The landscape of digital asset ownership has shifted significantly from simple accumulation to active participation in network economics. For many years, the primary strategy for cryptocurrency enthusiasts was to hold assets in a secure wallet, hoping for long-term price appreciation. This passive approach, often referred to as "HODLing," remains a valid strategy, but it leaves the potential productive value of the assets untapped. Modern investors now look toward methods that allow their digital holdings to generate passive income, effectively putting their capital to work while they wait for market movements.

Earning yield on cryptocurrency involves depositing assets into protocols or platforms that utilize those funds for various financial activities. These activities can range from validating transactions on a blockchain network to providing liquidity for loans. In return for locking up or depositing their assets, users receive rewards in the form of interest, often paid out in the same cryptocurrency they deposited. This mechanism mirrors traditional savings accounts in some ways but operates within a vastly different technological and risk framework.

The concept of earning interest on crypto assets has democratized access to financial tools that were previously available only to large institutions. By participating in these systems, individuals can compound their holdings over time. This means that the interest earned in one period generates its own interest in the next, accelerating the growth of the portfolio. As the infrastructure supporting these services matures, the options for participation have expanded to include a diverse array of cryptocurrencies and platform types.

The Mechanics of Yield Generation

At its core, a crypto savings or staking account functions by pooling user funds. When you deposit assets into a yield-bearing account, you are essentially lending those funds to the platform or protocol. The platform then deploys these assets to generate revenue. In a centralized context, the platform might lend your funds to institutional borrowers, hedge funds, or other traders who need liquidity for their operations. These borrowers pay interest on the loans, and the platform shares a portion of that interest with you, the depositor.

The specific mechanism for generating returns varies depending on the asset and the platform's strategy. For Proof-of-Stake (PoS) blockchains, the yield often comes directly from the network's consensus mechanism. Validators maintain the network by processing transactions and securing the blockchain. To do this, they must "stake" a certain amount of cryptocurrency. In return for their service and the capital they lock up, the network issues rewards. Platforms often aggregate user funds to participate in this staking process, distributing the rewards back to users after taking a small fee.

Another common method for generating yield involves liquidity provision. In the decentralized finance (DeFi) sector, automated market makers require pools of assets to facilitate trading. Users who deposit their tokens into these liquidity pools earn a share of the trading fees generated by the protocol. While the source text focuses heavily on savings accounts and lending platforms, many of these services utilize a hybrid approach on the backend to ensure consistent returns for their users.

