The Ethereum network acts as a shared global computer capable of running decentralized applications and executing complex computations. To secure this massive digital infrastructure, the protocol has transitioned from an energy-intensive Proof of Work model to a more efficient Proof of Stake mechanism. This shift has fundamentally changed how the network operates and how participants interact with the native currency, Ether. For investors and users, this transition introduced the concept of staking, a method to contribute to network security while earning rewards.

Staking involves participants locking up their holdings to support the validation of transactions and the creation of new blocks. By doing so, these participants, known as validators, replace the miners who previously secured the blockchain. The incentives for staking are direct. Validators receive compensation for their service, creating a yield generation engine native to the protocol itself. This system aligns the interests of the network with the interests of the token holders.

However, the mechanics behind staking yield, the monetary policy governing these rewards, and the technical standards enabling liquid alternatives are complex. Understanding these elements requires a deep dive into how Ethereum manages its supply, how fees function, and how smart contracts enable new forms of financial utility.

The Mechanics of Network Consensus

From Mining to Validating

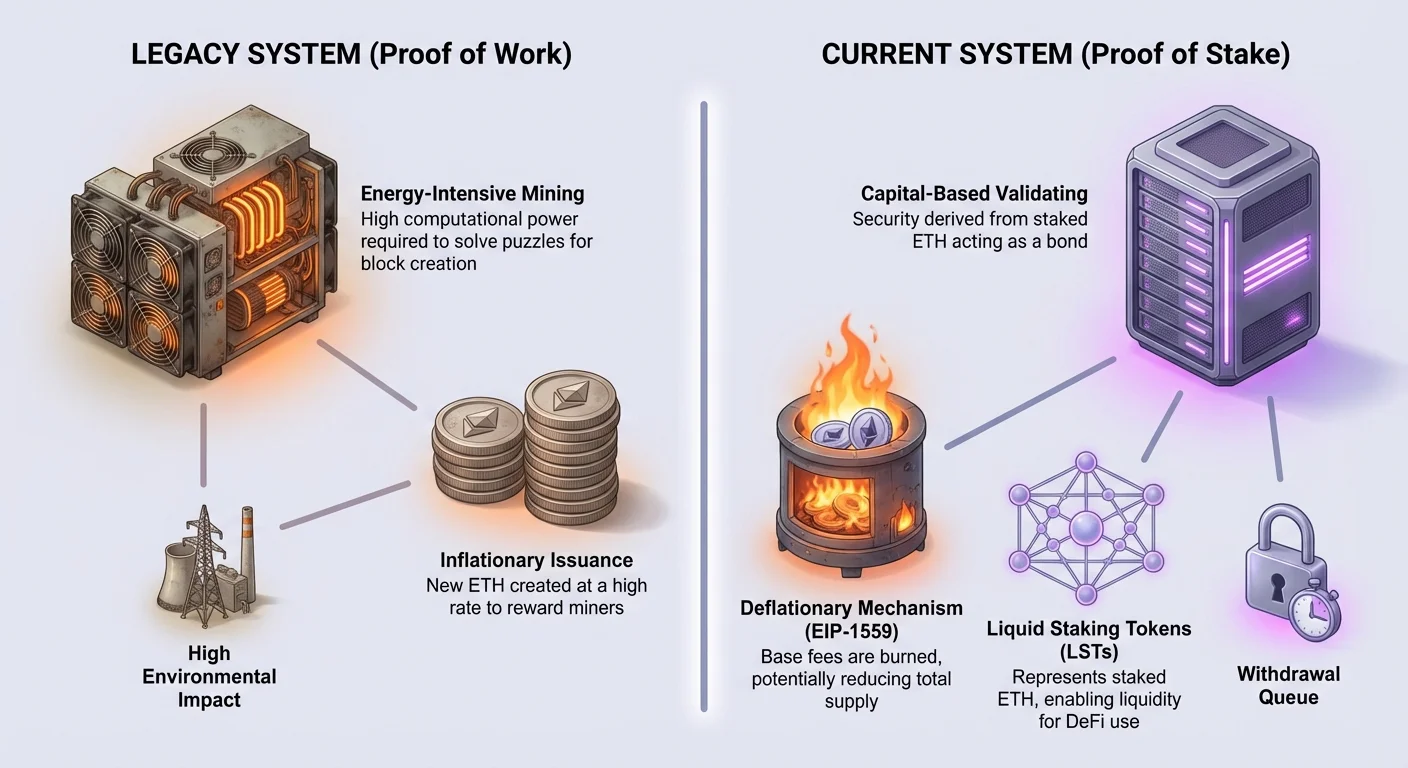

Historically, Ethereum relied on miners to process transactions. In this old system, miners used powerful hardware to solve complex mathematical puzzles. The first miner to solve the puzzle won the right to add the next block to the blockchain. They were rewarded with newly issued ETH for their efforts. This competitive process provided security but consumed vast amounts of electricity. It also required significant physical infrastructure and hardware investment from participants.

The transition to Proof of Stake changed this dynamic entirely. The network no longer requires physical mining rigs or massive energy consumption. Instead, security is derived from financial commitment. Participants now pledge, or "stake," their ETH as collateral. This stake acts as a bond of good behavior. If a validator acts maliciously or fails to perform their duties, a portion of their stake can be penalized or slashed. This economic disincentive ensures that validators act in the best interest of the protocol.

The Role of the Validator

