The Ethereum network functions as a vast, decentralized computer capable of processing complex applications and financial transactions. Unlike a standard home computer that draws electricity from a wall outlet, this shared global machine requires a specific form of internal fuel to operate. This digital fuel is known as "gas." Every action performed on the network, from sending a simple payment to executing a complex smart contract, requires a payment in gas.

This mechanism serves two primary purposes. First, it compensates the network participants who provide the computational hardware and electricity needed to process transactions and secure the ledger. Without this financial incentive, there would be no reason for independent operators to maintain the infrastructure. Second, the gas requirement acts as a security barrier against spam and infinite loops. By attaching a cost to every computational step, the network prevents malicious actors from clogging the system with useless processes.

Understanding how this market operates is essential for anyone interacting with the blockchain. The costs associated with gas are not fixed. They fluctuate based on supply and demand dynamics that can change second by second. During periods of high network usage, the demand for block space increases, driving up the price of gas. Conversely, when the network is quiet, costs decrease significantly. This dynamic creates a living, breathing marketplace for computational resources.

The Concept of Gas and Gwei

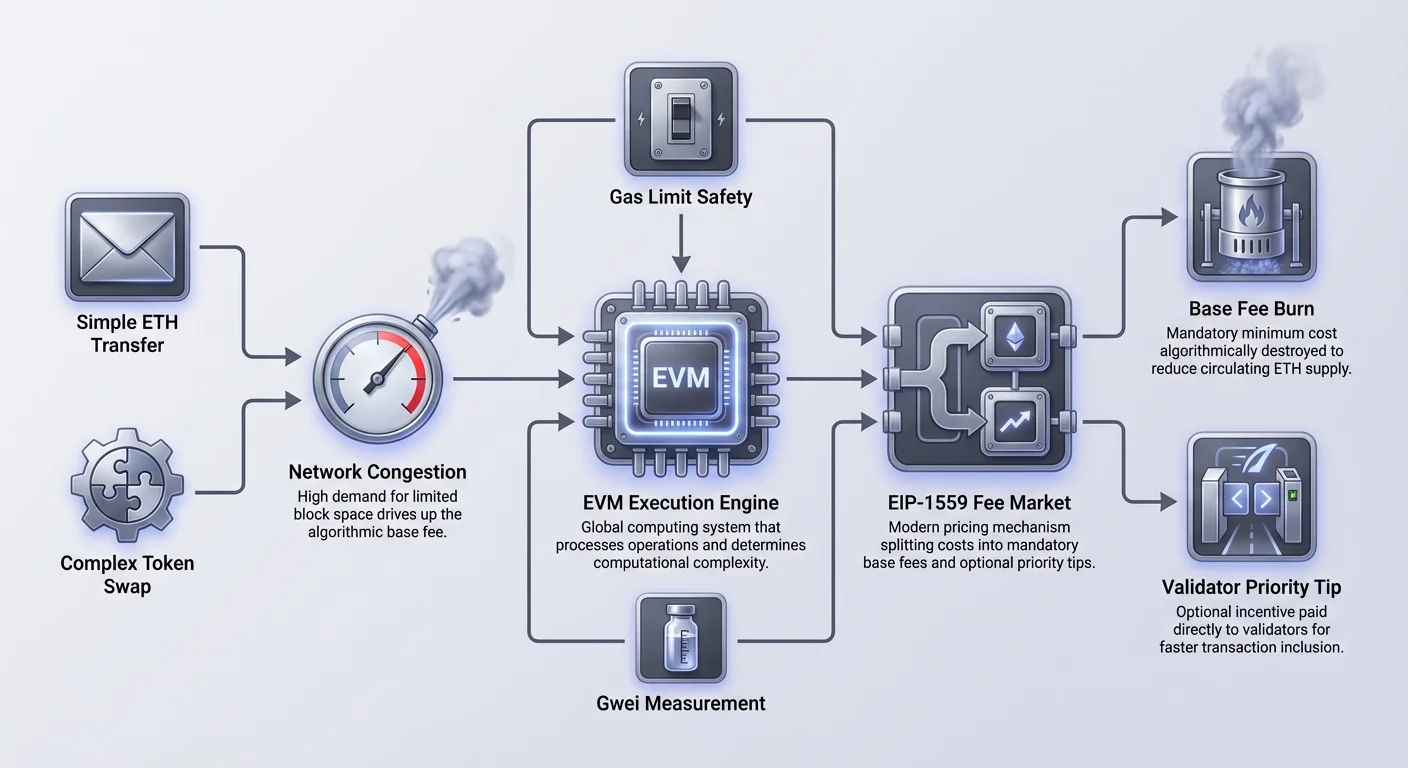

It is important to distinguish between "gas" as a unit of measurement and "Ether" (ETH) as the currency used to pay for it. Gas itself is a unit that measures the amount of computational effort required to execute a specific operation. A simple transfer of funds from one wallet to another requires a standard amount of computational work, typically set at 21,000 gas units. More complex interactions, such as swapping tokens on a decentralized exchange or minting a digital collectible, involve more lines of code and data storage. Consequently, these complex actions consume significantly more gas units.