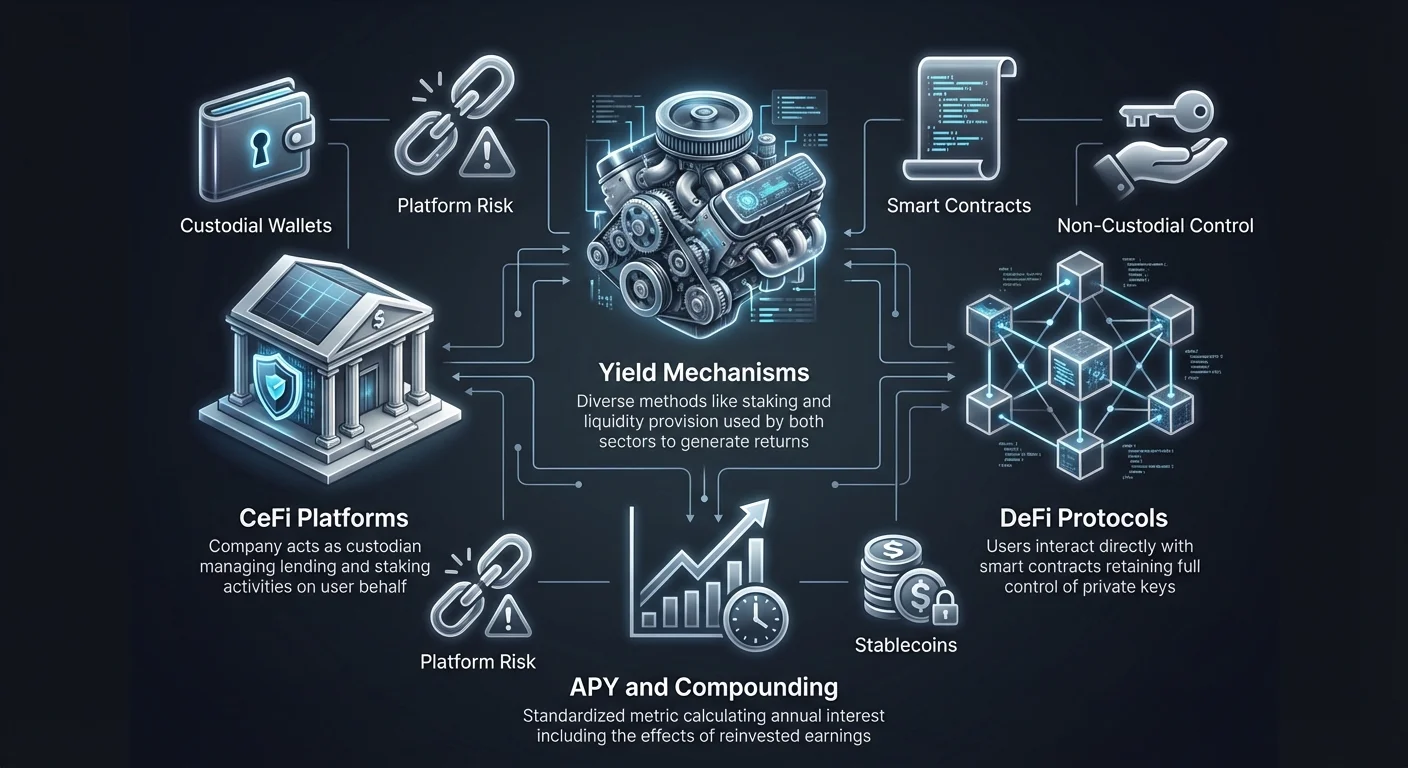

Annual Percentage Yield Explained

To understand the potential returns of these activities, investors must grasp the concept of Annual Percentage Yield (APY). APY is a standardized way to calculate the interest earned on an investment over one year. Crucially, APY includes the effects of compound interest. This differs from simple interest, which is calculated only on the principal amount. With APY, the interest is added to the principal balance periodically, meaning future interest payments are calculated on a larger base.

In the cryptocurrency market, APY rates can be significantly higher than those found in traditional finance. This is partly due to the higher demand for liquidity in the crypto space and the removal of intermediaries in decentralized protocols. However, it is important to note that these rates are rarely fixed indefinitely. They fluctuate based on market supply and demand dynamics. If many users deposit a specific asset, the yield may decrease. Conversely, if there is a shortage of an asset that borrowers need, the interest rate offered to depositors will typically rise.

Understanding APY also requires distinguishing it from APR (Annual Percentage Rate). While APY accounts for compounding, APR typically does not. When comparing different platforms or staking opportunities, ensuring that you are comparing like metrics is essential for accurate financial planning. Platforms typically display these rates prominently, but users should always check the terms to see how often interest is paid and compounded, as this frequency significantly impacts the final return.

Centralized Versus Decentralized Approaches

The ecosystem for earning yield is broadly divided into two categories: Centralized Finance (CeFi) and Decentralized Finance (DeFi). Each approach offers a distinct set of trade-offs regarding security, control, and ease of use. Understanding these differences is vital for any investor looking to participate in staking or savings programs.

Characteristics of CeFi Platforms

Centralized platforms act as custodians of your assets. When you use a CeFi service, you transfer your cryptocurrency to a wallet controlled by the company. These entities operate similarly to traditional banks. They manage the technical complexities of lending, staking, and security on your behalf. For beginners, this is often the most accessible route. The user interfaces are designed to be intuitive, often resembling standard banking apps, and they usually provide customer support services to assist with account management.

In a CeFi arrangement, you trust the platform to manage risk and solvency. These companies often have compliance teams and adhere to regulations in the jurisdictions where they operate. They may offer features like insurance on custodial assets or adhere to strict security audits. However, the user gives up direct control of their private keys. If the platform halts withdrawals or faces insolvency, the user's funds may be inaccessible. The trade-off is convenience and support in exchange for autonomy.

Dynamics of DeFi Protocols

Decentralized Finance platforms operate through smart contracts on a blockchain. There is no central company managing the funds; instead, code dictates how assets are lent, borrowed, and rewarded. Users interact with these protocols using non-custodial wallets, meaning they retain full control over their private keys and funds at all times. DeFi eliminates the counterparty risk associated with a central company failing, but it introduces smart contract risk—the possibility that the code contains bugs or vulnerabilities.

DeFi platforms often offer higher yields because they remove the intermediary taking a cut of the profits. The transactions are transparent and verifiable on the blockchain. However, the user experience can be more complex. Participants must manage their own security, understand how to interact with decentralized applications, and bear the responsibility for any errors made during transactions. Regulatory oversight is also less prevalent in the DeFi space, which can be a double-edged sword for participants seeking protection.

| Feature | Centralized Finance (CeFi) | Decentralized Finance (DeFi) |

|---|---|---|

| Custody | Platform holds funds | User holds funds (Non-custodial) |

| Ease of Use | High (Beginner friendly) | Moderate to Low (Technical) |

| Transparency | Limited (Company internal) | High (On-chain verifiable) |

Major Assets for Yield Participation

While Bitcoin is the most well-known cryptocurrency, the landscape of yield-bearing assets extends far beyond it. Proof-of-Stake blockchains and stablecoins are particularly prominent in the savings and staking sector. Investors often diversify their holdings across multiple assets to balance potential returns against volatility risks.

