The evolution of value exchange has always been driven by the need for greater efficiency and trust. Early societies relied on barter, a system where goods were exchanged directly for other goods. This method was inherently limited by the "double coincidence of wants," meaning both parties had to desire exactly what the other offered. To solve this, humanity moved toward commodity money. Items like shells, salt, and eventually precious metals became the standard because they were durable, divisible, and widely accepted.

Gold emerged as the enduring champion of commodity money. Its rarity and physical properties made it an excellent store of value. However, carrying heavy metals was impractical for daily commerce. This logistical friction led to the creation of representative money, such as paper certificates backed by gold reserves. Eventually, this evolved into the fiat currency systems used globally today. Fiat money derives value not from physical backing, but from government decree and public trust in the issuing authority.

While fiat currency solved portability issues, it introduced centralization risks. Central banks control the supply, which can lead to inflation and a loss of purchasing power. The digital age demanded a new evolution. This arrived with the advent of cryptocurrency. By leveraging blockchain technology, digital assets offer a decentralized alternative that operates without the need for intermediaries or central authorities. This shift represents a fundamental change in how humans perceive and transact value, defined by the core tradeoffs.

The Architecture of Digital Trust

At the heart of this financial revolution is the concept of the blockchain. Traditional databases are stored on central servers controlled by a single entity, such as a bank or a tech company. This creates a single point of failure and a target for censorship. A blockchain, in contrast, is a distributed digital record shared across a vast network of independent computers.

