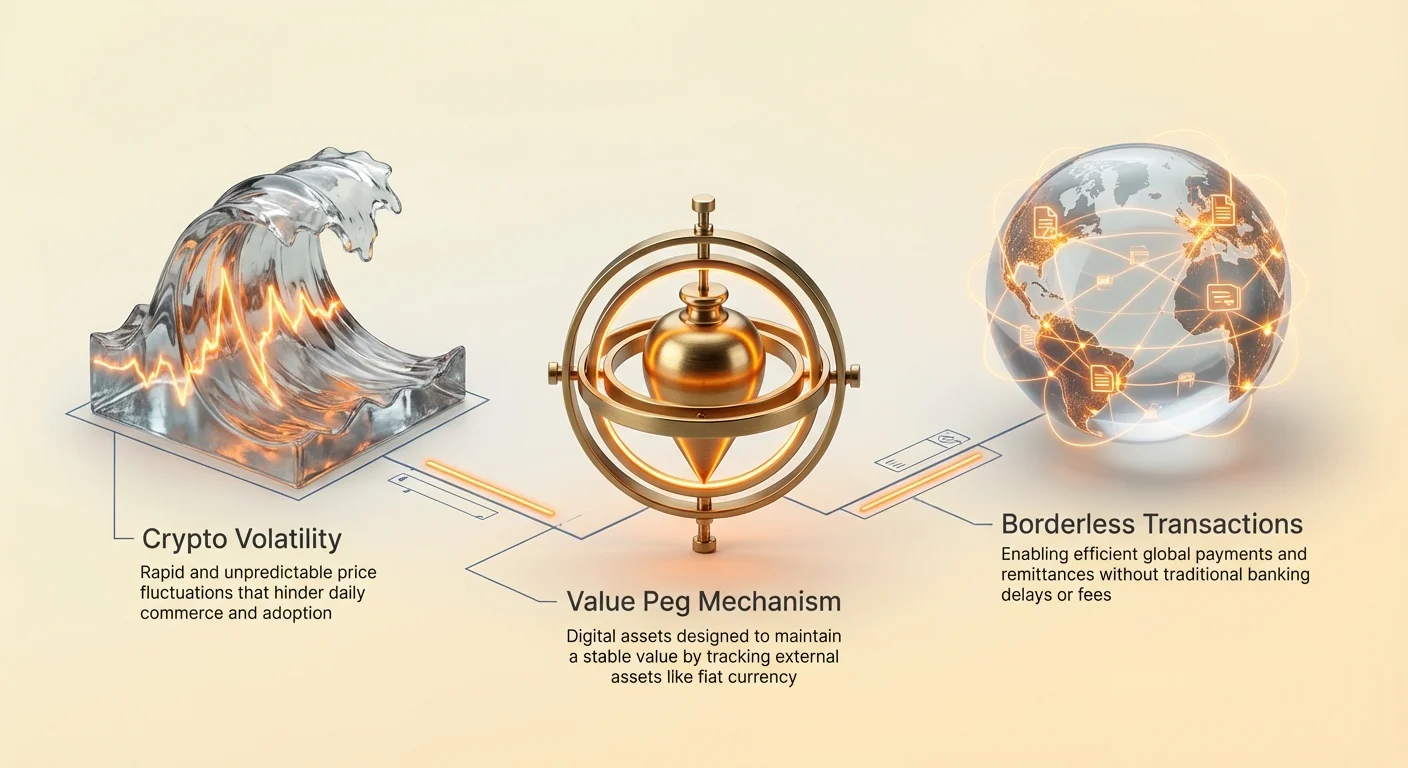

Cryptocurrency markets are characterized by their dynamic price movements. While this volatility attracts traders seeking significant returns, it presents a fundamental barrier to the adoption of digital assets for daily commerce. For a currency to function effectively as a medium of exchange or a unit of account, it requires a predictable value. If the purchasing power of a digital asset fluctuates wildly within a single hour, it becomes impractical for buying groceries, paying rent, or settling international business contracts.

This specific limitation within the crypto ecosystem led to the development of stablecoins. These are digital assets designed to minimize price volatility by pegging their value to a stable external asset, most commonly the US dollar. By combining the speed and borderless nature of blockchain technology with the relative stability of fiat currency, stablecoins serve as a critical bridge between traditional finance and the decentralized web. They allow users to store value and transact globally without leaving the blockchain environment.