Ethereum and Smart Contract Platforms

Ethereum (ETH) is a primary vehicle for earning yield. As the leading smart contract platform, it supports a vast ecosystem of decentralized applications. Users can earn interest on ETH, with rates generally ranging between 2% and 7% APY. This yield usually comes from the network's staking mechanism, where ETH is locked to secure the blockchain. Because Ethereum is widely used for paying transaction fees and collateralizing loans in DeFi, demand remains consistently high.

Solana (SOL) and Cardano (ADA) are other major Proof-of-Stake assets that offer competitive staking rewards. Solana is known for its high-speed transactions and growing ecosystem, offering APYs often between 5% and 10%. Cardano focuses on a research-driven approach and strong community governance, with yields typically falling in the 4% to 7% range. Staking these assets contributes to the security of their respective networks, and the rewards reflect the network's inflation rate and transaction fee revenue.

Stablecoins and Predictable Returns

For investors seeking to minimize price volatility while earning yield, stablecoins are a popular choice. Assets like USDT (Tether) and USDC (USD Coin) are pegged to the value of the US dollar. Because traders and institutions frequently need stablecoins to enter and exit positions or to arbitrage markets, the demand for borrowing them is high. This demand translates into attractive interest rates for lenders, often ranging from 5% to 12% APY.

DAI is another stablecoin option, operating on a decentralized model. Unlike USDT or USDC, which are backed by fiat reserves in a bank, DAI is backed by crypto collateral and governed by smart contracts. Interest rates for DAI typically range between 4% and 10%. Earning yield on stablecoins is often viewed as a strategy to accumulate capital during flat market conditions, avoiding the price swings of assets like Bitcoin or Ethereum while still outpacing traditional fiat savings rates.

The Role of Lending Markets

Lending platforms are a critical component of the crypto yield ecosystem. They serve as the marketplace where supply meets demand. On one side, you have lenders—individuals or entities looking to earn passive income on their idle assets. On the other side, you have borrowers who need liquidity for trading, leveraging positions, or operational capital.

Borrowing Dynamics and Collateral

Borrowers in the crypto space rarely get unsecured loans. To mitigate the risk of default, lending platforms generally require over-collateralization. This means the borrower must deposit more value in crypto assets than they intend to borrow. For example, to borrow $5,000 worth of stablecoins, a borrower might need to deposit $10,000 worth of Bitcoin. This collateral serves as a security deposit. If the borrower fails to repay the loan, or if the value of the collateral drops significantly, the platform can liquidate the assets to ensure the lender is repaid.

This system protects the yield earners. Since the loans are backed by assets, the risk of losing the principal due to borrower default is significantly reduced compared to unsecured lending. The interest paid by the borrower forms the basis of the yield paid to the lender. The rates are dynamic; in times of high market activity, traders are willing to pay higher interest rates to access leverage, directly benefiting the depositors.

Loan-to-Value Ratios

A key metric in this ecosystem is the Loan-to-Value (LTV) ratio. This ratio expresses the amount of the loan as a percentage of the collateral's value. A lower LTV ratio implies a safer loan with a larger buffer against price volatility. Lending platforms monitor these ratios in real-time. If a borrower's LTV rises too high due to a drop in collateral value, they receive a margin call—a request to add more collateral. Failure to do so results in liquidation. This automated risk management is essential for maintaining the solvency of the lending pool and protecting the interest-generating accounts.

Evaluating Risks in Yield Farming

While the returns in crypto savings and staking can be attractive, they come with distinct risks that differ from traditional banking. Understanding these dangers is requisite for any participant. The lack of government-backed insurance, such as the FDIC protection found in US banking, means that safety relies entirely on the platform's security and the stability of the underlying assets.

Market and Volatility Risk

The most immediate risk to any crypto investor is market volatility. Even if an account pays a high APY, the underlying value of the asset can depreciate. For instance, earning 5% interest on an asset that loses 20% of its market value results in a net loss in fiat terms. This is why stablecoins are popular for pure yield seeking—they mitigate the price fluctuation of the principal asset. However, for long-term believers in assets like Bitcoin or Ethereum, volatility is often accepted as part of the investment cycle, and yield is viewed as a bonus on top of holding.

Platform and Smart Contract Risks

Platform risk refers to the possibility that a centralized exchange or lending service could fail, become insolvent, or face legal shutdowns. If a platform manages its internal lending poorly or falls victim to fraud, user funds can be jeopardized. In the DeFi world, this risk manifests as smart contract risk. If the code governing a liquidity pool or staking protocol contains a bug, hackers can exploit it to drain funds. Unlike centralized platforms where a company might intervene, blockchain transactions are generally irreversible.