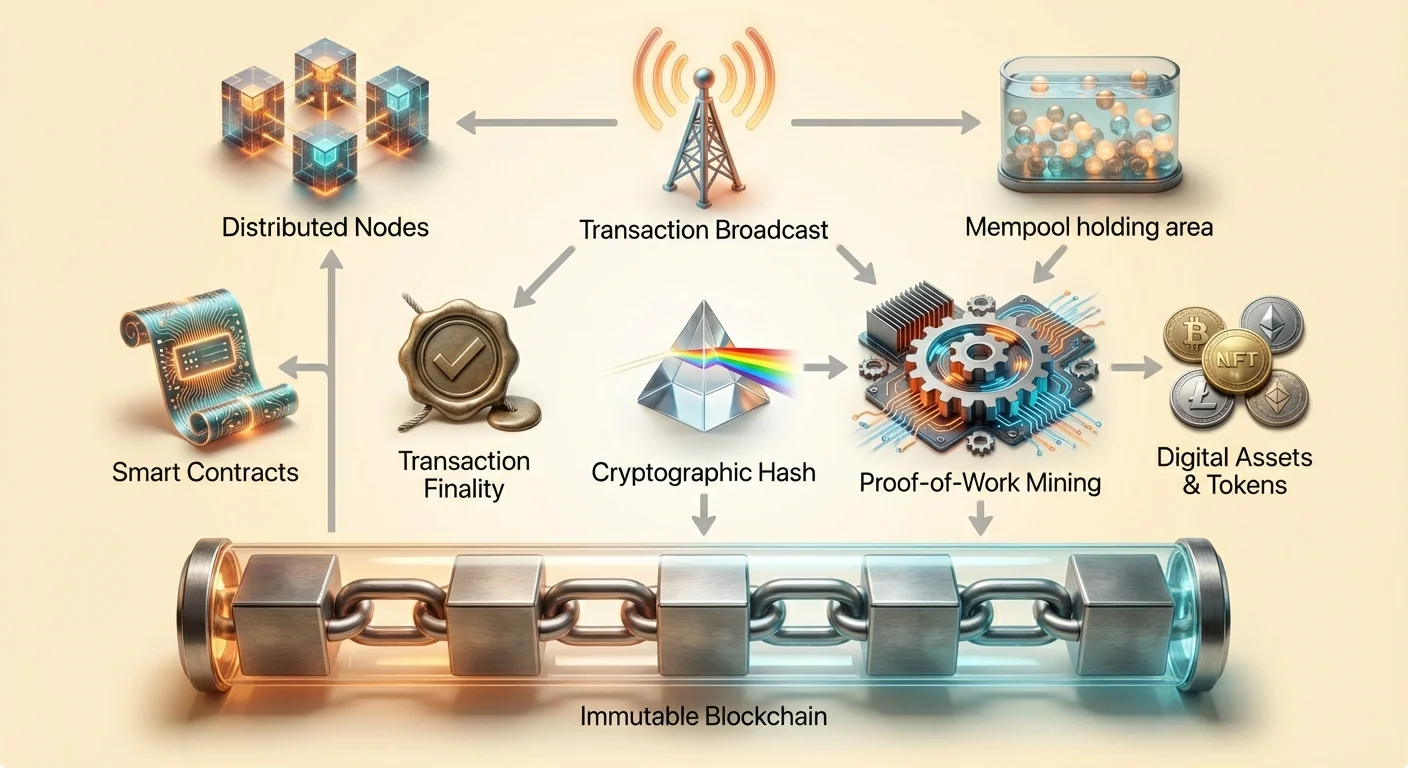

These computers are known as nodes. They work collectively to verify and record transactions. No single node has authority over the others. When a transaction occurs, it is broadcast to the network. The nodes validate the details to ensure the sender has the necessary funds and that the transaction adheres to the network's rules. This process eliminates the need for a trusted third party to oversee the exchange and verification.

Once verified, transactions are grouped together into a block. This block is then added to the existing chain of previous blocks. The structure creates a chronological history that is viewable by anyone with access to the network. This transparency ensures accountability. While user identities are often pseudonymized using alphanumeric addresses, the flow of funds is open for public audit. This architecture creates a system where trust is placed in code and consensus rather than in human institutions.

Immutability: The Unchangeable Record

One of the most critical features of blockchain technology is immutability. In the context of cryptocurrency, immutability refers to the inability to alter or delete data once it has been confirmed on the blockchain. This property is achieved through cryptographic hashing and the linking of blocks. Each block contains a unique code, or hash, that is generated based on the data within it.

Crucially, each block also includes the hash of the previous block. This creates a digital chain where every link depends on the one before it. If a malicious actor attempted to change a transaction in a past block, that block's hash would change. Consequently, the link to the next block would break. To make the change valid, the attacker would have to re-calculate the hashes for every subsequent block in the chain.

The Role of Mining in Security

This re-calculation is made deliberately difficult through a process often called mining. In Proof-of-Work systems like Bitcoin, miners compete to solve complex mathematical problems to add new blocks. This requires significant computational power and energy. The sheer cost of energy and hardware needed to rewrite the blockchain acts as a massive economic deterrent against fraud, fueling the debate around Bitcoin's efficiency and sustainability.

To alter the record, an attacker would need to control more than half of the network's computing power. For a sufficiently large and decentralized network, this is practically impossible. This security model ensures that once a transaction is recorded, it remains part of the permanent history. It prevents counterfeiting and the "double-spending" of digital assets.

Resistance to Tampering

Immutability is what makes digital assets distinct from digital files like JPEGs or MP3s. A standard digital file can be copied infinitely with no way to distinguish the original. A crypto asset, secured by an immutable ledger, cannot be duplicated. Ownership is absolute and verifiable. This permanence provides the foundation for digital scarcity, allowing digital items to hold value in a way that was previously impossible.

Finality and Transaction Confirmation

While immutability ensures history cannot be changed, finality refers to the point at which a transaction is considered irreversible. In traditional banking, a transaction might appear in a user's account immediately, but settlement can take days. During this window, transactions can be reversed or cancelled by the bank. In blockchain systems, finality is achieved through confirmations.

When a transaction is first broadcast, it enters a holding area known as a memory pool. It sits there until a miner or validator picks it up and includes it in a new block. Once that block is added to the chain, the transaction has one confirmation. As more blocks are added on top of it, the transaction becomes increasingly buried in the chain's history.

Probabilistic vs. Deterministic Finality

Different blockchains handle finality in different ways. Some systems, like Bitcoin, offer probabilistic finality. The more confirmations a transaction has, the lower the mathematical probability that it could ever be reversed. For high-value transfers, users typically wait for multiple confirmations to ensure the funds are secure. This is why a crypto transaction is not always instantaneous; security takes precedence over immediate settlement.