The demand for these assets has grown exponentially. Initially used primarily by traders to lock in profits during market downturns, their utility has expanded significantly. Today, businesses use them for efficient cross-border settlements, and individuals in high-inflation economies use them to preserve their wealth. Understanding the mechanics, types and risks of these assets is essential for navigating the modern digital economy.

The Evolution of Monetary Systems

From Commodities to Fiat

The history of money reveals a constant search for efficiency and stability. Early societies relied on barter systems, which were limited by the need for a double coincidence of wants. Both trading parties had to desire exactly what the other offered. This inefficiency led to the adoption of commodity money, such as seashells or gold. These items possessed intrinsic value and scarcity, making them effective mediums of exchange.

As economies expanded, carrying heavy metals became impractical. This spurred the creation of representative money, where paper certificates represented a claim on a physical commodity stored in a vault. Eventually, this evolved into the modern fiat system. Fiat currency is not backed by physical commodities but by government decree and public trust. While flexible, fiat systems are vulnerable to inflation, where the purchasing power of money decreases over time due to supply expansion.

The Digital Transformation

The introduction of Bitcoin marked a shift toward digital scarcity. Unlike fiat currency, which can be printed at will by central banks, many cryptocurrencies have fixed supply schedules. However, the market valuation of these decentralized assets is determined solely by supply and demand dynamics, leading to high volatility.

Stablecoins emerged to address this specific gap in the evolutionary timeline. They attempt to offer the best of both worlds: the stability of fiat currencies and the technological advantages of cryptocurrencies. They operate on decentralized networks, allowing for 24/7 transfers and programmability, while maintaining a value that users recognize and understand. This hybrid approach has made them one of the most widely used applications of blockchain technology.

The Utility of Stable Digital Assets

The primary use case for stablecoins initially revolved around cryptocurrency trading. When a trader believes the market is about to drop, converting volatile assets like Bitcoin into a stablecoin allows them to protect their capital without converting back to fiat currency. This process avoids the time delays and fees associated with traditional banking transfers. The funds remain on the blockchain, ready to be deployed immediately when market conditions change.

Beyond trading, stablecoins are revolutionizing global payments. Traditional international transfers often take days to settle and incur high fees from multiple intermediaries. Stablecoin transactions settle in minutes, regardless of geographic distance. This efficiency is particularly valuable for remittances, where workers send money to families in other countries. By bypassing traditional rails, more value reaches the intended recipients.

In regions experiencing hyperinflation, stablecoins offer a lifeline. When a national currency loses value rapidly, citizens often face strict capital controls that prevent them from buying foreign currency. Stablecoins provide a digital alternative, allowing individuals to hold US-dollar-denominated assets via a smartphone. This acts as a hedge against the devaluation of their local purchasing power, offering economic freedom in restrictive environments.

