The evolution of cryptocurrency trading has moved rapidly from centralized systems to decentralized protocols. In the early days of digital assets, buying or selling required a trusted intermediary to manage the order book and hold funds. This model mirrored traditional finance, where banks and brokers facilitated every exchange. However, the rise of Decentralized Finance (DeFi) introduced a new paradigm that allows users to trade directly with smart contracts.

At the heart of this shift is a fundamental change in how market liquidity is sourced and managed. Traditional platforms rely on market makers to provide buy and sell orders. Decentralized Exchanges (DEXs) often use a different mechanism entirely. They replace the traditional order book with code known as Automated Market Makers (AMMs). This technology allows trading to occur 24/7 without a central authority or a specific counterparty on the other side of the trade.

Understanding how AMMs function requires a deep dive into the concept of liquidity itself. It is the fuel that powers these decentralized engines. Without sufficient liquidity, trading becomes expensive, slow, and inefficient. For traders and investors alike, grasping the mechanics of AMMs is no longer optional. It is essential for navigating the modern crypto landscape safely and effectively.

The Foundation: Understanding Liquidity

Liquidity is a term often thrown around in financial circles, but it has specific implications in crypto. In the broadest sense, it refers to how easily an asset can be converted into cash or another asset without significantly affecting its price. Cash is the ultimate liquid asset because it is universally accepted. Real estate, by contrast, is highly illiquid because selling a property takes time, effort, and negotiation.

Financial Liquidity

Financial liquidity specifically measures the ease of converting assets into cash. In the context of cryptocurrency, major assets like Bitcoin and Ethereum are considered highly liquid. They can be sold for stablecoins or fiat currency almost instantly on most major platforms. There is a massive pool of buyers ready to purchase these assets at any given moment.

However, not all digital assets share this trait. Smaller altcoins or specific Non-Fungible Tokens (NFTs) often suffer from low financial liquidity. A holder might own an asset that is theoretically valuable, but if no one is willing to buy it immediately, its effective liquidity is zero. This risk is inherent in newer or niche markets where the pool of participants is small.

Market Liquidity

Market liquidity refers to the health of a specific trading pair on an exchange. It indicates the market's ability to absorb large buy or sell orders without causing drastic price changes. A liquid market is stable. If a trader buys a large amount of Bitcoin on a major exchange, the price barely moves because there are enough sell orders to cover the demand.

In contrast, an illiquid market is volatile and fragile. If a trader attempts a large transaction in a trading pair with low volume, the price may spike or crash instantly. This phenomenon occurs because there are not enough orders to fulfill the request at the current price. The trade "eats through" the available orders, pushing the price further up or down until the order is filled.

Why Liquidity Matters for Traders

For the average user, liquidity dictates the cost and speed of a trade. High liquidity generally results in tighter spreads, meaning the difference between the buying and selling price is small. This ensures that traders get a fair market rate for their assets.

Low liquidity leads to a problem known as slippage. Slippage happens when the final execution price of a trade is different from the expected price. In a highly illiquid environment, a trader might expect to buy a token for $100, but due to a lack of sellers, the average cost ends up being $105. This hidden cost erodes profits and adds significant risk to trading on smaller decentralized platforms.

The Traditional Model: Centralized Order Books

To appreciate the innovation of AMMs, one must first understand the system they replaced. Centralized Exchanges (CEXs) operate using an order book model. This is the standard in traditional stock markets and major crypto platforms. An order book is simply a digital list of all outstanding buy and sell orders for a specific asset pair.

In this system, there are two main participants: makers and takers. Makers are traders who place limit orders. They state a specific price at which they are willing to buy or sell, adding depth to the order book. Takers are traders who accept those existing orders at the current market price, removing liquidity from the book. The exchange’s matching engine pairs these buyers and sellers instantly.

This model works exceptionally well when there are thousands of active participants. However, it relies heavily on professional market makers—institutions that constantly place buy and sell orders to ensure there is always someone to trade with. If these market makers withdraw, liquidity dries up, and trading grinds to a halt. This reliance on centralized entities and professional liquidity provision was a bottleneck that decentralized finance sought to remove.

Enter the Automated Market Maker (AMM)

DeFi solved the liquidity problem by removing the need for a traditional order book. Instead of matching a buyer with a seller, Decentralized Exchanges use Automated Market Makers. An AMM is a protocol that allows digital assets to be traded in a permissionless and automatic way by using liquidity pools rather than a traditional market of buyers and sellers.

