For centuries, the concept of money has relied entirely on a system of trusted intermediaries. Whether trading gold certificates, exchanging paper currency, or swiping a credit card, financial transactions have always required a third party to verify who owns what. Banks, governments, and payment processors maintain the ledgers that track the movement of wealth. This system works reasonably well when the centralized authorities are competent and honest, but it introduces a single point of failure. If the central authority makes an error, engages in corruption, or decides to freeze assets, the user has little recourse.

The financial crisis of 2008 exposed the fragility of this trust-based model. Major financial institutions that were considered pillars of the global economy collapsed or required bailouts due to mismanagement. Trust in the banking system eroded rapidly as individuals realized their money was not as secure as they had believed. It became clear that the centralized ledgers managed by traditional finance were opaque and vulnerable to manipulation. The world needed a form of money that did not rely on human error or institutional permission to function.

In the midst of this turmoil, a pseudonym known as Satoshi Nakamoto released a whitepaper proposing a solution. This solution was a peer-to-peer electronic cash system that removed the need for trusted third parties entirely. By utilizing cryptographic proof rather than trust, this new system allowed two willing parties to transact directly with one another without the need for a middleman. This invention introduced the world to the concept of digital scarcity, solving a problem that had plagued computer scientists for decades.

The Failure of Centralized Money

To understand why digital scarcity was necessary, one must first understand the inherent flaws of fiat currency. Fiat money is government-issued currency that is not backed by a physical commodity like gold or silver. Its value is derived primarily from government decree and public trust in the issuing authority’s economic stability. While this system allows for flexible monetary policy, it also grants central banks the power to increase the money supply at will.

When a government prints more money, the supply increases, but the value of goods and services does not necessarily grow at the same rate. This imbalance typically leads to inflation, where the purchasing power of each individual unit of currency decreases. Over time, holding fiat currency results in a guaranteed loss of value. The ledger that tracks this money is private and closed, meaning the public cannot audit the money supply or verify that the rules are being followed.

This centralization also creates a permissioned system. To participate in the modern economy, one must apply for an account with a bank. These institutions act as gatekeepers, deciding who is allowed to transact and who is not. They can block transactions, freeze accounts, and charge fees for their services. For millions of people around the world who live under authoritarian regimes or in areas with underdeveloped banking infrastructure, this system acts as a barrier to financial freedom rather than a facilitator of it.

The Digital Double-Spend Problem

Before 2009, creating digital money was considered impossible due to the "double-spend" problem. In the digital world, a file is easily copied. If you send a photo to a friend via email, you retain a copy of that photo on your own device. Both you and your friend now have the file. This mechanism works perfectly for sharing information, but it is disastrous for money. If you could send a digital dollar to a merchant and also keep that same digital dollar to spend again, the currency would be worthless.

Prior attempts to create digital cash relied on a central server to track balances and prevent double-spending. However, this returned to the original problem of centralized trust. If the central server was hacked or shut down, the currency would fail. Satoshi Nakamoto’s innovation was to solve the double-spend problem without a central server.