Centralized Stability Mechanisms

Reserve-Backed Models

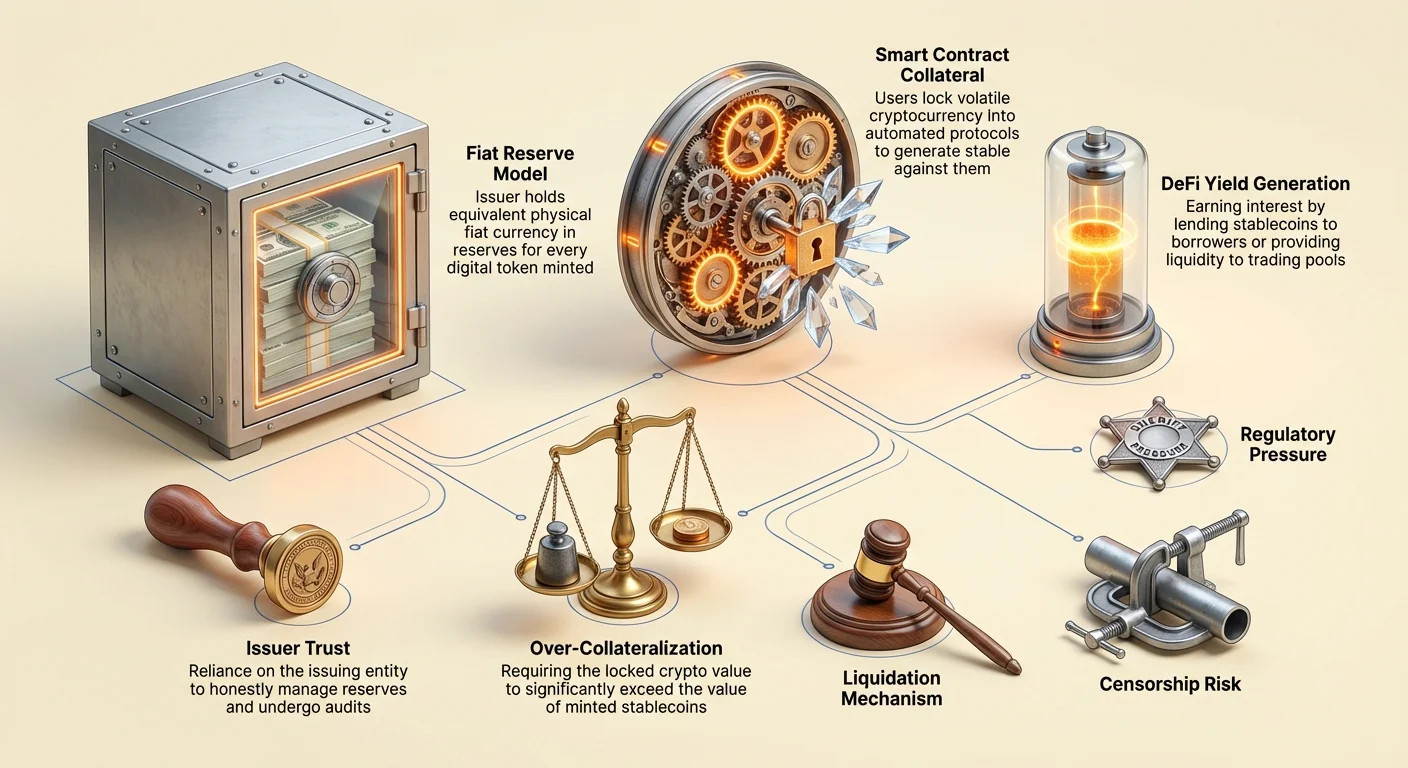

The most prevalent form of stablecoin is the centralized, reserve-backed model. In this system, a central issuer creates digital tokens that represent fiat currency held in a bank account. For every unit of the stablecoin issued on the blockchain, the company claims to hold an equivalent unit of fiat currency, such as the US dollar, in reserve. Tokens like USDT and USDC operate on this principle.

Users can, in theory, redeem their tokens for the underlying fiat currency at any time. This 1:1 backing provides a strong psychological assurance of value. The mechanism is straightforward: when a user deposits dollars with the issuer, new tokens are minted. When tokens are redeemed, they are burned, and the dollars are returned to the user. This expands and contracts the digital supply to match the reserves held in custody.

The Role of Trust

This model relies heavily on trust. Users must believe that the issuing company actually possesses the reserves they claim to have. Unlike decentralized assets where the ledger is public and verifiable by code, the reserves of a centralized stablecoin are held in private bank accounts. This introduces counterparty risk. If the issuer mismanages funds or faces regulatory action, the peg could be threatened.

To maintain confidence, reputable issuers undergo periodic audits or attestations by third-party accounting firms. These reports are published to verify that the assets in the bank match the tokens in circulation. However, the quality and frequency of these reports vary between issuers. The reliance on traditional banking infrastructure also means these assets are subject to the same regulations and limitations as the legacy financial system.

Transparency and Verification Issues

The intersection of corporate secrecy and public blockchain ledgers creates unique challenges for centralized stablecoins. While the movement of tokens is visible on-chain, the backing assets remain opaque. Controversy has historically surrounded certain issuers regarding the composition of their reserves. Questions often arise about whether reserves are held in liquid cash or in riskier commercial paper and corporate bonds.