The Innovation of Constant Product

The most common AMM model uses a mathematical formula to determine prices. The classic formula, popularized by Uniswap, is x * y = k. In this equation, x and y represent the quantity of two different tokens in a liquidity pool. The variable k is a constant value that the pool attempts to maintain.

The protocol dictates that the total liquidity in the pool must remain constant. When a trader buys Token A from the pool, they add Token B. This increases the supply of Token B and decreases the supply of Token A. According to the formula, as the supply of Token A drops, its price relative to Token B must rise. This automatic price adjustment happens instantly with every trade, ensuring the pool remains balanced according to the algorithm.

Removing the Counterparty

In a traditional trade, if you want to sell Bitcoin, you need another human or bot to buy it. In an AMM, your counterparty is a smart contract. You are trading against a pool of funds, not a person. This means trades can be executed 24/7, regardless of whether any other traders are active at that moment.

This system democratizes market making. You no longer need permission from a centralized exchange or massive capital to facilitate trades. Anyone can interact with the smart contract to swap tokens. The pricing is not set by a central authority but is derived purely from the ratio of assets currently held in the smart contract.

The Role of Arbitrage

AMMs do not automatically know the external market price of an asset. They only know the ratio of tokens inside their own pool. If the price of Ethereum rises on a centralized exchange, the price on the AMM might lag behind briefly. This discrepancy creates an opportunity for arbitrage traders.

Arbitrageurs notice that Ethereum is cheaper on the AMM than on the outside market. They buy the undervalued Ethereum from the AMM, which reduces the pool's supply and drives the price up. They continue buying until the AMM price matches the global market price. These traders play a vital role in keeping AMM prices accurate, effectively synchronizing the decentralized pools with the broader financial world.