While the amount of gas needed for a specific transaction type remains relatively stable, the price per unit of gas changes constantly. This price is denominated in a fractional unit of Ether called "gwei." One gwei equals 0.000000001 ETH. Users quote gas prices in gwei because the amounts are otherwise too small and cumbersome to handle in standard ETH terms. Instead of saying a gas price is 0.000000030 ETH, a user simply says "30 gwei."

The total transaction fee a user pays is calculated by multiplying the gas limit (the amount of work) by the gas price (the cost per unit of work). If a transaction requires 21,000 units of gas and the current market price is 30 gwei, the total fee would be 630,000 gwei, or 0.00063 ETH. This separation of "work required" and "price of work" allows the system to decouple the complexity of a task from the market value of network capacity.

The Modern Fee Structure

The mechanism for determining transaction fees underwent a significant overhaul with the implementation of Ethereum Improvement Proposal 1559 (EIP-1559) in August 2021. Prior to this update, the fee market operated on a "first-price auction" model. Users simply bid a gas price, and miners prioritized the highest bids. This system was often inefficient and unpredictable, leading users to frequently overpay just to ensure their transactions went through.

The modern system introduced a more structured approach to pricing. It split the single fee into two distinct components: the Base Fee and the Priority Fee. This dual-structure model was designed to make fees more predictable and to automate the process of bidding for block space. It removes much of the guesswork that previously plagued users, allowing wallets to estimate costs with greater accuracy.

The Base Fee Mechanism

The Base Fee is the mandatory minimum cost required to include a transaction in a block. It is not set by validators or miners but is algorithmically determined by the protocol itself based on the utilization of the previous block. The network targets a specific block size, measured in gas units (typically 15 million gas). If a block is more than 50% full, the Base Fee for the next block automatically increases. If it is less than 50% full, the fee decreases.

This algorithmic adjustment creates a predictable pricing curve. The fee can move up or down by a maximum of 12.5% from block to block. This prevents sudden, massive spikes in the minimum cost, although prolonged periods of high demand will still cause the price to rise exponentially over time. Crucially, the Base Fee is not paid to the validators. Instead, this portion of the ETH is "burned," meaning it is permanently destroyed and removed from the total circulating supply.

Priority Fees and Tips

The second component of the transaction cost is the Priority Fee, commonly referred to as a "tip." This is an optional fee that users add on top of the Base Fee. While the Base Fee is burned, the Priority Fee goes directly to the validator who proposes the block. This serves as an incentive for validators to include specific transactions, especially when the network is congested.

When the network is operating below capacity, the Priority Fee can be very low, as there is plenty of space in the block for everyone. However, when demand exceeds the available block space, users must compete to get their transactions processed quickly. In these scenarios, a higher Priority Fee acts as a bribe to the validator to jump the queue. Wallets often provide presets for these fees, allowing users to choose between "Eco," "Fast," or "Fastest" execution speeds based on their urgency and budget.

Transaction Execution and The EVM

At the heart of this system lies the Ethereum Virtual Machine (EVM). The EVM is the global computing engine that executes the code contained in smart contracts. Every node in the network runs the EVM and processes the same transactions to maintain consensus. When a user initiates a transaction, they are essentially sending a set of instructions to the EVM execution layer.

The EVM breaks down these instructions into smaller operations, known as opcodes. Each opcode has a specific gas cost associated with it based on its computational complexity. Simple mathematical additions are cheap, while operations that require storing data on the blockchain or accessing historical data are expensive. This granular pricing ensures that the fees paid accurately reflect the burden placed on the network's resources.

The gas limit acts as a safety mechanism during execution. When submitting a transaction, the user specifies the maximum amount of gas they are willing to consume. If the transaction hits this limit before completing, the EVM halts the operation and reverts any changes made to the ledger. However, the gas used up to that point is still paid to the validator as compensation for the wasted work. This prevents accidental infinite loops in code from draining a user's entire wallet or stalling the network indefinitely.

Market Dynamics and Congestion

The fee market is ultimately driven by supply and demand. The supply of block space is limited by the protocol rules. There is a target size of 15 million gas per block and a hard maximum of 30 million gas. Since new blocks are produced approximately every 12 to 15 seconds, the network has a finite throughput capacity. It cannot simply process more transactions just because more people want to use it.

Demand, on the other hand, is highly variable. It is driven by market events, such as a sudden crash in asset prices causing panic selling, or the launch of a popular new NFT collection. When demand surges, the algorithmic Base Fee begins to climb. If blocks remain full for an extended period, the Base Fee can skyrocket, making simple transactions prohibitively expensive for the average user.

During these congestion events, the user experience shifts. Wallets will display significantly higher cost estimates. Users who set their gas limits too low may find their transactions stuck in the "mempool"—a waiting area for pending transactions. These transactions will remain pending until network activity cools down and the market rate falls back to the price the user offered, or until the user submits a replacement transaction with a higher fee.