Liquidity risk is another factor to consider. In times of extreme market stress, a platform might pause withdrawals if it lacks the immediate liquidity to fulfill all requests. This can leave users unable to access their funds when they need them most. High liquidity on a platform is a strong indicator of health, ensuring that deposits and withdrawals can occur smoothly without significant delays or price impact.

| Risk Category | Description | Primary Mitigation |

|---|---|---|

| Market Volatility | Asset price drops below yield gains | Use stablecoins for savings |

| Platform Risk | Exchange insolvency or failure | Diversify across reputable platforms |

| Smart Contract | Bugs in decentralized code | Use audited, established protocols |

Selecting the Right Platform

Choosing where to deposit your assets is as important as choosing which assets to buy. The crypto market offers a wide range of platforms, from established global exchanges to niche DeFi protocols. Due diligence is required to separate reliable services from those with unsustainable models.

Reputation and Security Standards

A platform's reputation is built over time. Long-standing exchanges that have weathered multiple market cycles without major security breaches generally offer higher reliability. Users should look for platforms that employ robust security measures, such as cold storage for the majority of client funds. Cold storage means the assets are kept offline, disconnected from the internet, making them inaccessible to remote hackers.

Additionally, look for features like Two-Factor Authentication (2FA) for all account actions. Platforms that encourage or enforce 2FA add a critical layer of defense against unauthorized access. Transparency regarding reserves and audit history is also a positive signal. Some platforms undergo regular third-party audits to verify that they hold the assets they claim to manage.

Fees and Terms of Service

Fee structures can significantly eat into projected returns. Investors should carefully review deposit and withdrawal fees, as well as any management fees associated with staking products. Some platforms charge a percentage of the rewards earned, while others might charge for converting assets.

The terms of the savings account also matter. Flexible accounts allow users to withdraw their funds at any time, offering high liquidity but often lower interest rates. Fixed-term accounts require users to lock their funds for a specific period, such as 30 or 90 days. In exchange for this commitment, platforms typically offer higher APYs. Choosing between these options depends on the investor's need for liquidity versus their desire to maximize yield.

Taxation and Regulatory Compliance

Participating in staking and earning interest has tax implications in many jurisdictions. In general, tax authorities often treat crypto interest as income at the time it is received. This means that every interest payment is a taxable event, calculated based on the fair market value of the asset at that moment. This is distinct from capital gains tax, which applies when you sell an asset for a profit.

Keeping detailed records is essential. Investors need to track the date, value, and amount of every interest payment. Many exchanges provide transaction history downloads to assist with this. However, the complexity of crypto taxes often leads investors to use specialized software or consult tax professionals. Regulatory environments are also evolving. Some regions may impose stricter rules on lending products or restrict access to certain yield-bearing services. Staying informed about local laws helps ensure compliance and avoids unexpected liabilities.

Investment Strategies for Yield

Developing a strategy for earning yield involves balancing risk tolerance with financial goals. A well-rounded approach often involves diversification not just of assets, but of platforms and methods. Relying on a single platform or a single coin concentrates risk.

Diversification of Assets and Platforms

Spreading investments across different cryptocurrencies captures yield from various sectors of the market. For example, holding a mix of stablecoins for steady income, along with ETH or SOL for potential growth and staking rewards, creates a balanced portfolio. Similarly, utilizing multiple platforms reduces the impact of a single service failure. If one platform pauses withdrawals, having funds elsewhere ensures continued access to liquidity.

Reinvesting and Compounding

To fully capitalize on the power of APY, investors often practice manual compounding if the platform does not do it automatically. This involves taking the interest earned and adding it back to the principal deposit. Over long periods, this effect can be substantial. However, users must weigh the transaction fees (gas fees) associated with claiming and reinvesting rewards against the potential gains, especially in DeFi environments where network fees can be high.

Conclusion

The transition from passive holding to active participation through staking and savings accounts represents a maturation of the cryptocurrency market. By leveraging Proof-of-Stake mechanisms and lending markets, investors can generate yield that rivals or exceeds traditional financial products. Whether through the convenience of centralized exchanges or the autonomy of decentralized protocols, the opportunities to put digital assets to work are vast. However, these opportunities are inextricably linked to risks, ranging from market volatility to technical vulnerabilities.

Success in this arena requires a disciplined approach to risk management and continuous education. Investors must scrutinize the platforms they trust, understand the source of the yield they earn, and remain vigilant regarding the security of their funds. As the industry evolves, the mechanisms for earning yield will likely become more sophisticated, offering new avenues for wealth generation. The key lies in balancing the pursuit of high returns with the preservation of capital.

Invest only what you can afford to lose and always secure your accounts with strong authentication.