If a significant portion of reserves is held in illiquid or volatile assets, a "run on the bank" scenario could be disastrous. If too many users attempt to redeem their tokens simultaneously, the issuer might struggle to convert their non-cash assets quickly enough to meet demand. This liquidity mismatch is a primary risk factor for holders of centralized stablecoins.

Furthermore, regulatory bodies globally are scrutinizing these reserves more closely. Demands for full transparency and strict capital requirements are increasing. In some jurisdictions, issuers are now required to hold reserves solely in high-quality liquid assets to ensure redemption is always possible. This regulatory pressure pushes the industry toward greater transparency but increases compliance costs for issuers.

Decentralized Protocols

Collateralized Debt Positions

Decentralized stablecoins aim to remove the need for a central authority. Instead of trusting a company, users trust smart contracts and code. The most successful version of this is the Collateralized Debt Position (CDP) model, used by protocols like MakerDAO to create DAI. In this system, users lock up volatile cryptocurrency assets, such as Ethereum, into a smart contract as collateral.

Once the collateral is locked, the user can generate a specific amount of stablecoins as a loan against their crypto holdings. Crucially, these loans must be over-collateralized. This means the value of the locked crypto must exceed the value of the stablecoins minted. For example, a user might need to lock $150 worth of Ethereum to mint $100 worth of DAI. This buffer protects the system against the volatility of the collateral asset.

Liquidation Mechanisms

The stability of a decentralized stablecoin depends on rigorous liquidation mechanisms. If the value of the collateral drops below a certain threshold, the smart contract automatically sells the collateral to repay the debt and burn the stablecoins. This ensures that the circulating supply remains fully backed, even if the market crashes.

This process is permissionless and automated. No human manager decides when to liquidate; the code executes the sale based on price feeds. While this removes central points of failure, it introduces complexity. Users managing CDPs must actively monitor their collateral ratios to avoid liquidation penalties. This model trades the counterparty risk of centralized issuers for the technical and market risks of managing complex financial positions.

The Algorithmic Experiment

A third, riskier category is the algorithmic or seigniorage-style stablecoin. These protocols attempt to maintain a peg without full collateral backing. Instead, they use complex algorithms and game theory incentives to manage supply and demand. The most infamous example was TerraUSD (UST), which utilized a two-token system involving a volatile sister token, LUNA.

The mechanism encouraged arbitrage. If UST traded above $1, users could burn $1 worth of LUNA to mint 1 UST, selling it for a profit and increasing the UST supply to lower the price. Conversely, if UST dropped below $1, users could burn UST to mint $1 worth of LUNA, reducing supply to raise the price. This relied entirely on the market's faith in the volatile sister token.

When confidence eroded, these systems historically faced a "death spiral." In May 2022, a massive sell-off broke the UST peg. The algorithm frantically minted trillions of LUNA tokens in a futile attempt to restore balance, rendering the collateral worthless. This event wiped out billions of dollars in value and highlighted the extreme dangers of under-collateralized financial engineering in the crypto space.

Generating Yield on Stable Assets

Decentralized Finance Opportunities

One of the most attractive features of stablecoins is the ability to earn yield. Unlike fiat currency sitting in a traditional savings account, which often earns negligible interest, stablecoins can be deployed in Decentralized Finance (DeFi) protocols. Yields in this sector have historically ranged significantly higher than traditional banking rates, reflecting the higher risk profile.

Holders can lend their stablecoins to borrowers through over-collateralized lending platforms. The interest paid by borrowers is distributed to the lenders. Alternatively, users can provide liquidity to Automated Market Makers (AMMs). By depositing stablecoins into a trading pool (e.g., a USDC/ETH pair), users earn a portion of the trading fees generated by the exchange.

Risk and Reward Dynamics

The high yields available in crypto markets are not without peril. Returns are generated through various strategies that carry specific risks. When depositing funds into a smart contract, users face "smart contract risk"—the possibility that a bug in the code could allow hackers to drain the funds. Unlike bank deposits, these funds are generally not insured by government agencies.

Additionally, yield generation often involves lending to traders who use leverage. During periods of high market volatility, demand for borrowing stablecoins increases, pushing interest rates up. However, if the market collapses, borrowers may default, or the platforms themselves may face insolvency. Users must carefully assess the source of the yield. If a protocol offers returns that seem too good to be true without a clear revenue source, it often indicates unsustainable economics or hidden risks.

