channels for developers. An active community of developers can also be a valuable resource for troubleshooting and sharing best practices.

Testing Environments

Before deploying real capital, traders need a safe space to test their algorithms. Top exchanges provide "sandbox" or "paper trading" environments. these mimic the live market but use virtual funds. A high-fidelity sandbox allows traders to verify their logic and connection stability without financial risk.

Risk Management in Automated Systems

Automation brings efficiency, but it also introduces the risk of runaway errors. A bug in the code could theoretically drain an account in minutes if not checked. Robust risk management protocols must be hard-coded into the trading system.

Stop-Loss and Kill Switches

Every automated strategy should have defined exit points. A stop-loss order acts as a safety net, closing a position if losses exceed a certain threshold. Additionally, a global "kill switch" is a necessary fail-safe. This feature monitors the system's overall performance and halts all trading activity if it detects abnormal behavior, such as a rapid succession of losing trades.

Position Sizing Logic

Algorithms must also manage position sizing dynamically. Betting too large on a single trade can lead to ruin. The code should calculate the appropriate trade size based on the current account balance and the calculated risk of the specific setup. This discipline ensures that the trading capital can withstand streaks of losses, which are statistically inevitable in high-frequency trading.

Tokenized Assets in HFT

While cryptocurrencies are the primary focus, the technology of high-frequency trading is expanding into tokenized representations of traditional assets. Tokenized stocks allow traders to apply crypto-native algorithmic strategies to equity markets. These tokens track the price of real-world shares but trade on crypto rails.

This opens up new avenues for HFT strategies that are not bound by traditional stock market hours. Since crypto exchanges operate 24/7, tokenized stocks allow for continuous trading. This is particularly useful for reacting to news events that occur outside of standard banking hours. However, traders must be aware of the liquidity differences between the tokenized asset and the underlying stock.

Geographic and Regulatory Factors

The location of the trader and the regulatory status of the exchange can impact the viability of high-frequency strategies. Some jurisdictions impose strict rules on leverage or derivatives trading. Others may restrict access to certain exchanges entirely.

Compliance and KYC

Most centralized exchanges require Identity Verification (KYC) to access higher withdrawal limits and advanced features. For institutional-level HFT, this compliance is mandatory. Traders must ensure they are legally permitted to use the chosen platform and that the exchange complies with relevant regulations to avoid sudden service interruptions.

Regional Restrictions

Certain features, such as high leverage or specific token pairs, may be geo-restricted. An algorithm designed to trade perpetual swaps might fail if the trader connects from a jurisdiction where those products are banned. Checking the terms of service regarding supported regions is a critical step in the setup process.

Conclusion

Optimizing API execution for high-frequency trading and scalping is a discipline that merges financial strategy with software engineering. The choice of exchange is fundamental to this process. Traders must look beyond user interfaces and marketing claims to evaluate the core technical performance of the platform. Key metrics such as matching engine speed, API latency, and liquidity depth dictate whether a strategy can be executed successfully.

Furthermore, the economic structure of the exchange, including fee tiers and rebate programs, plays a massive role in the net profitability of high-frequency strategies. By leveraging features like zero-fee pairs, colocation, and advanced order types, traders can sharpen their edge. However, this power comes with the responsibility of rigorous risk management and security practices. The integration of robust code, secure API management, and a reliable exchange partner forms the foundation of a successful automated trading operation.

Successful HFT relies on minimizing latency, maximizing liquidity, and optimizing fee structures through robust API integration.