In the Proof of Stake model, the protocol randomly selects validators to propose new blocks and attest to the validity of blocks proposed by others. This process happens in set time intervals. When a validator is chosen to propose a block, they bundle pending transactions and submit them to the network. Other validators then check this work. Once consensus is reached, the block is added to the chain, and the state of the ledger is updated.

This system democratizes participation to some extent, as it removes the need for specialized computer hardware. However, it shifts the requirement to capital accumulation. To become a full validator, a specific amount of ETH is required to be deposited into the official deposit contract. Those who do not hold the full amount required to run a standalone validator can still participate by pooling their resources with others. This collective approach allows smaller holders to access the same yield generation opportunities as larger entities.

Understanding Ethereum's Monetary Policy

Historical Issuance Schedules

Unlike Bitcoin, which has a hard cap of 21 million coins etched into its code, Ethereum’s monetary policy has been more fluid. The total supply is not capped, but the rate at which new coins are created has evolved significantly over time. When the network launched, the issuance rate was relatively high. Five ETH were created with every block, leading to an initial annual inflation rate exceeding 20 percent. This high rate was necessary to bootstrap the network and incentivize early miners.

Over the years, protocol upgrades have systematically reduced this issuance. In 2017, the block reward was lowered from five ETH to three ETH. Later, in 2019, it was further reduced to two ETH. These reductions lowered the inflation rate considerably, bringing it down to single digits. The goal has always been to secure the network with the minimum necessary issuance. This efficient approach ensures security without diluting the value of existing holdings more than necessary.

The Impact of EIP-1559

A major shift in Ethereum’s economic model occurred with the implementation of Ethereum Improvement Proposal 1559 (EIP-1559). Before this upgrade, the fee market operated on a simple auction system where users bid to have their transactions included. EIP-1559 introduced a more predictable base fee for every block. Crucially, this base fee is not paid to validators. Instead, it is burned, meaning it is permanently removed from the circulating supply.

This burning mechanism acts as a counterbalance to the issuance of new ETH. The amount of ETH burned depends directly on the demand for block space. When the network is congested and demand is high, more ETH is burned. During periods of intense activity, the amount of ETH destroyed via the base fee can exceed the amount of new ETH created. This dynamic creates a direct link between the utility of the network and the scarcity of the asset.