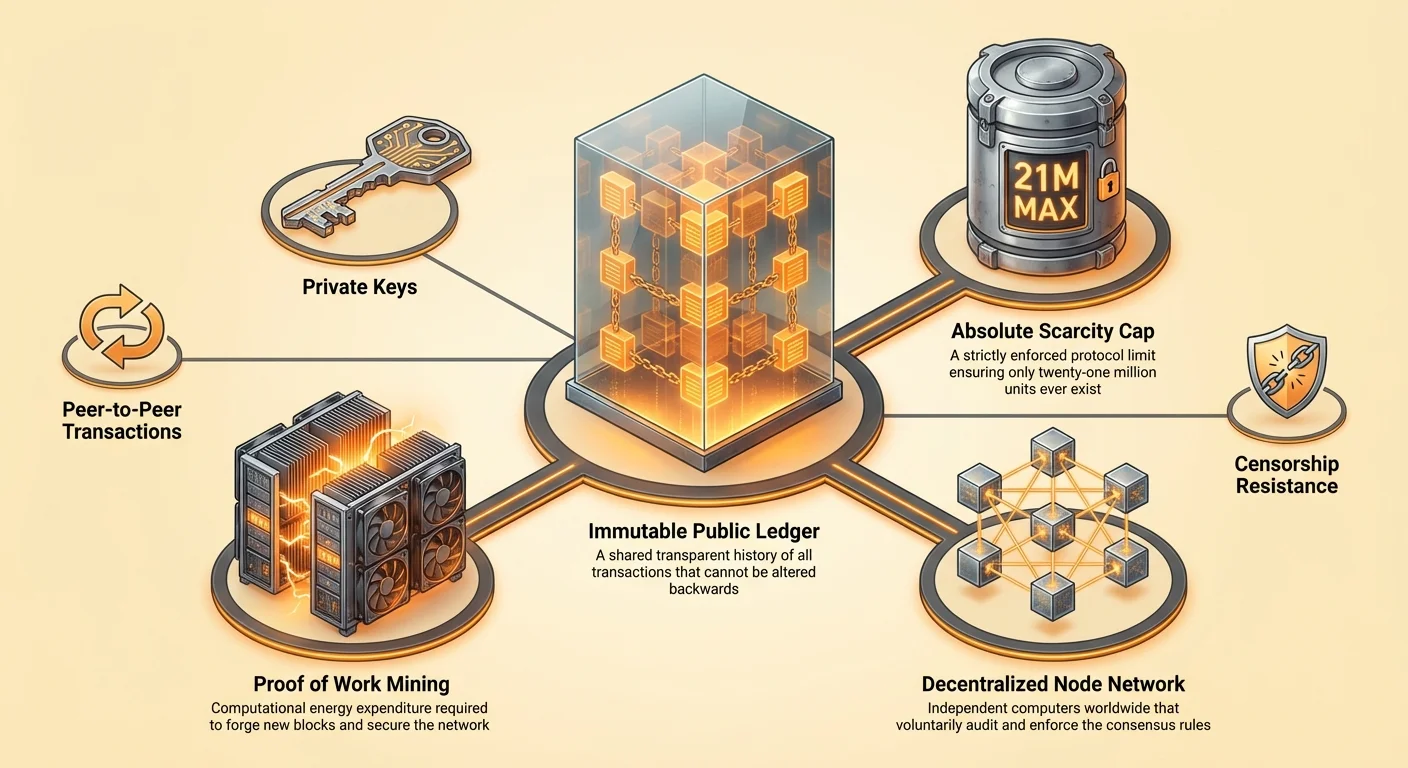

The solution involved a public, decentralized ledger known as a blockchain. Instead of one bank holding the ledger, thousands of independent computers, known as nodes, would hold identical copies of the ledger. Every transaction would be broadcast to the entire network. If someone tried to spend the same coin twice, the network would reject the second transaction because it would conflict with the history recorded on the shared ledger. This breakthrough allowed for the creation of a digital asset that was unique, uncopyable, and finite.

The Engineering of Absolute Scarcity

The defining characteristic of this new digital asset is its absolute scarcity. Unlike fiat currencies, which can be printed without limit, the protocol for this digital asset has a hard cap. There will never be more than 21 million units created. This supply schedule is written into the code and enforced by the network of participants. No central bank or government can decide to mint more coins to pay off debts or stimulate the economy.

This fixed supply creates a deflationary pressure that contrasts sharply with inflationary fiat money. As demand for the asset grows over time, the supply remains strictly limited, which historically has led to an increase in purchasing power. This scarcity is verifiable by anyone. By running a node, a user can independently audit the entire supply to ensure that no extra coins have been secretly created.

While the total supply is capped, the utility of the currency is maintained through divisibility. Each unit can be divided into 100 million smaller units. This ensures that the world will never "run out" of the currency. Even if the value of a single unit becomes incredibly high, users can still transact in small fractions. This combination of strict scarcity and high divisibility mimics the properties of precious metals but adapts them for the digital age.

The Mechanics of Trustless Consensus

The system relies on a mechanism called Proof of Work to secure the network and reach an agreement on the state of the ledger. In a decentralized network where participants do not know or trust each other, there must be a way to prevent bad actors from flooding the network with false information. Proof of Work solves this by requiring participants to expend energy to propose new blocks of transactions.

The Role of Mining

The individuals and entities that perform this work are called miners. They use powerful computers to solve complex mathematical problems. The process is energy-intensive by design. This energy expenditure serves as a barrier to entry for attackers. To rewrite the history of the ledger or alter transactions, an attacker would need to control more than half of the network's computing power. This would require a staggering amount of hardware and electricity, making such an attack economically irrational.

Mining also serves as the distribution mechanism for new coins. When a miner successfully solves the mathematical problem and adds a block of transactions to the chain, they are rewarded with newly minted coins. This process is often compared to gold mining, where physical effort is required to extract new resources from the earth. In the digital realm, computational effort is required to unlock new units of currency.

The Power of Nodes

While miners build the blockchain, nodes are the auditors that enforce the rules. A node is a computer running the software that validates every transaction and block. Nodes ensure that miners are not cheating. If a miner tries to create more coins than the protocol allows or tries to process an invalid transaction, the nodes will reject the block.

Anyone can run a node without asking for permission. This is a critical component of decentralization. It means that the rules of the network are not enforced by a police force or a court system, but by the collective consensus of thousands of independent users. This structure ensures that the network remains open, neutral, and resistant to corruption.