Other blockchain architectures aim for deterministic finality, where a transaction is considered final as soon as it is included in a block. These systems often prioritize speed and throughput, making them suitable for different use cases. Understanding finality is crucial for merchants and users to know when a payment is truly settled and safe to consider "received."

Smart Contracts: The Engine of Automation

Moving beyond simple value transfers, the industry has evolved to include programmable money. This is made possible through smart contracts. A smart contract is a self-executing contract where the terms of the agreement are directly written into lines of code. The code and the agreements contained therein exist across the distributed, decentralized blockchain network.

These contracts automatically enforce and execute actions when pre-defined conditions are met. There is no need for an intermediary, such as a lawyer or a bank, to interpret the contract or facilitate the transaction. If input A happens, then output B executes automatically. This reduces the potential for human error and removes the need for trust between transacting parties, forming a new architecture of trust.

Decentralized Applications (DApps)

Smart contracts serve as the building blocks for Decentralized Applications, or DApps. These applications run on peer-to-peer networks rather than centralized servers. Ethereum is the most prominent example of a blockchain designed to support this functionality. It acts as a platform for developers to build complex programs that benefit from the security and decentralization of the underlying network.

The rise of DApps has led to the creation of entirely new industries. Decentralized Finance, or DeFi, is a prime example. DeFi platforms allow users to lend, borrow, and trade assets without using a traditional bank or brokerage. These services run autonomously via smart contracts, available 24/7 to anyone with an internet connection.

Removing Counterparty Risk

In traditional finance, you often face counterparty risk—the danger that the other party in an agreement will default on their obligations. Smart contracts mitigate this by holding funds in escrow programmatically. The funds are only released when the code verifies that the conditions have been met. If the conditions are not met, the funds are returned. This automation creates a more efficient and transparent system for executing agreements.

The Tokenization of Value

Smart contracts also enable the creation of tokens. In the crypto industry, a token is a digital asset that represents ownership or value within a specific ecosystem. While cryptocurrencies like Bitcoin function primarily as money, tokens can represent a vast array of things. They are typically created on top of existing blockchains, utilizing the security of the base layer.

Utility and Governance

Tokens are often categorized by their function. Utility tokens provide access to a specific product or service. For example, a decentralized cloud storage network might require users to pay in a specific token to store data. Governance tokens represent a shift toward community ownership. Holders of these tokens can vote on proposals that influence the development of a project. This allows for decentralized decision-making, where the direction of a protocol is determined by its users rather than a corporate board.

Non-Fungible Tokens (NFTs)

Another major innovation is the Non-Fungible Token, or NFT. Unlike standard cryptocurrencies, which are interchangeable (one Bitcoin is equal to another Bitcoin), NFTs are unique. Each token has distinct properties that make it unlike any other. This uniqueness makes them ideal for representing ownership of digital art, collectibles, and even real-world assets like real estate, leveraging specific Ethereum token standards.

NFTs solve the problem of digital provenance. They provide a verifiable history of ownership and authenticity for digital items. This capability has opened new economies for creators, allowing them to monetize digital work directly without relying on centralized platforms that extract value.

The Spectrum of Censorship Resistance

One of the most profound implications of blockchain technology is censorship resistance. In a financial context, censorship refers to the suppression of economic activity. This can take the form of freezing assets, blocking transactions, or confiscating wealth. Traditional financial systems are highly susceptible to censorship because they rely on centralized intermediaries.

Banks and payment processors act as gatekeepers. They can be pressured by governments or internal policies to deny service to specific individuals or organizations. In contrast, a decentralized cryptocurrency network has no central authority to coerce. Censorship resistance is the ability to carry out financial actions despite the wishes of any third party.