Deflationary Mechanics

The combination of reduced issuance from the shift to Proof of Stake and the burning mechanism of EIP-1559 has profound implications. The transition to Proof of Stake reduced the amount of new ETH issued by approximately 90 percent compared to the Proof of Work era. Because validators have lower operating costs than miners, the network does not need to issue as much currency to pay for security.

When this low issuance is paired with high network usage, Ethereum can become deflationary. If the burn rate exceeds the issuance rate, the total supply of ETH decreases over time. This is a significant departure from traditional inflationary currencies. It suggests that as the ecosystem grows and transaction volume increases, the available supply of the underlying asset could contract. This potential for scarcity adds a new dimension to the value proposition of holding and staking ETH.

The Economics of Staking Yield

The yield generated from staking comes from two primary sources: the issuance of new tokens and the priority fees paid by users. Understanding the distinction between these two revenue streams is vital for grasping how APY (Annual Percentage Yield) fluctuates.

| Revenue Source | Origin | Recipient |

|---|---|---|

| Block Rewards | New Protocol Issuance | Validator |

| Priority Fees | User Transaction Tips | Validator |

| Base Fees | User Transaction Cost | Burned (Destroyed) |

Block Rewards and Issuance

The first component of staking yield is the block reward. This is the newly minted ETH that the protocol generates to pay for security. This rate is determined by the total amount of ETH staked in the network. The protocol is designed to issue enough reward to incentivize security, but not more. As more people stake, the reward rate per validator slightly decreases. This self-balancing mechanism ensures that there is always an equilibrium between network security and inflation.

These rewards are paid automatically by the protocol. They represent the baseline yield that a validator can expect to earn over the long term. Because this issuance is programmable and predictable based on the total stake, it provides a relatively stable foundation for yield calculations. However, it is the variable component of rewards that often drives short-term fluctuations in staking returns.

Transaction Fees and Tips

The second component of yield comes from transaction fees. While the base fee is burned, users have the option to add a "priority fee" or tip to their transactions. This tip is an incentive for validators to prioritize their specific transaction over others in the memory pool. When the network is busy, users who need their transactions processed quickly will increase their tips.

These tips are paid directly to the validator who proposes the block. Unlike the steady trickle of block rewards, income from tips can be volatile. During a highly anticipated NFT mint or a sudden market crash, the demand for block space spikes. Consequently, the tips paid to validators can increase dramatically for short periods. This means that a staker's yield is partially dependent on the overall activity and health of the on-chain economy.

The Concept of Liquid Staking

The Liquidity Problem

Staking participates in securing the network, but it comes with a significant trade-off: illiquidity. When a user deposits ETH into the staking contract, those funds are locked. They cannot be used for trading, used as collateral in DeFi, or sent to other wallets. Furthermore, the process of unstaking is not instant. There is a withdrawal queue and a delay mechanism designed to maintain network stability.

This lock-up creates an opportunity cost. An investor holding staked ETH cannot react to market movements or utilize that capital elsewhere. For many users, losing access to their liquidity is a barrier to participation. They want to earn the yield associated with network security, but they also want the freedom to use their assets within the broader ecosystem. This dilemma led to the innovation of Liquid Staking Tokens.

The ERC-20 Solution

To solve the liquidity issue, developers utilize the ERC-20 token standard. ERC-20 is a technical standard that defines how tokens function on the Ethereum network. It ensures that tokens are fungible, meaning each unit is identical to another, much like one dollar bill is equal to another. This standardization allows tokens to interact seamlessly with exchanges, lending protocols, and wallets.

Liquid staking providers create a smart contract that accepts a user's ETH and deposits it into the staking mechanism on their behalf. In return, the contract mints and sends the user a new ERC-20 token representing their claim on that staked ETH. This new token is a Liquid Staking Token (LST). The user now holds a token that represents their original deposit plus any rewards that accrue over time.