Unstoppable Financial Sovereignty

One of the most profound implications of a decentralized, scarce digital asset is censorship resistance. In the traditional financial system, transactions can be blocked, reversed, or flagged by intermediaries. Governments can pressure banks to cut off services to political dissidents, protest movements, or industries they deem undesirable. This ability to weaponize the financial system is a powerful tool for control.

A decentralized digital currency operates as a "push" system. The user pushes the value directly to the recipient, similar to handing someone physical cash. There is no intermediary to step in and stop the transfer. Once a transaction is confirmed on the blockchain, it is immutable. It cannot be reversed, altered, or erased. This property gives individuals total control over their wealth.

This level of sovereignty is essential in a world where financial repression is common. Capital controls, which prevent citizens from moving their wealth out of a country, are used by struggling economies to trap value. A censorship-resistant asset allows individuals to bypass these controls and preserve their purchasing power. It serves as an exit valve for people living under monetary regimes that are failing or oppressive.

Comparing Stores of Value

Throughout history, humans have used various items as stores of value, from seashells to precious metals. To understand where digital scarcity fits in, it is helpful to compare it to traditional assets like gold, fiat currency, and real estate. Each of these assets has different properties regarding liquidity, scarcity, and portability.

| Feature | Digital Scarcity (Bitcoin) | Gold | Fiat Currency | Real Estate |

|---|---|---|---|---|

| Scarcity | Absolute (Mathematical) | Relative (Physical) | Unlimited (Political) | High (Physical) |

| Portability | High (Global/Digital) | Low (Heavy/Physical) | High (Digital) | Impossible |

| Liquidity | High (24/7 Markets) | Medium | High | Low |

The Digital Gold Narrative

Gold has long been the gold standard for storing value because it is durable, fungible, and difficult to increase in supply. However, gold is heavy and expensive to secure. Transporting large amounts of value in gold requires armored trucks and security teams. It is also difficult to verify; fake gold bars filled with tungsten have fooled even experienced dealers.

Digital scarcity offers an improvement on gold’s properties. It is weightless and can be transported across the world in minutes. A billion dollars in value can be stored on a device smaller than a thumb drive or even memorized as a seed phrase. Verification is instant and cost-free using a software node. While gold has a multi-millennial track record, digital assets are rapidly establishing themselves as a superior alternative for the modern era.

The Problem with Real Estate

Real estate is another common store of value, prized for its scarcity. They are not making any more land. However, real estate is highly illiquid. Buying or selling a property takes months and involves significant friction in the form of fees, taxes, and legal paperwork. Real estate is also immovable. If you need to flee a jurisdiction due to war or political instability, you cannot take your house with you. Digital assets solve the liquidity and portability issues inherent in property while maintaining the scarcity that gives it value.

The Privacy Paradox

A common misconception about public blockchains is that they are anonymous. In reality, they are pseudonymous. The ledger is completely transparent, meaning every transaction that has ever occurred is visible to the public. However, these transactions are not tied to names or physical addresses, but to strings of cryptographic characters known as addresses.

Tracing and Transparency

Because the ledger is public, it is possible to trace the flow of funds. Blockchain analytics firms specialize in analyzing these patterns to link addresses to real-world identities. If a user undergoes a "Know Your Customer" (KYC) process at a centralized exchange, their identity can be linked to their on-chain activity. Once that link is made, their financial privacy is compromised.

This transparency is a double-edged sword. It makes the system auditable and prevents corruption within the supply mechanics, but it requires users to be proactive about their privacy. Best practices for maintaining privacy include avoiding address reuse and utilizing tools that break the link between sender and receiver.

The Spectrum of Anonymity

True privacy in a digital age is difficult to achieve. While cash remains the most private form of transaction, it is physical and local. Digital scarcity provides a middle ground—more private than a credit card statement sold to advertisers, but less private than a suitcase of banknotes. Enhancements to the protocol and second-layer technologies continue to improve the privacy guarantees for users who prioritize anonymity.

Energy as a Shield

The environmental impact of the Proof of Work mechanism is a subject of intense debate. Critics argue that the energy consumption of the network is wasteful. However, this perspective often fails to account for the utility of the security being purchased with that energy. The energy is not wasted; it is used to secure a global financial network that holds hundreds of billions of dollars in value without a standing army or a banking fortress.

Thermodynamic Security

The requirement to expend energy is what gives the network its unforgeable costliness. If creating money or changing the ledger were cheap, it would be easy to attack. By tethering the digital asset to the physical world of energy production, the network creates a thermodynamic wall of security. This prevents spam and makes rewriting the blockchain prohibitively expensive.