Token Standards and Gas Costs

The type of asset being moved significantly impacts the gas cost. While native Ether (ETH) transfers are the cheapest operation, moving tokens requires interacting with smart contracts. The most common standard for these assets is ERC-20. This standard defines a common list of rules that tokens must follow, allowing them to work seamlessly across different applications.

Comparing Transfer Costs

An ETH transfer is a native protocol action, requiring no smart contract interaction. In contrast, sending an ERC-20 token involves calling a function within a smart contract to update the ledger of balances. This updates the internal state of the contract, recording that User A now has fewer tokens and User B has more. This state change requires more computational resources than a native transfer.

Because of this added complexity, token transfers can cost two to three times more in gas than sending ETH. If a user interacts with a more complex protocol, such as a Decentralized Exchange (DEX) to swap tokens, the cost rises even further. A swap involves multiple contract interactions, liquidity pool checks, and balance updates, often costing ten times as much as a simple ETH transfer.

| Transaction Type | Complexity | Relative Cost |

|---|---|---|

| ETH Transfer | Low | 1x (Baseline) |

| ERC-20 Transfer | Medium | ~2x - 3x |

| Token Swap | High | ~5x - 10x |

The Role of Wrapped Ether (WETH)

A unique quirk of the ecosystem is the existence of Wrapped Ether (WETH). Ether itself predates the ERC-20 standard. Consequently, ETH does not follow the rules that govern ERC-20 tokens. This creates a compatibility issue for decentralized applications (dApps) designed to handle ERC-20 assets uniformly. To solve this, users often convert ETH into WETH.

A unique quirk of the ecosystem is the existence of Wrapped Ether (WETH). Ether itself predates the ERC-20 standard. Consequently, ETH does not follow the rules that govern ERC-20 tokens. This creates a compatibility issue for decentralized applications (dApps) designed to handle ERC-20 assets uniformly. To solve this, users often convert ETH into WETH. WETH is essentially a smart contract that holds ETH and issues an equivalent ERC-20 token pegged 1:1 with the deposit. This "wrapping" process allows ETH to behave exactly like any other token, simplifying the code for trading platforms and lending protocols. However, the process of wrapping and unwrapping ETH costs gas. Users must send a transaction to the WETH contract to deposit their ETH, incurring a fee. When they wish to retrieve their native ETH, they must send another transaction to burn the WETH and withdraw the funds.

Monetary Policy and Deflation

The introduction of the Base Fee burn mechanism fundamentally altered the network's monetary policy. In the original model, all fees went to miners, increasing the supply of circulating ETH as they sold their rewards. Under the current system, the Base Fee is permanently removed from circulation. This creates a direct link between network usage and the total supply of the currency.

When network activity is high, the amount of ETH being burned can exceed the amount of new ETH being issued to validators as block rewards. During these periods, the network becomes deflationary, meaning the total supply of ETH decreases over time. This acts as a counterbalance to the issuance of new coins.

The issuance rate dropped significantly following the transition to Proof-of-Stake, reducing the amount of new ETH entering the market by approximately 90%. Combined with the burn mechanism from EIP-1559, high transaction volumes accelerate the reduction of supply. This dynamic means that users paying for gas are not just buying block space; they are actively participating in the economic regulation of the asset's supply.

Advanced Gas Strategies

For frequent users, managing gas costs is a critical skill. Most modern wallets incorporate advanced features to help navigate the fee market. Automatic estimators analyze the last few blocks to suggest appropriate fees, but users can also manually adjust these settings. Setting a low priority fee can save money if the user is willing to wait longer for confirmation.

Conversely, if a transaction is time-sensitive, such as trying to buy a limited-availability item, users can increase the Priority Fee to outbid others. However, this "gas war" behavior can lead to wasted funds if the transaction fails or if someone else bids even higher. Advanced users may also utilize tools that track historical gas prices to identify the times of day or week when the network is typically less congested, scheduling their non-urgent maintenance tasks for these cheaper windows.

Layer 2 scaling solutions have emerged as a primary method for avoiding high mainnet fees. These networks process transactions off the main chain, batching them together before settling the final result on Ethereum. By splitting the gas cost of the final settlement across thousands of individual transactions, Layer 2s can offer fees that are a fraction of the cost of the main network.

Conclusion

The Ethereum gas market is a sophisticated economic engine that balances the scarcity of computational resources with the demand for decentralized execution. By shifting from a simple auction model to a dual-fee structure involving Base Fees and Priority Fees, the network has established a more predictable and efficient way to price block space. This system ensures that validators are compensated for their work while simultaneously managing network spam and integrating usage directly into the asset's monetary policy.

The relationship between gas, the EVM, and token standards like ERC-20 highlights the technical complexity involved in even the simplest blockchain interactions. As the ecosystem evolves with Layer 2 solutions and potential future upgrades, the mechanics of gas will likely continue to refine. However, the fundamental principle remains: computational power is a finite resource, and gas serves as the critical pricing mechanism that allocates this resource among millions of global users.

Gas fees are simply the price you pay for the computer to process your request securely.