The Engine Room: Liquidity Pools

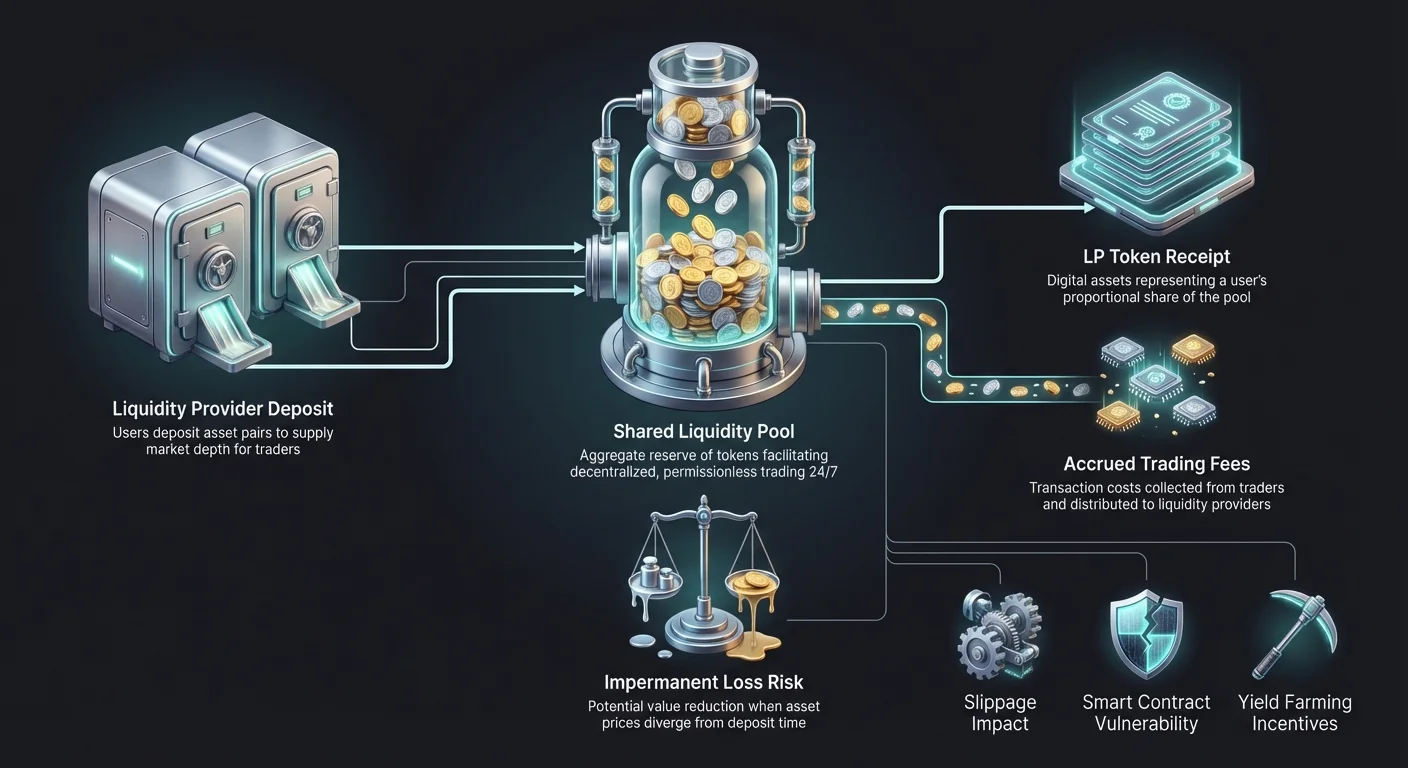

An AMM cannot function without assets. A smart contract with no tokens cannot facilitate a trade. This is where liquidity pools come in. A liquidity pool is a crowdsourced collection of crypto assets locked in a smart contract. These pools are the backbone of any DEX.

Instead of a centralized company providing the funds, the liquidity is provided by users. These users are known as Liquidity Providers (LPs). LPs deposit pairs of tokens—typically in equal value—into the pool. For example, a user might deposit $1,000 worth of Ethereum and $1,000 worth of USDC. By doing so, they increase the depth of the market, allowing other users to trade against those funds. The larger the pool, the more stable the prices and the lower the slippage for traders.

The Incentive: Why Provide Liquidity?

Why would a user lock up their valuable assets in a smart contract for strangers to trade against? The answer lies in financial incentives. DEXs are designed to reward those who facilitate the system. Without these incentives, the pools would be empty, and the exchange would fail.

Earning Trading Fees

Every time a trader executes a swap on a DEX, they pay a small transaction fee. On a centralized exchange, this fee goes to the corporate entity running the platform. On a DEX, this fee is distributed directly to the Liquidity Providers.

The fees are shared explicitly based on the percentage of the pool a user owns. If you provide 1% of the total liquidity in a specific pool, you are entitled to 1% of the trading fees generated by that pool. For popular trading pairs with high volume, these fees can generate a significant annualized return, often higher than traditional bank interest rates.

LP Tokens

When a user deposits assets into a pool, the smart contract issues them a receipt known as a Liquidity Provider (LP) token. These tokens represent the user's share of the pool. They are crucial for tracking ownership and claiming rewards.

LP tokens are themselves crypto assets. They can be transferred, traded, or used in other DeFi applications. When a liquidity provider wants to exit the market, they return their LP tokens to the smart contract. In exchange, the contract burns the LP tokens and releases the user's original deposited assets, plus any trading fees earned during the period.

Yield Farming

To attract even more liquidity, many protocols offer additional rewards on top of standard trading fees. This practice is known as yield farming or liquidity mining. A DEX might distribute its own governance token to users who stake their LP tokens.

This creates a dual layer of income for the provider: the trading fees from the swaps and the free governance tokens from the protocol. Yield farming has been a major driver of DeFi growth, as it allows users to put their idle assets to work. However, it introduces complexity, as users must manage multiple tokens and smart contract interactions to maximize their returns.

Risks and Challenges in AMM Trading

While AMMs offer autonomy and profit potential, they are not without risks. The decentralized nature of these platforms means there are no safety nets. If a user makes a mistake or the technology fails, funds can be lost permanently. Understanding these risks is critical for anyone participating in DeFi.

Impermanent Loss

The most significant risk for liquidity providers is a concept called Impermanent Loss (IL). This occurs when the price of the deposited tokens changes compared to when they were deposited. Because the AMM automatically rebalances the ratio of assets, an LP often ends up holding more of the token that is dropping in value and less of the token that is rising.

For example, if you deposit ETH and USDC, and the price of ETH doubles, the pool will sell some of your ETH for USDC to maintain the ratio. If you withdraw your funds at that moment, your total value in dollar terms will be higher than when you started, but lower than if you had simply held the ETH and USDC in a wallet without providing liquidity. The loss is "impermanent" because it disappears if prices return to their original ratio, but it becomes permanent once funds are withdrawn.

Slippage and Price Impact

For traders, the primary risk is slippage. As mentioned earlier, this is the difference between the expected price and the executed price. In AMMs, slippage is determined by the size of the trade relative to the size of the pool.