Furthermore, the search for cheap energy drives miners to seek out stranded assets. Hydroelectric dams that produce more power than the local grid can consume, or natural gas flares at remote oil sites, are increasingly used to power the network. In these cases, the network acts as a buyer of last resort for energy that would otherwise be wasted.

Comparative Efficiency

When comparing efficiency, one must look at the total cost of the existing fiat system. The traditional banking system requires physical branches, data centers, armored transport, and millions of employees commuting to work. It is also backed by the military power required to sustain the dominance of national currencies. Compared to the sprawling infrastructure of the legacy financial world, a digital network that secures value directly through electricity is arguably a more efficient allocation of resources.

Sovereignty and Self-Custody

The ultimate innovation of digital scarcity is the ability to self-custody wealth. In the traditional system, money in a bank account is technically not the user's property; it is a liability of the bank. The user is a creditor to the bank. If the bank fails, the user must rely on insurance schemes or government bailouts to be made whole.

With digital assets, possession of the private key equates to ownership of the asset. A self-custodial wallet allows the user to hold their wealth directly, without any counterparty risk. This is often summarized by the mantra: "Not your keys, not your coins."

The Responsibility of Freedom

This freedom comes with responsibility. If a user loses their private key, the funds are unrecoverable. There is no customer support line to call and no password reset function. This shift requires a change in mindset from reliance on institutions to personal responsibility. However, for those who master the security practices, it offers a level of financial independence that was previously impossible.

Tools for self-custody have evolved significantly. Hardware wallets, which keep keys offline and immune to computer viruses, provide a high level of security. Multi-signature setups allow users to distribute risk across multiple keys, ensuring that a single mistake does not lead to a total loss of funds.

Evolution of the Ecosystem

While Bitcoin established the concept of digital scarcity as a store of value and medium of exchange, the technology has inspired further innovation. Other networks, most notably Ethereum, have taken the underlying blockchain technology and applied it to different purposes.

Programmable Money

Ethereum differentiates itself by being a platform for decentralized applications (DApps) and smart contracts. While Bitcoin is often compared to a digital calculator—doing one thing extremely well and securely—Ethereum is like a smartphone, capable of running various applications. Smart contracts allow for complex financial agreements to be executed automatically when certain conditions are met.

This has led to the rise of Decentralized Finance (DeFi), where users can lend, borrow, and trade assets without traditional financial intermediaries. However, this added complexity comes with trade-offs. To support these features, Ethereum moved to a different consensus mechanism called Proof of Stake, which prioritizes scalability and energy efficiency but arguably sacrifices some of the absolute simplicity and hardness that characterizes the original Proof of Work model.

Comparing Objectives

It is important to distinguish between these assets based on their goals.

| Feature | Bitcoin (BTC) | Ethereum (ETH) |

|---|---|---|

| Primary Purpose | Digital Money / Store of Value | Platform for Applications |

| Consensus | Proof of Work (Energy) | Proof of Stake (Capital) |

| Supply | Capped (21 Million) | Unlimited (Dynamic) |

Bitcoin remains focused on being the hardest, most secure form of money, while other platforms explore the boundaries of what programmable blockchains can achieve. Both play a role in the broader shift away from centralized gatekeepers.

Global Financial Inclusion

The crisis of trust is not just a Western problem; it is a global humanitarian issue. Billions of people remain unbanked, lacking access to basic financial services because they do not have the necessary identification or live in regions that are not profitable for banks to serve. Digital scarcity offers an open alternative. All that is needed to participate is a smartphone and an internet connection.

This accessibility allows for seamless cross-border remittances. Migrant workers often pay exorbitant fees to send money home to their families through traditional services. A peer-to-peer digital transaction can settle in minutes for a fraction of the cost, regardless of national borders. This efficiency puts more money back into the hands of the people who earned it and strengthens local economies.

Furthermore, for citizens in countries experiencing hyperinflation, a scarce digital asset offers a lifeline. When a national currency loses half its value in a year due to government mismanagement, holding a decentralized asset can mean the difference between survival and poverty. It provides a way to opt out of a failing monetary policy and preserve the fruits of one's labor.

Conclusion

The emergence of digital scarcity was not an accident, but a necessary response to a systemic failure of trust. The 2008 financial crisis demonstrated that centralized intermediaries could not be blindly trusted to safeguard the world's wealth. By replacing fallible human institutions with verifiable code and cryptographic proof, a new foundation for value was created. This system offers a form of money that is immune to inflation, censorship, and seizure.

As the world becomes increasingly digital, the need for a native digital currency becomes more apparent. The transition from trust-based systems to proof-based systems represents a fundamental shift in how society organizes and exchanges value. While the technology continues to evolve and face challenges regarding regulation and energy, the core premise remains unshaken: money is too important to be left in the hands of middlemen.

True financial freedom requires a system where the rules are enforced by math, not by men.