The Three Pillars of Resistance

True censorship resistance rests on three pillars. First is the freedom to transact. This ensures that no one can prevent a user from sending or receiving assets. Second is the freedom from confiscation. In a self-custodial system, users hold their own private keys. Without these keys, no authority can seize the funds. Third is the immutability of transactions. Once a payment is processed, it cannot be reversed by a central administrator.

| Feature | Traditional Banking | Decentralized Crypto |

|---|---|---|

| Control | Bank/Government | User (Self-Custody) |

| Reversibility | High (Chargebacks) | None (Immutable) |

| Access | Permissioned | Permissionless |

Degrees of Decentralization

Not all cryptocurrencies offer the same level of protection. Censorship resistance exists on a spectrum. Bitcoin is widely considered the most resistant due to its massive, distributed network and Proof-of-Work mechanism. Newer blockchains may prioritize speed or low fees over decentralization, making them potentially more vulnerable to external pressure.

Users must understand these trade-offs. A highly centralized network might offer faster performance but could be shut down or coerced by regulators. A highly decentralized network is robust and unstoppable, serving as a hedge against overreach. This becomes vital in scenarios involving capital controls, where citizens are restricted from moving their wealth, or during bank runs where access to fiat deposits is limited.

Regulatory Friction: KYC and Anonymity

The rise of censorship-resistant money inevitably clashes with traditional regulatory frameworks. Governments enforce laws known as Know Your Customer (KYC) to prevent financial crimes. These regulations require financial institutions to verify the identity of their clients. This includes collecting personal data like government IDs and proof of address.

The goal of KYC is to combat money laundering, terrorist financing, and fraud. By linking real-world identities to financial accounts, regulators can track illicit flows of money. This system works effectively in a centralized model where intermediaries control the entry and exit points of the economy.

The Privacy Trade-off

However, strict KYC requirements create a tension with the principles of privacy and decentralization. When users interact with centralized crypto exchanges, they are often required to undergo KYC procedures. This creates a database of sensitive personal information that becomes a target for hackers. It also links a user's on-chain activity to their physical identity, reducing anonymity.

Decentralized exchanges (DEXs) and peer-to-peer platforms operate differently. They function through smart contracts and often do not require personal information to use. This aligns with the ethos of permissionless access but presents challenges for regulators. The debate between financial privacy and regulatory compliance is ongoing.

Compliance in a Decentralized World

Innovations are emerging to bridge this gap. Some projects are exploring privacy-preserving identity solutions that allow users to prove they are not bad actors without revealing all their personal data. Others focus on analyzing transaction patterns (Know Your Transaction, or KYT) rather than static identities. As the industry matures, finding a balance that protects user rights while deterring crime remains a primary challenge.

Stablecoins: Bridging Fiat and Crypto

A critical component in the adoption of smart contracts and digital transactions is the stablecoin. Cryptocurrencies like Bitcoin and Ethereum are known for their price volatility. While this creates investment opportunities, it makes them less ideal for day-to-day payments or short-term contracts. Stablecoins solve this by pegging their value to a stable asset, most commonly the US dollar, necessitating comparing collateralization models.

These assets allow traders and users to keep value on the blockchain without exposure to wild market swings. They enable the use of DeFi applications for savings and lending with predictable outcomes. There are different types of stablecoins, ranging from those backed by fiat reserves in a bank to decentralized versions backed by crypto collateral or algorithms.

Centralized stablecoins offer stability but require trust in the issuing company to hold the necessary reserves. Decentralized stablecoins attempt to maintain their peg through incentives and code, reducing reliance on a central entity but often introducing higher complexity and risk.

Conclusion

The transition from fiat currency to digital assets represents a shift from institutional trust to technological verification. Blockchain technology provides a secure, immutable ledger that guarantees the finality of transactions without intermediaries. This foundation supports the creation of smart contracts, which automate agreements and enable complex decentralized applications.

Censorship resistance serves as a safeguard for financial freedom, allowing individuals to control their wealth independent of state or corporate interference. While challenges regarding regulation and privacy persist, the structural advantages of immutability and code-based finality offer a robust alternative to traditional finance. As these technologies mature, they continue to redefine the mechanics of value exchange globally.

Code-based money empowers individuals to transact freely, securely, and without permission in a global digital economy.