If a pool has $1 million in liquidity and a trader tries to swap $500,000, the price impact will be massive. The algorithm will exponentially increase the price as the supply of the requested token drains. Traders must be careful to check the price impact before confirming a transaction. Most DEX interfaces allow users to set a "slippage tolerance" (e.g., 0.5% or 1%), causing the transaction to fail if the price moves beyond that limit.

Smart Contract Risks

AMMs run on smart contracts—code executed on the blockchain. While this removes human error in execution, it introduces technical risk. If the code contains a bug or a vulnerability, hackers can exploit it to drain the liquidity pools.

Unlike a centralized exchange where a company might have insurance or legal recourse, DeFi hacks are often irreversible. Furthermore, because anyone can create a token and a liquidity pool, scams are prevalent. "Rug pulls" occur when a developer creates a new token, pairs it with a valuable asset like Ethereum in a liquidity pool, and then pulls all the liquidity out, leaving investors with worthless tokens.

Comparing Architectures: CEX vs. DEX

The choice between using a Centralized Exchange (CEX) and a Decentralized Exchange (DEX) depends on user priorities. CEXs offer speed and ease of use, while DEXs offer control and privacy. The following comparison highlights the structural differences between the two models.

| Feature | Centralized Exchange (CEX) | Decentralized Exchange (DEX) |

|---|---|---|

| Custody | Exchange holds funds | User holds funds (Self-custody) |

| Trading Mechanism | Order Book (Makers/Takers) | Automated Market Maker (AMM) |

| Privacy | Requires KYC (ID Verification) | No KYC (Anonymous/Pseudonymous) |

| Asset Listing | Vetted by exchange management | Permissionless (Anyone can list) |

| Fees | Exchange keeps fees | Liquidity Providers earn fees |

| Security Risk | Corporate hack or insolvency | Smart contract bugs or user error |

This table illustrates the trade-offs. A CEX acts as a custodian, which is convenient but risky if the exchange goes bankrupt. A DEX requires the user to manage their own security via a private wallet, which grants total ownership but requires more technical responsibility.

Key Terminology for DEX Traders

Navigating the world of AMMs requires learning a new vocabulary. These terms appear frequently in DEX interfaces and documentation. Mastery of this lingo helps traders avoid costly mistakes and understand the mechanics of their transactions.

Gas

Gas refers to the fee paid to the network to execute a transaction. Every interaction with a smart contract—whether swapping tokens, adding liquidity, or claiming rewards—requires computation. Users pay for this computation in the blockchain's native currency (e.g., ETH on Ethereum). During times of high network congestion, gas fees can spike, making small trades uneconomical.

TVL (Total Value Locked)

Total Value Locked is a metric used to gauge the health and size of a DeFi protocol. It represents the aggregate dollar value of all assets currently deposited in the platform’s smart contracts. A high TVL generally indicates that the protocol is trusted by the community and has deep liquidity, which usually translates to better trading rates and lower slippage.

Aggregators

As the number of DEXs has grown, price differences between them have become common. DEX aggregators are tools that scan multiple exchanges to find the best price for a specific trade. They can split a single trade across several liquidity pools to minimize slippage. Aggregators act as a search engine for liquidity, simplifying the process for the end user.

The Future of Decentralized Trading

The technology behind AMMs is evolving rapidly. Early iterations were simple and sometimes inefficient, but new generations of protocols are solving these issues. Innovations are focusing on capital efficiency, allowing liquidity providers to concentrate their funds within specific price ranges. This mimics the depth of traditional order books while retaining the decentralized nature of the AMM.

Furthermore, the rise of Layer-2 solutions is addressing the issue of high gas fees. By processing transactions off the main chain and settling them in batches, these networks make DEX trading affordable for smaller investors. User interfaces are also improving, narrowing the gap between the slick experience of a CEX and the complex functionality of a DEX. As these barriers lower, the distinction between traditional and decentralized trading continues to blur.

Conclusion

The shift from centralized order books to Automated Market Makers represents a major turning point in financial history. By replacing intermediaries with code, AMMs have democratized access to market making and trading. Liquidity is no longer the domain of large institutions; it is a crowdsourced resource that anyone can contribute to and benefit from. This architecture ensures that markets can function 24/7 without reliance on a central authority.

However, this freedom comes with increased responsibility. Traders must navigate risks like impermanent loss, slippage, and smart contract vulnerabilities. Understanding the mechanics of liquidity pools and the incentives that drive them is essential for survival in this space. As the technology matures, it promises to build a more open, transparent, and efficient financial system for the global economy.

True financial sovereignty requires understanding the code that manages your money.