Comparing WETH and Liquid Staking

The concept of wrapping an asset to make it usable in smart contracts is not new. Wrapped Ether (WETH) is a common example. ETH, being the native currency, predates the ERC-20 standard. To use ETH in many decentralized applications, it must be "wrapped" into an ERC-20 compliant form known as WETH. Users deposit ETH into a smart contract and receive WETH at a 1:1 ratio. The WETH can then be used in trading and DeFi.

Liquid staking tokens function similarly but with a crucial difference: value accrual. A WETH token is simply a static representation of ETH. It does not earn interest or rewards. An LST, however, represents staked ETH that is actively earning yield from the network. As the underlying staked ETH accrues block rewards and transaction tips, the value of the LST increases relative to ETH, or the quantity of tokens in the user's wallet grows. This makes LSTs a capital-efficient way to hold exposure to Ether while retaining the ability to transact.

Risks and Considerations

Smart Contract Vulnerabilities

While staking offers rewards, it introduces distinct layers of risk. One primary concern is smart contract risk. Liquid staking relies on complex code to manage deposits, distribute rewards, and handle withdrawals. If there is a bug or an exploit in the smart contract code of the liquid staking provider, funds could be lost. This risk is distinct from the security of the Ethereum blockchain itself. It is a risk specific to the application layer built on top of it.

The Ethereum Virtual Machine (EVM) executes these contracts exactly as written. If the logic contains a flaw, the EVM will still process it. Users must trust the audits and the development teams behind the liquid staking protocols. Unlike holding ETH in a self-custody wallet, holding an LST involves trusting the code of the issuer.

Market Volatility and De-pegging

Another risk factor involves market dynamics. Liquid staking tokens are traded on open markets. Ideally, the price of an LST should closely track the value of the underlying ETH plus accrued rewards. However, market conditions can cause the price to deviate. If there is a sudden rush of users trying to sell their LSTs for ETH, the liquidity in the market might dry up.

This scenario can lead to a "de-peg," where the LST trades at a discount compared to the value of the ETH it represents. While the underlying ETH is still safe in the staking contract, a user forcing a quick sale during a de-peg event would realize a loss. This highlights that while LSTs offer liquidity, that liquidity is dependent on market depth and buyer demand.

Future Outlook and Layer 2 Integration

The Ethereum ecosystem is continuously evolving. A major focus of current development is scalability through Layer 2 solutions. These are separate networks that handle transactions off the main chain to increase speed and reduce costs. They process bundles of transactions and then settle the final state on the main Ethereum blockchain.

Staking plays a crucial role here as well. The security provided by Layer 1 stakers ultimately protects the integrity of these Layer 2 networks. As activity migrates to Layer 2s to avoid high gas fees, the demand for ETH as a settlement currency remains. The transaction fees paid by these Layer 2 networks to verify their data on the main chain contribute to the yield earned by stakers.

Furthermore, future updates to the protocol aim to improve the efficiency of data availability. These technical improvements will likely lower the cost for Layer 2 networks to operate, potentially driving more usage. Increased usage eventually translates to more priority fees and a higher burn rate. Thus, the future of staking yield is tied closely to the success of the protocol’s scaling roadmap.

Conclusion

The transformation of Ethereum from a mining-based system to a staking-based economy has redefined the utility of its native asset. Staking has turned ETH into a productive asset capable of generating yield through protocol issuance and transaction fees. This shift has also introduced deflationary pressure through the burning of base fees, creating a unique economic structure where high network usage can reduce total supply.

Liquid Staking Tokens have emerged as a vital tool for navigating this new landscape. By leveraging the ERC-20 standard, they unlock the value of staked assets, allowing capital to flow freely through the decentralized finance ecosystem. However, users must weigh the benefits of yield and liquidity against the risks of smart contract bugs and market volatility. As the network continues to scale and evolve, staking will remain the central pillar of Ethereum’s security and economic model.

Staking allows you to earn rewards for securing the network, but requires balancing yield against liquidity and technical risks.