Regulatory and Compliance Pressures

Governments view stablecoins with a mix of interest and caution. As these assets grow in market capitalization, they attract the attention of financial regulators who worry about their impact on monetary policy and financial stability. A major concern is the potential for stablecoins to facilitate illicit finance or evade capital controls.

Regulatory frameworks are tightening globally. Know Your Customer (KYC) and Anti-Money Laundering (AML) laws, which require verifying the identity of customers, are increasingly being applied to stablecoin issuers and the exchanges that trade them. This creates a tension between the open, permissionless ethos of crypto and the surveillance requirements of traditional finance.

In the United States and Europe, proposed legislation seeks to treat stablecoin issuers similarly to banks. This would impose strict reserve audits and operational standards. While this could increase consumer protection and reduce the risk of issuer collapse, it may also limit innovation and raise barriers to entry for new projects. The outcome of these regulatory battles will likely define the structure of the crypto market for the coming decade.

Censorship Resistance Spectrums

The Freedom to Transact

Censorship resistance refers to the ability of a network to process transactions without interference from third parties. It ensures that no entity can prevent a user from sending or receiving value, nor can they confiscate assets. This property exists on a spectrum. Bitcoin is widely considered the most censorship-resistant asset because its network is distributed globally among thousands of independent miners and nodes.

Centralized stablecoins like USDC and USDT sit on the opposite end of this spectrum. Because they are run by private companies subject to government regulation, they possess "blacklisting" capabilities. The issuers can, and do, freeze specific addresses at the request of law enforcement. When an address is frozen, the tokens inside become immovable and effectively worthless.

Implications for Users

This capability creates a fundamental divergence in utility. For institutional investors and compliant businesses, the ability to freeze funds is a safety feature that recovers stolen assets and ensures regulatory compliance. For users seeking true financial sovereignty or those living under authoritarian regimes, this feature represents a critical vulnerability.

Decentralized stablecoins like DAI offer a middle ground but are not immune. Since DAI is largely collateralized by centralized assets like USDC, it inherits some of the censorship risks of its collateral. If the issuer of the collateral were to freeze the assets held in the decentralized protocol's smart contracts, the stability of the decentralized token would be compromised. This interdependence highlights the difficulty of achieving complete censorship resistance while maintaining a stable peg to a fiat currency.

The Future Landscape

The stablecoin market is rapidly evolving. Central banks are actively developing their own competitors: Central Bank Digital Currencies (CBDCs). A CBDC would be a digital version of a national currency, issued directly by the central bank rather than a private company. These would likely offer the highest level of safety regarding the peg but arguably the lowest level of privacy and censorship resistance.

Private stablecoins will likely continue to integrate deeper into the DeFi ecosystem. We may see a bifurcation of the market: highly regulated, compliant stablecoins for institutional use and mainstream commerce, alongside experimental, decentralized alternatives for crypto-native applications. As technology matures, the focus will shift toward improving capital efficiency and reducing the reliance on centralized banking infrastructure.

| Feature | Centralized Stablecoins | Decentralized Stablecoins |

|---|---|---|

| Backing | Fiat reserves in bank | Crypto assets in smart contracts |

| Trust Model | Trust in issuing company | Trust in code/market mechanisms |

| Censorship | Funds can be frozen/censored | High resistance to freezing |

Conclusion

Stablecoins represent a critical innovation in the financial landscape, solving the volatility problem that hinders widespread cryptocurrency adoption. By offering a predictable store of value and a reliable medium of exchange, they unlock the potential of blockchain technology for payments, savings, and global commerce. However, this stability comes with distinct trade-offs regarding trust, centralization, and regulatory compliance.

The risks associated with stablecoins are multifaceted. Centralized models introduce counterparty risk and censorship possibilities, while decentralized models face technical complexities and market-based liquidation risks. Algorithmic attempts have shown the catastrophic consequences of flawed economic design. As the sector matures, users must navigate these risks carefully, understanding that not all stable assets are built with the same resilience or safety mechanisms.

Understanding the mechanics behind a stablecoin is the only way to truly assess if your digital dollars are safe.